Central Asia Metals is a mining and exploration company with operations primarily in Kazakhstan. The group’s principle activity is the production of copper cathode at its Kounrad operations in the country. They also have an investment in a copper tailings project in Chile and are listed on the AIM exchange.

The costs of the delivery to the end customers are effectively borne by the group through means of an annually agreed buyer’s fee which is offset from the selling price. The group sells and distributes its copper cathode product primarily through an offtake arrangement with Traxys which is for a minimum of 90% of the plant’s output. The copper is transported from the Kounrad site by rail and delivered to the end customers in Turkey. As part of the offtake arrangements, the group sells the copper cathodes at a price linked to the LME copper price.

The plant at Kounrad was constructed as a 10,000 tonnes per annum plant and the resource at Kounrad estimates that the dumps contain over 600,000 tonnes of copper, of which some 250,000 tonnes is recoverable giving the mine an estimated life of over 15 years. The plan now is to increase capacity to 15,000 tonnes per annum.

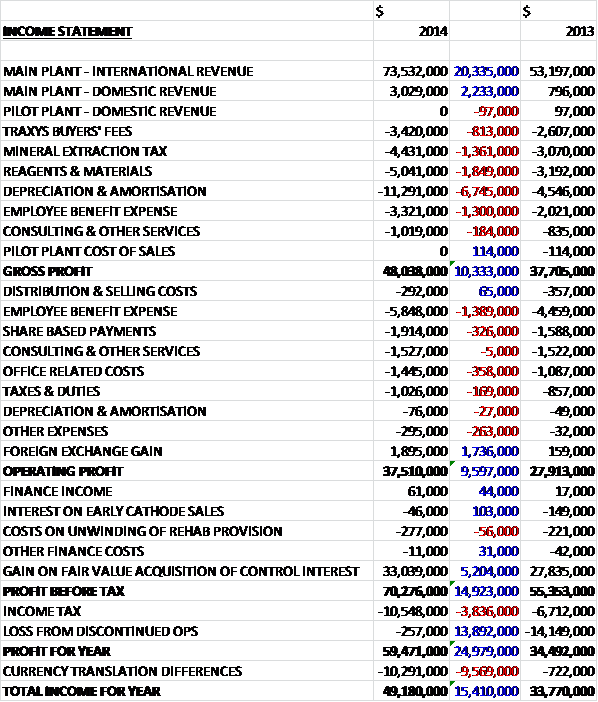

Revenues increased considerably year on year as the group took complete control of the Kazakh mine. There was also an increase in cost of sales, including a $6.7M growth in depreciation and amortisation following the uplift in asset values to give a gross profit some $10.3M ahead of last year. Admin expenses also increased with a $1.4M growth in staff costs, a $358K increase in office costs and a $326K growth in share based payments, partially offset by a $1.7M increase in the foreign exchange gain so that operating profit increased by $9.6M to $37.5M. This then nearly doubled by a $33M gain on the fair value gain on the acquisition of the joint partner venture and after an increase in tax and a $13.9M fall in the loss from discontinued operations in Mongolia after they were fully impaired last year meant that the profit for the year came in at $59.5M, an increase of $25M year on year, although this comparison is fairly meaningless given the fact that last year the group did not have full control of the subsidiary. It should also be noted that there was also a $10.3M charge relating to the translation of foreign operations.

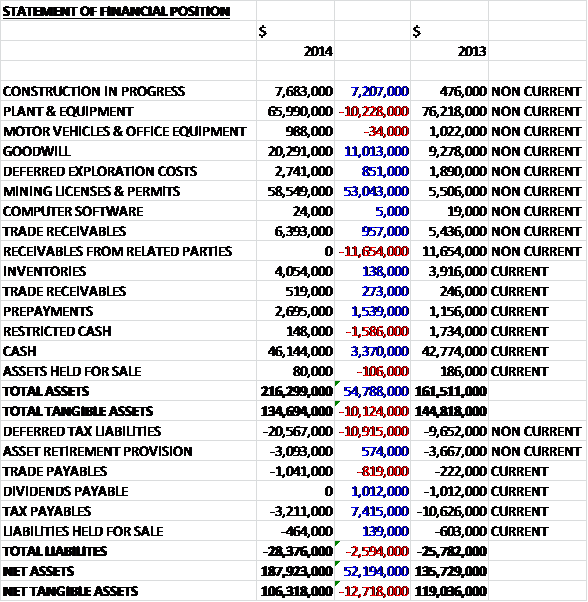

When compared to the end point of last year, total assets increased by $54.8M driven by a $53M growth in the value of mining licenses and permits as a result of the Kounrad acquisition, an $11M increase in goodwill, a $7.2M growth in construction in progress and a $3.4M increase in non-restricted cash partially offset by an $11.7M fall in receivables from related parties (the ex-joint venture) and a $10.2M decline in the value of plant and equipment. Total liabilities also increased during the year as a $7.4M fall in current tax payables as the group paid an instalment against the corporate tax payable, and a $1M eradication in the dividends payable was more than offset by a $10.9M increase in deferred tax liabilities due to the acquisition. The end result is a net tangible asset level of $106.3M, a decline of $12.7M year on year.

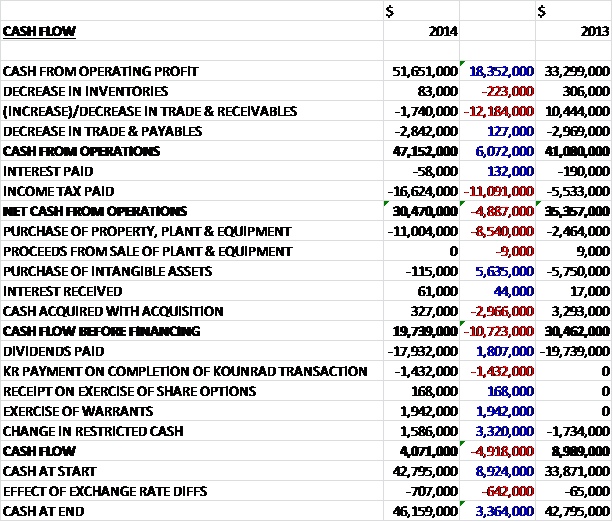

Before movements in working capital, cash profits increased by $18.4M to $51.7M. The large fall in receivables that occurred last year did not repeat this time and the group paid $11.1M more in income tax so that net cash from operations actually fell by $4.9M to $30.5M. The group then spent $11M on property, plant and equipment mostly relating to the SX-EW plant expansion with the rest going on the new boiler and sustaining capex, and $115K of tangible assets so that the free cash flow was an impressive $19.4M. The group paid the bulk of this out in dividends and also paid out 1.4M relating to the completion of the Kounrad transaction before a $1.9M receipt relating to the exercise of warrants and a $1.6M fall in restricted cash meant that the cash flow for the year stood at $4.1M to give a cash level of $46.2M at the year-end.

In October 2013 the ownership of Kounrad Copper Company increased from 60% to 100% following the acquisition of 40% of the business. Consequently the comparative results for 2013 comprise of 60% of the revenues and costs associated with the project for the first nine months of the year but 100% for the final three months whereas the results for 2014 comprise 100% of the revenues and costs for the full year.

In Kounrad, a total of 11,136 tonnes of copper cathode was produced during the year which represents a marginal increase on the production target of 11,000 tonnes. Since the start of leaching operations in 2012, the focus of the activity has been on the Eastern dump area which is estimated to contain about 168,000 tonne of copper at the outset of operations with some 80,000 tonnes expected to be recovered in total so there should be some 52K tonnes still to be recovered from the area. From 2017 there will be an increasing proportion of recovered copper supplied by the transfer of leach solutions from the Western dump areas and by 2019 the Western dump area will be the predominant feed source following the gradual depletion of the Eastern dumps.

The C1 cash cost of production was $1,566 per tonne compared to $1,600last year, aided by the depreciation of the Kazakh currency, and fully absorbed costs within Kazakhstan were $3,642 per tonne, an increase from the $3,152 recorded last year due to increased depreciation and amortisation charges as a result of the accounting treatment of the acquisition of the 40% share of the Kounrad project. A total of 11,163 tonnes of copper was sold at an average copper price of $6,794 per tonne compared to $7,114 last year. During the year the utilisation rate of the plant was 98.7% which met expectations.

Leaching operations in winter when temperatures regularly get to -20 are facilitated by a combination of heating the dump irrigation solution and also covering certain areas of the dripper piping system with a layer of protective high-density polyethylene sheeting. As leaching operations progress on the Eastern dumps, the distances from the plant to the leaching cells become greater and during 2015 the operations plan involves leaching various blocks located in the Northern part of dump 7 which will result in pumping the irrigation solution a distance of 3km. In order to achieve the delivery of the required volume of solution and to ensure that dumps 5 and 2 can be irrigated from 2016 onwards, a modification to the pump delivery system is being undertaken which involves the addition of a second parallel pipeline.

These two pipelines will be equipped with booster pumps at a point close to the junction of dumps 7 and 5 in order to overcome the calculated extra head pressure that is required to maintain the flow volumes. At the year-end the pipeline had already been installed and all necessary pumping equipment ordered and ready for delivery to site. It is expected that it will be commissioned in late Q2 2015.

The board have agreed on a phased expansion of annual copper cathode production to 15,000 tonnes at the existing plant with a capital expenditure programme over the next three years through to 2017. It is thought that through the expansion of the existing SX-EW facility to a nominal capacity of 15,000 tonnes, the Eastern dumps can provide the required quantity of copper to reach this by 2016. Thereafter, through the phased introduction of leach solutions from the Western dump area, this capacity can be maintained until the cessation of leaching activities in the Eastern dumps. The required quantity of solutions transferred between the East and West sites can be achieved by the installation of two 12.6km pipelines.

During the year detailed engineering plans were finalised for the expansion. They comprised the installation of extra heating capacity through the addition of two 2.8 MW boilers thus allowing increased winter production. In addition the plant is to be expanded by the inclusion of a sixth mixer settler and construction of a separate EW building containing 24 new EW cells and associated equipment, thus increasing the copper plating capacity by about 50%. The construction work on the new boilers started in June and was completed by October which increased the total installed heating capacity to 14 MW and provides for a planned design increase in heating winter raffinate flows from 450m3/hr to 750m3/hr. This raises the temperature of cold incoming solution at 1 degree C to 10 degrees prior to passing through the SX mixer settler units. By December the boiler house was performing somewhat better than design forecasts.

The second stage of the plant expansion requires the addition of a sixth mixer settler unit in the SX section and a new EW section, containing 24 EW cells. Following the receipt of the necessary state permits, work commenced on site in July and commissioning is scheduled for Q2 2015. The new EW overhead crane, which is used for harvesting cathode plates, had been fully installed by the end of the year and will be used to install and equip the 24 EW cells during Q1 2015. All the purchase orders and equipment supply contracts have been placed, with many items already delivered. The capital costs for the expansion will be in line with, if not less than, the announced capital budget of $15.5M.

Engineering design of the facilities required to start leaching at the Western dumps by Q2 2017 has progressed well during the year. The technical project documentation was completed in July and has been submitted for approval and it is anticipated that state approval will be granted in Q2 2015. Once all approvals have been received, equipment procurement and certain construction work will start on site from late Q3 2015. This stage of the Kounrad expansion plan requires the construction and installation of two pipelines, each of 12.6km.

One pipeline will enable PLS from the Western dumps to be transferred to the expanded SX-EW plant for processing into cathodes. The other pipeline will enable the raffinate solution from the SX section to be transported back to the dumps for irrigation purposes. In order to provide the ability to operate through the winter at the Western dumps, a boiler house of the same design as the original facility at the Eastern plant will be installed. During December, final engineering discussions were undertaken to finalise the specifications and revalidate the capital cost, estimated to be about $19.5M for this phase of the expansion.

The supply of sufficient technical quality water from 2017 onwards to allow simultaneous leaching at both the Eastern and Western dumps has always been an important consideration. At present all such water is provided from an underground reservoir sourced from an abandoned mine about 8km to the NE of the plant. Studies have indicated that this reservoir has the capability to provide adequate water at least until the end of 2017 but beyond this time, the source may not be capable of providing the extra volume of water needed to simultaneously operate two leaching sites. The decision was taken, therefore, to install a water pipeline to transport water drawn from Lake Balkhash to the Kounrad site. This will provide sufficient water for the project through to the end of its life as well as assisting the local community with plentiful water for their own purposes.

This project required the upgrading of an intermediate pumping station close to Balkhash and the installation of 16.5km of pipeline. The estimated capital cost of the programme is $2.7M and it is anticipated that installation works will be completed by the end of 2015. As the abstraction system from the lake does not operate in winter, commissioning will be conducted during Q2 2016. During the winter months, the make-up water requirement is very low, which can be provided by the underground reservoir as required.

Last year the group acquired a 50% interest in Copper Bay ltd for a cash investment of $3.2M. Copper Bay Ltd was incorporated with the sole purpose of developing the Copper Bay project in the Atacama region of Chile. For nearly forty years until 1975, several copper mines disposed of the tailings residues from their mineral processing operations into the Rio Salado which outflows into Chanaral Bay. Over that period it is believed that some 250M tonnes of tailings were discharged into the bay. They now sit in the bay and on the beach at Chanaral and cover a 13km2 area. The business is examining the viability of reclaiming and processing the copper tailings to produce copper cathode and copper concentrate. The $3.2M invested into the business was used to deliver a pre-feasibility study and significant progress has been made with $1.8M spent on advancing the project with work expected to be completed by Q2 2015.

During the year a drilling campaign was conducted on the beach with a total of 136 holes being drilled to an average depth of 9.2m and a total of 1,022 samples were collected for assaying. The resource is currently being assessed with the potential for additional copper resources to be investigated at a later date. During the year the technical focus has been on assessing the most efficient means of extracting the copper from the resource. The outline process is for the tailings to be reclaimed by dredging from the beach zone, after which the reclaimed solids will be pumped to the nearby processing plant.

The first stage of the process consists of leaching whereby sulphuric acid is added to the tailings in order to solubilise the copper oxides. This will be conducted in a series of leach tanks to produce a PLS for conventional processing into copper cathodes by means of a SX-EW plant. The second stage of the processing is for the leached residue solids to undergo a froth flotation process in order to extract residual sulphide materials into a saleable concentrate product. The final tailings reside from this combined process will then be returned either to the beach zone as coarse backfill or to a tailings management facility as fine tailings.

This latter process is expected to result in about 90% of the processed tailings from the plant being returned to the beach zone and this part of the process is very important to both the economic viability and the environmental success of the project. A significant amount of bench scale metallurgical testing has been carried out throughout the year and this has indicated that a copper recovery in the range of 70% to 73% can be achieved from the above processes. Additional testing performed on a seven tonne bulk sample taken from the drilling programme is under consideration as part of the next stage of the project.

There is a high degree of local and national support for any proposed improvements to the environmental conditions in the area due to historical pollution and any initiative to reduce the impact of the tailings on the environment will be welcomed by the regional state authorities. During the year an environmental fatal flaw analysis of the project was undertaken together with an environmental baseline study. The study did not identify any fatal flaws in the project and provided management with a better understanding of the environmental obligations. The most important environmental aspect for the viability of the project involves the assessment of the re-deposition of the processed tailings to the beach zone and this issue continues to be studied.

The feasibility study is expected to be complete during Q2 at which time a decision will be taken by the board regarding additional investment of $3M to increase their holding to 75% of the project which would then be used to finance more detailed work on the project.

The total capital cost for the Kounrad expansion is estimated at $35M over the next three years including the $9.4M already spent this year but in addition to the estimated $6.5M that will be spent on sustaining capital expenditure for the plant and Kounrad site during the three year period. At the year-end the group has $46.3M in cash with $12.7M held in Kazakhstan to cover the expansion costs and working capital requirements in the country along with instalment payments of corporate income tax. There were no debts outstanding.

The group continues to hold for sale the assets it owns in Mongolia and is actively seeking to sell the Ereen and Handgait projects. The sales are taking longer than the board anticipated due to the current political and regulatory uncertainties in the country and the implications of a court case brought by the minority partner on the Ereen project. In June, Bayanresources was sold for nil consideration.

During the year the group completed the acquisition of the remaining 40% of the Kounrad project which consisted of two key parts. The first transaction involving the transfer of an additional 40% ownership of Kounrad Copper Company was completed in October 2013. The second transaction involving the transfer of the remaining 40% economic interest in the subsoil use contract was completed in May 2014. On completion of the Kounrad transaction, a total of 21,211,751 shares were issued to Kenges Rakishev in May. An additional cash payment of $1.4M was paid to Kenges on that date to reflect the entitlement to dividends payable. In all the total consideration came to $67.2M, mostly in shares and the transaction generated goodwill of $20.3M with a recognised gain on fair value of the assets of $32.4M. As well as becoming a major shareholder in the group after the Kounrad transaction with 16% of the total share capital, Kenges Rakishev was also appointed to the board

Apparently there are currently insufficient reserves available in the company for distribution as dividends so the directors are proposing to rectify this by completing a court approved capital reduction scheme by cancelling the company’s share premium account and transferring the reserves to retained earnings which is expected to become effective around May 2015. I have to say this is going over my head somewhat but the company apparently undertook a previous capital reduction scheme in 2013.

The group is somewhat susceptible to foreign exchange movements and had the Kazakh Tenge and British Pound strengthened by 10% against the US dollar, profits for the year would have been $1.9M lower. The group is also clearly affected by the price of copper. Given the debt-free status of the group, the board have up to now not bothered with a hedging policy but given the recent volatility in the price of copper, the board have now allowed a hedging policy of up to 30% of the group’s twelve month production, although this has not yet been utilised and there is currently no hedging in place. A 10% fall in the price of copper would have reduced profits for the year by $7.7M.

Another risk for the group is Kazakhstan tax risk. The tax system in the country is at an early stage of development. The application of tax laws and regulations are still evolving which considerably increases the risks with respect to mining and subsoil use operations. Tax regulation and compliance is subject to review and investigation by the authorities who may impose extremely severe fines, penalties and interest charges. The group’s main receivable is the VAT incurred on purchases within Kazakhstan and a total of $6.4M was still owed to the group. They are working closely with advisors and local partners to try and recover the amount due and the planned means of recovery will be through a combination of the local sales of cathode copper to effectively offset VAT liabilities and by a successful appeal to the authorities.

The Chinese economy is crucial to the copper market, accounting for just under half of world demand. Concerns about growth in the construction sector in China have been compounded by the huge overcapacity that has been constructed in the major cities of the country and the correction in China’s real estate sector could prove damaging to the demand for copper. Despite this scenario, China’s copper consumption is still expected to grow by 4% in 2015. On the supply side of the equation, the situation is not clear. Analysts have been predicting a surplus of copper supply in 2015 and 2016 due to production capacity increases coming on stream from the major miners but the recent reductions in the copper price have led many to reassess this expected surplus. In recent months Rio Tinto has lowered forecasts for its Kennecott mine by 100,000 tonnes, BHP has cut 150,000 tonnes from Econdida’s 2015 outlook and Glencore shaved guidance for Minera Alumbrera by 50,000 tonnes. These kind of figures really put CAM’s production guidance in context and current consensus is that the market will return to a deficit after 2016.

During the year the copper price came under pressure due to increasing supply and continued concerns over the outlook for the growth of the Chinese economy. These price pressures became particularly acute at the start of 2015 when the price fell to a five and a half year low of $5,505 per tonne. Whilst the current commodity price environment provides a challenge to all copper producers from which the group is not immune, their low operating cash costs mean they are in a good position to remain competitive with the price needing to go below $3,500 per tonne before the group stops being profitable, something that has happened only twice over the past ten years.

At the current share price the shares trade on a PE ratio of 10.5 but this increases to 13 on next year’s consensus forecast. The dividend yield currently stands at 8% falling to a still-decent 5.6% on next year’s forecast.

Overall then, this has been an interesting year for the group characterised by the acquisition of the remaining part of the Kounrad joint venture that they did not previously own. Profits did increase but net tangible assets fell during the year. The operating cash flow also fell but this was due to a bit payment of tax and were it not for this, the underlying cash flow was positive. During the year 11,136 tonnes of copper was produced at a cash cost of $1,566 per tonne and a fully absorbed cost of $3,642. The average sales price of $6,794 does suggest plenty of headroom here but the price of copper has been falling and stood at $5,505 at the start of the year – still profitable for the group but this is clearly something that needs to be watched closely.

The other main risk really is the reliance on just one project in Kazahstan so the group is very susceptible to political risk in the country. This could end up being mitigated by the very interesting tailings project in Chile with more details on this in the future. The Kounrad mine itself seems like a small but quality asset which has a low cost base despite the freezing winter temperatures requiring boilers to heat the raffinate. There is clearly potential risk in the expansion but if that goes to plan, the mine will be producing 15,000 tonnes a year before long. The assets in Mongolia look like total write-offs and seem to be impossible to get rid of.

At a forward PE ratio of 13 and a dividend yield of 5.6% the shares certainly look fairly decent value but really this is a play on the price of copper and with the Chinese economy struggling at the moment, this is clearly a risky buy.

On the 21st May the group released an update covering Kounrad expansion. The SX-EW extension has been successfully commissioned with the internally funded $13.4M programme including construction works and equipment installation for the extended SX-EW facilities. The extra mixer-settler tank has increased the plant’s solution treatment capacity by 33% to 1,200 cubic metres per hour, and the additional 24 electro-winning cells have increased the daily plating capability by 42% to 50 tonnes of copper. The infrastructure upgrade also included the installation of an additional 10MW transformer substation.

This stage 1 expansion and additional 5.6MW boiler capacity installed towards the end of last year have increased the plant’s nameplate annual capacity to 15,000 tonnes of cathode copper and the company remains on track to achieve its 2015 production target of 13,000 tonnes of copper and 15,000 tonnes in 2016. The main focus now is on implementing the stage 2 expansion programme, the approvals process for which is proceeding as schedule.

On the 24th June the group announced that it is exercising its right to invest a further $3M to increase its shareholding in Copper Bay ltd to 75%. This investment is being made following the completion of an internal pre-feasibility study on the Chanaral Bay Copper Tailings Project. The funds will be used to conduct a definitive feasibility study on the project. The study revealed an indicated resource estimate of 104,345 tonnes of copper at a grade of 0.244% and an inferred resource estimate of 19,838 tonnes at a grade of 0.234%.

Much of the inferred resource will be used as a berm to protect the resource area from sea ingress during dredging operations and it will then be reclaimed on completion of dredging. This resource only covers the Chanaral beach area and there is potential upside at Chanaral to significantly increase this resource through the future inclusion of a similar amount of additional mineralised material in the surf and bay zones covered by the license.

Test work indicates that the most effective means of extracting the copper from the tailings is by initial acid leach to produce a clean copper concentrate and indicative metallurgical recovery from the PFS test work is 72.8%. Dredged material will be fed to the plant and will result in annual copper production of 8,600 tonnes comprising 6,200 tonnes of cathode and 2,400 tonnes of copper concentrate. The reported resource in the beach area would be sufficient for a mine life of nine years and the study envisages fine tailings being stored in a tailings management facility located 3km from the proposed site of the processing plant and coarse tailings re-deposited on the beach.

Environmental and social studies commenced over a year ago will continue throughout the next year and a half. The Chanaral area is well known for the adverse environmental impact caused by the historic deposition of tailings into the bay and beach zone and, due to the reclamation of these tailings the project is strongly supported by the local community.

Project economics are based on the mineral resources estimated on the beach and do not consider the material that may be identified in the surf and bay zone. The prelim capital expenditure estimate is $88M. Estimated C1 cash costs of operation are $1.34/lb with a project NPV at 8% discount rate of about $50M after tax with an IRR of 21% based on a long term copper price of $3/lb – I don’t know why they have to keep switching between lbs and tonnes as it is rather annoying! Future exploitation of the surf and bay zones may provide significant economic upside to the project. I must say this all sounds rather promising unless that copper price keeps coming down.

On the 25th June it was announced that CFO Nigel Robinson exercised options over 144,736 shares at an exercise price of 1c per share – very nice for him! On the same day he sold the lot and earned himself £262K which is certainly a nice pay day. It is a shame he didn’t hold on to any of the shares but he still owns 646,715.

On the 29th June the group announced that an incident occurred on the Kounrad site that will impact on the production guidance of 13,000 tonnes for this year. During normal production activity a problem occurred in the solvent extraction section which resulted in a significant quantity of the organic inventory being lost to the dumps within a very short time frame. After inspection, it was identified that one of nine weir plates in the recently commissioned SX mixer settler had fallen out of position, resulting in the ability of the organic inventory to escape from the circuit via the raffinate and onto the dumps. The reasons for the failure of the plate are currently being investigated.

The problem has since been rectified and the plant has started again but at a much lower flow rate. This will continue for several more days until the site team can stabilise the plant and determine the full extent of the loss of organic inventory, any impact on the pipeline infrastructure and the duration of time that the plant will need to operate at reduced production capacity before the organic inventories can be replenished. The impact on full scale production at Kounrad is temporary and will not affect the ability of the plant to produce high quality copper cathodes at competitive costs of production.

On the 3rd July the group provided a production update for the first half of the year. Kounrad Q2 production of 3,093 tonnes of cathode copper brings production for the half year to 5,444 tonnes, a 6.9% increase over the first half of 2014. The increase is largely due to the expanded boiler house capacity at the plant resulting in higher solution volume treatment rates during the winter months.

Following the earlier incident, the SX-EW plant is now operating at 45% capacity. Orders for the replacement organic inventory have been placed and are expected to be delivered on site by mid-August. Following their arrival, the will be added to the SX circuit, after which the dump leaching process will need to reach pre-incident flow rates which are more than double the current level. Management anticipate that the overall circuit will be back at design capacity by the start of September. The incident will impact the previously stated 2015 production target of 13,000 tonnes of copper and at the moment it looks as though it will be closer to 12,000 tonnes which is still an increase on the 11,136 tonnes produced last year but disappointing nonetheless.

The share price has not done much over the past year, it could be looking for a leg-up now though?

This is the real problem. The copper price hit a recent low towards the end of August and is now attempting a bit of a recovery but whether this will be maintained remains to be seen.