Central Asia Metals has now released their interim results for the year ending 2018.

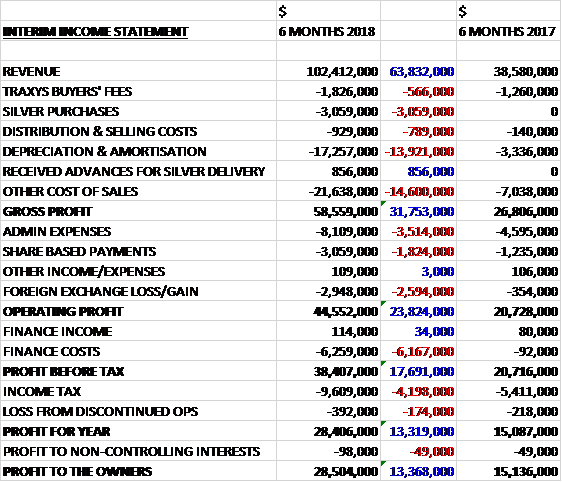

Revenues increased by $63.8M when compared to the first half of last year. Depreciation was up $13.9M and other cost of sales grew by $14.6M to give a gross profit $31.8M higher. Admin expenses were up $3.5M, share based payments increased by $1.8M and the forex loss increased by $2.6M which meant the operating profit was $23.8M higher. Finance costs were up $6.2M and tax charges increased by $4.2M, all of which gave a profit for the period of $28.5M, a growth of $13.4M year on year.

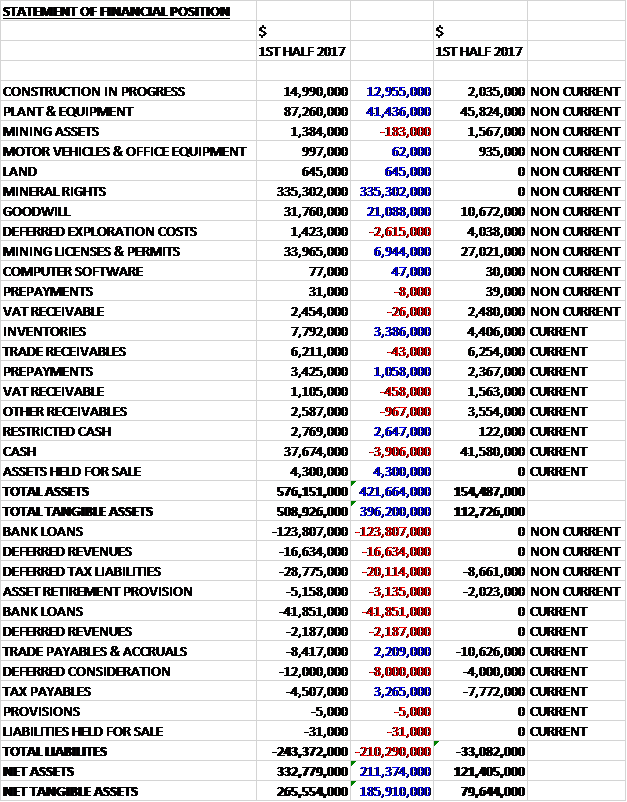

When compared to the end point of last year, total assets increased by $421.7M driven by a $335.3M increase in mineral rights. A $41.4M growth in plant & equipment, a $13M increase in construction in progress, a $21.1M growth in goodwill and a $6.9M increase in mining licences. Total liabilities also increased during the period due to a $165.7M increase in bank loans, a $20.1M growth in deferred tax liabilities, a $16.6M increase in deferred revenues and an $8M increase in deferred consideration. The end result was a net tangible asset level of $265.6M, an increase of $185.9M over the past six months.

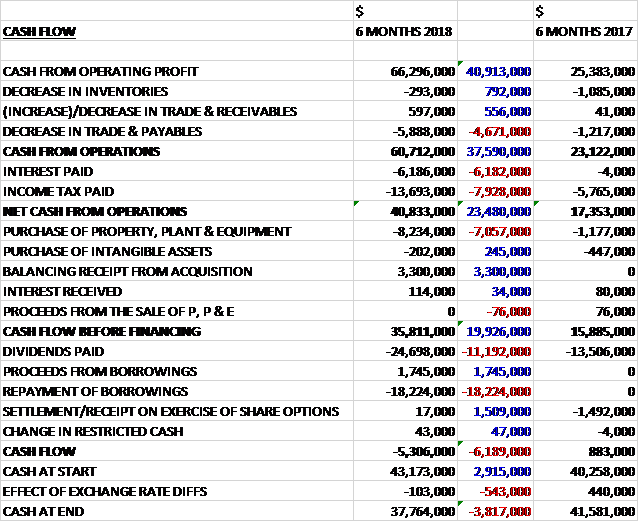

Before movements in working capital, cash profits increased by $40.9M to $66.3M. There was a cash outflow from working capital, interest payments increased by $6.2M and tax payments were up $7.9M to give a net cash from operations of $40.8M, an increase of $23.5M year on year. The group spent $8.2M on fixed assets and $202L on intangibles but brought in $3.3M as a balancing receipt from the acquisition to give a free cash flow of $35.8M. Of this, $16.5M was used to pay back loans and $24.7M was spent on dividends to give a cash outflow of $5.3M and a cash level of $37.8M at the period-end.

The EBITDA at the Kounrad mine was $29.2M, a decline of $100K year on year. Copper production was slightly below that of the first half of last year due to a particularly cold winter and sales were down due to a temporary increase in the inventory of cathode on site awaiting dispatch. The average copper price received was $6,672 per tonne which was around $1,000 per tonne higher than last time which offset the 12% decrease in sales volumes.

The mine produced 6,747 tonnes of copper cathode in the period, down from 7,027 in the first half of last year due to a particularly cold winter in Kazakhstan. Despite this they remain on course to achieve their full year copper production guidance of between 13,000 and 14,000 tonnes. During the period leaching was undertaken with 4,312 tonnes of copper being leached from the Western Dumps. Copper sales in the period were 6,044 tonnes and 763 tonnes were in stock, representing a 12% decrease in sales volumes.

During the period the team undertook a cathode refurbishment programme and also focussed on strengthening the trench walls around the Western Dumps initial leaching area. The Kounrad cost of sales increased by $600K due to recognising a full period relating to the Western Dumps leaching process. The cash cost of copper production increased somewhat from 45c per pound to 53c per pound as a result of leaching operations at the Western Dumps for a full six month period, which resulted in slightly higher electricity and reagent costs along with higher labour charges.

The EBITDA at the Sasa mine was $41.7M which represents the maiden result. The mine is on track to meet its full year production guidance of between 21,000 and 23,000 tonnes of zinc and between 28,000 and 30,000 tonnes of lead. In the first half, total ore mined was 390,932 tonnes and ore processed was 393,605 tonnes. The average mill head grades were 3.34% for zinc and 3.91% for lead with the average metallurgical recoveries being 83.8% for zinc and 93.5% for lead.

Total H1 production was 22,624 tonnes of zinc concentrate (21,719 tonnes) at an average grade of 48.7% and 19,712 tonnes of lead concentrate (20,301 tonnnes) at a grade of 73%. The payable production of zinc was 9,211 tonnes of zinc and 13,666 tonnes of lead. Payable base metal concentrate sales were 9,256 tonnes of zinc and 13,701 tonnes of lead. During the period the mine sold 180,233 ounces of silver which had been pre-sold. The average zinc price was $3,256 per tonne and for lead it was $2,478 per tonne.

During the period, construction of TSF4 continued with completion achieved of the river diversion tunnel, water channel and starter dam. Subject to final approvals, the group remains on track for completion of this new facility by the end of 2018. After consultation with its key site trade union in April, the mine offered an average pay rise of 16% to the workforce.

A review and audit of the processing plant was undertaken and several areas identified for performance improvement. The results of these studies are currently being implemented. In April the mine took delivery of a stirred media detritor mill that was ordered by the previous owners with the expectation of improved zinc recoveries, which replaced the existing zinc regrind mill. The mill was installed with some metallurgical successes but its inclusion in the processing plant has not, as yet, resulted in a consistently improved performance. Zinc recoveries will be monitored during the second half of the year. Sasa’s zinc equivalent cash cost of production was 44c per pound which was the same as the costs last year.

At Shuak, the second exploration season started in May and since then thee CHT drilling programme has been completed, plus 1,050 metres of diamond drilling. An IP survey is also underway. The Kyzyl-Sor prospect has been identified as the key area of interest in terms of oxide mineralisation, with the northern area of the license showing the most promise for sulphide mineralisation.

There has been quite a lot of upheaval at the board level with a new CEO, Gavin Ferrar being appointed CFO and Scott Yelland joining as COO.

Going forward, the prices of copper, zinc and lead have been under considerable pressure since June over fears for global growth and trade disputes. The group are on track to deliver 2018 annual production guidance and the board are also looking for more acquisitions which seems a bit soon to me.

After the period-end in July the Macedonian authorities established that withholding tax amounting to $5.9M is due on income from payments in 2016 and 2017 which has now been paid in full. This charge is currently being appealed by the group.

At the current share price the shares are trading on a PE ratio of 11 which falls to 9.4 on the full year consensus forecast. After the dividend was kept the same the shares are yielding 7.1% which falls to 6.9% on the full year forecast.

On the 4th October the group released a trading update covering Q3 which demonstrated that the group is on tack to achieve 2018 production guidance for all three of their metal products. At Koundrad, Q3 copper production of 3,938 tonnes brings output for the first nine months of the year to 10,686 tonnes. The total amount of copper recovered from the Western Dumps in the year to date represents 65% of the total. Copper sales in Q3 were 3,626 tonnes, bringing the nine month total to 9,670 tonnes.

At Sasa, in Q3 mines and processed ore were 206,406 tonnes and 206,014 tonnes respectively. The average head grades were 3.25% zinc and 3.92% lead while metallurgical recoveries were 85.7% for zinc and 94% for lead. Zinc recoveries have increased during the period as the performance of the new stirred media detritor mill has stabilised. In the period 11,658 tonnes of concentrate containing 49.3% zinc and 10,455 tonnes of concentrate containing 72.7% lead were produced. Payable production of zinc was 4,810 tonnes and of lead was 7,222 tonnes.

Exploration activities continued at Shauk, focussing primarily at the Kyzyl-Sor prospect. A total of 19,467 metres of core hydrotransport drilling has been untaken and this programme has now finished. A 77km IP geophysical programme to identify sulphide mineralisation has also been completed.

Overall then this has been a step change period for the group. Profits were up, net assets increased and the operating cash flow improved with a decent amount of free cash being generated. This would be expected as the group partially used equity to purchase another mine. Kounrad actually seemed to have struggled a little bit. Lower production due to a harsh winter has offset a higher copper price, without which these results would be considerably worse. There is not much comparison for Sasa but it seems to be performing fairly well.

Since the period-end there has been some considerable pressure on prices due to the increased trade disputes but the group is on track for their production targets and with a forward PE of 9.4 and yield of 6.9% these shares look quite cheap. Tricky, if metals prices don’t deteriorate further it could be worth buying back in here.

On the 9th January the group released a trading update covering Q4. They produced 3,363 tonnes of copper to make 14,049 for the year, a decline of just 34 tonnes. They produced 5,769 tonnes of zinc to make 22,535 for the year, a growth of 947 tonnes. They produced 7,401 tonnes of lead to give 29,388 for the year, a decline of 493 tones. They have released guidance for 22K to 24K tonnes of zinc; 28K to 30K tonnes of lead; and 12.5K to 13.5K tonnes of copper for 2019.

The construction of the tailings storage facility 4 at Sasa is now materially complete and is expected to complete in H1 2019. The facility should provide tailings storage for seven years. During the second half of the year the group started a Life of Mine study which is also expected to be completed sometime during 2019. As part of this study, they undertook drilling at both Svinja Reka, the location of current operations, and Golema Reka, which was mined between 1981 and 2010. The aim of the programme was to identify additional resource potential and convert a portion of the inferred resources to the indicated category.

Sinja Reka currently has an inferred mineral resource of 2.7M tonnes containing 3.2% lead and 2.1% zinc. Results of the drilling have confirmed extensions to the mineralisation down to and beneath the 750 metre level at significant intersections. The grades identified in the area below the 830 metre level appear to be higher than the current inferred resource demonstrates. Golema Reka currently has an inferred mineral resource of 7.4M tonnes containing 3.7% lead and 1.5% zinc. Drilling demonstrated an extension of mineralisation beneath the 700m level.

During the year the group completed the second exploration season at Shuak. While the results have been encouraging, they are of the opinion that this project is unlikely to be of sufficient scale to warrant development. Therefore they plan to return the asset to the current 20% shareholders, while retaining a net smelter return royalty of 1.25% as per the original agreement. The group have screened 22 business development opportunities and conducted three site visits. They are currently further reviewing two potential base metal opportunities.