Cambria Automobiles has now released its interim results for the year ending 2015.

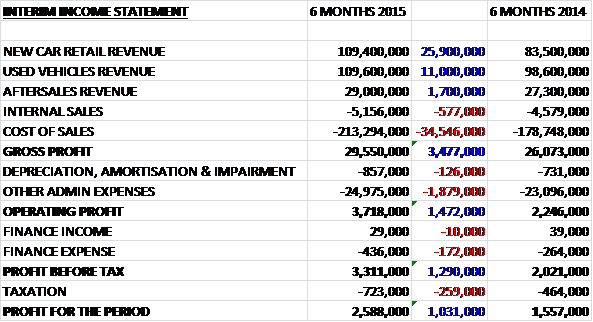

When compared to the first half of last year, revenues increased across all three sectors with new car sales up £25.9M, used car sales up £11M and aftersales increasing by £1.7M. Cost of sales also increased to give a gross profit some £3.5M higher. Admin expenses were also up slightly and finance expenses were up, reflecting the interest on the loans drawn down last year and increased consignment stock interest charges, to give a profit before tax some £1.3M higher before the tax payment meant that the profit for the period stood at £2.6M, an increase of £1M when compared to the first six months of 2014.

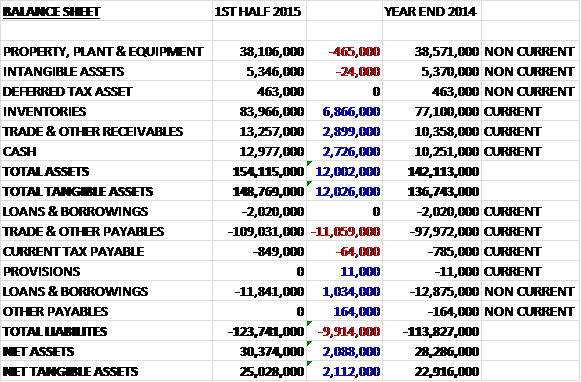

Total assets increased by £12M when compared to the end point of last year, driven by a £6.9M increase in inventories, a £2.9M growth in receivables and a £2.7M increase in cash, partially offset by a £465K reduction in the value of property, plant and equipment. Liabilities also increased as an £11.1M increase in payables was partially offset by a £1M fall in loans and borrowings. The end result is a £2.1M increase in net tangible assets to £25M.

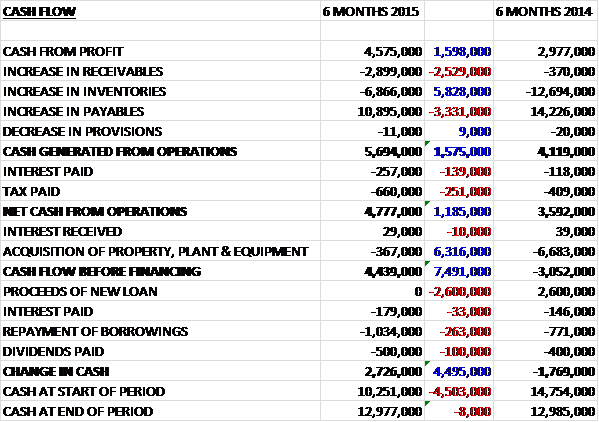

Before movements in working capital, cash profits increased by £1.6M to £4.6M. A large increase in payables was not entirely offset by increases in receivables and inventories and after higher interest and tax payments, the net cash from operations stood at £4.8M, an increase of £1.2M. Capital expenditure only accounted for £367K as there were no acquisitions during the period so there was an impressive free cash flow of £4.4M, of which £1M was used to pay down debt and £500K was spent on dividends to give a cash flow for the half year of £2.7M to increase the cash pile to £13M which was incidentally almost exactly the level of cash at the end of the first half of last year.

New car gross profits increased by £1.6M, although gross margin fell slightly to 6.6%. Sales grew by 15.6% to 5,362 units, and like for like sales volumes increased by 8.8% when the acquired Barnet outlet is discounted. This performance compares slightly favourably to the 8.2% year on year increase in new car registrations in the UK as a whole with the private registrations element of the market increasing by 6%. The group’s sale of new vehicles to private individuals increased by 12.7%, supported by strong consumer offers from the manufacturers. New commercial vehicle sales increased by 35% to 511 units whilst new fleet sales increased by 36% to 266 units which is a trend that is expected to continue.

Used car gross profits grew by £1M with the margin remaining steady at 9%. Sales grew by 2.9% to 7,106 units with like for like sales flat year on year, although profit per unit increased by 7.7%. Aftersales profits increased by £800K with the margin increasing slightly to 42.8% with service hours increasing by 4.4% year on year but showing no growth on a like for like basis. As seen above, capital expenditure was fairly low during the period but a planning application has been submitted for the substantial redevelopment of the Barnet facility for Jaguar Land Rover acquired last year to create a state of the art dealership. The refurbishment is likely to cost about £5M and will be incurred next year.

The board are still actively pursuing acquisition opportunities to strengthen the group’s position in luxury and premium brand cars. In the past they have concentrated on acquiring and turning around underperforming dealerships but they are now in a position to consider acquisitions which are immediately earnings enhancing. The performance in March was ahead of plan and the previous year and the board are confident that this momentum will continue to deliver an improved performance across all of its activities. March saw a record level of car registrations In the UK and the current economic landscape with low interest rates and a favourable exchange rate against the Euro allowing manufacturers to continue to deliver strong consumer offers which should ensure that volumes in the new car market in the UK remains robust.

As already announced, after the half year end, the group acquired the Land Rover franchise in Swindon from TH White for a total cash consideration of £7.56M which included £3M in goodwill payments. The group intends to draw down a new £1.6M loan in respect of the freehold property acquired with the balance satisfied by the existing financing facilities. This new dealership represents the second Land Rover outlet acquired by the group and will be relocated to the current Jaguar dealership already owned by Cambria in the town.

Net debt stood at £900K at the end of the half compared to £700K at the same period of last year. After a 50% increase in the interim dividend, the shares now yield 1.1% on an annual rolling basis with the board intending to maintain a progressive dividend policy for the full financial year as long as the payment of the dividend does not detract from the primary aim to utilise available fund to continue to grow the business.

Overall this was a fairly good update. Profits were up and net assets increased to improve what is an already strong balance sheet, although it should be noted that there is a large amount of operating lease payments payable that are off the balance sheet. The cash generation was excellent during the period although again there is a bit of a caveat as the capital expenditure during the period was very low and the group has announced that it expects to spend £5M on developing the Barnet Land Rover outlet alone next year. Operationally, like for like new car sales were slightly ahead of the market but used car sales and aftersales were both flat year on year, albeit with increased profits.

It is perhaps a bit harsh, though, to compare profits on a like for like basis given the fact that the group’s strategy is to buy new dealerships to increase its profits. Also, the new car market in the UK continues to be very strong with a record March this year. The prevailing economic conditions mean that this performance is likely to continue in the immediate future. Finally, the dividend increase is welcome but still not much to get excited about. Overall I have very mixed feelings about an investment here. As long as the favourable market conditions continue, the group is likely to continue to do well. I may look to add if the opportunity presents itself, although for now I will wait to see what Vertu’s update tomorrow brings.

On the same day the group announced that a company controlled by Chairman Philip Swatman purchased 85,000 shares at a value of just over £50K and he now owns 250,000 shares in the group. This is a good vote of confidence and I am very tempted to buy in here.

On the 8th September the group released a trading update covering the year as a whole. They have continued to perform well in the second half of the year and results for the year are expected to be ahead of current market expectations. Trading in the first eleven months of the year has been substantially ahead of the same period last year on both a total and like for like basis. New vehicle unit sales were up 9% but up only 1% on a like for like basis. Unit sales to private retail customers were up 9.3% (2.1% LFL) with gross profit per retail unit improving by 15.3% (LFL 1.6%). Used vehicle sales also performed well with unit sales 4.5% (1.3% LFL) ahead and gross profit per unit up by 8.1% (LFL 6.7%) which has significantly enhanced the profit derived from the used car part of the business. Growth in the aftersales operations has also continued, with hours sold up by 8% (2% LFL) year on year.

Both the Barnet JLR dealership acquired in July 2014 and the Swindon Land Rover dealership acquired in April 2015 are integrating well and are contributing in line with expectations. Heading into the important September trading period, the new car order book is building well reflecting strength in the market as a whole.

It is always nice to see an “above expectations” trading update. The new car sales look a little slow but the contribution from the acquisitions looks very good and that increase in the second hand profit per unit looks very good to me. I am very happy to continue holding here.