Character Group has now released its final results for the year ended 2016.

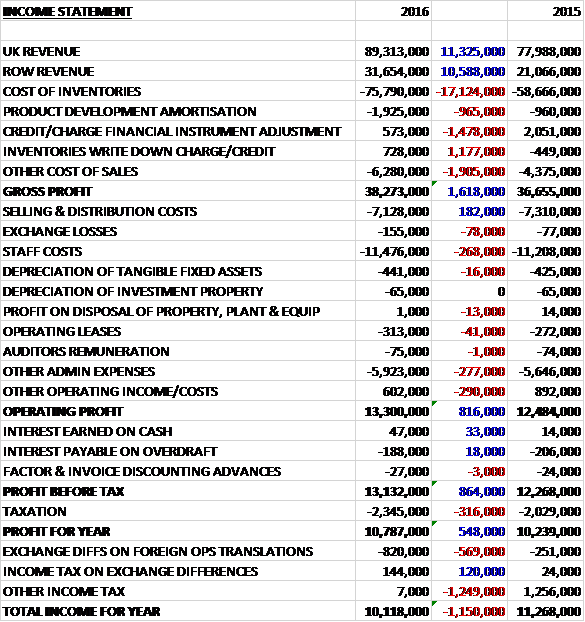

Revenues increased when compared to last year with an £11.3M growth in UK revenue and a £10.6M increase in ROW revenue, aided by the weakness of Sterling. Cost of inventories increased by £17.1M, amortisation was up £965K and other cost of sales grew by £2.2M to give a gross profit £1.6M ahead of 2015. Selling and distribution costs reduced by £182K but staff costs were up £268K and other operating expenses grew by £426K with a £290K fall in other operating income which meant that the operating profit was £816K higher. Finance costs were down marginally but tax charges increased by £316K to give a profit for the year of £10.8M, a growth of £548K year on year.

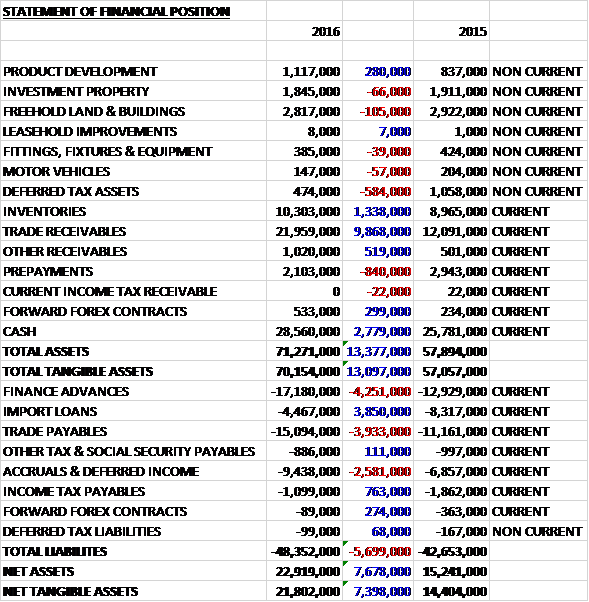

When compared to the end point of last year, total assets increased by £13.4M to £71.3M driven by a £9.9M growth in trade receivables, a £2.8M increase in cash and a £1.3M growth in inventories. Total liabilities also increased as a £3.9M reduction in import loans was more than offset by a £4.3M increase in finance advances, a £3.9M growth in trade payables and a £2.6M increase in accruals and deferred income. The end result was a net tangible asset level of £21.8M, a growth of £7.4M year on year.

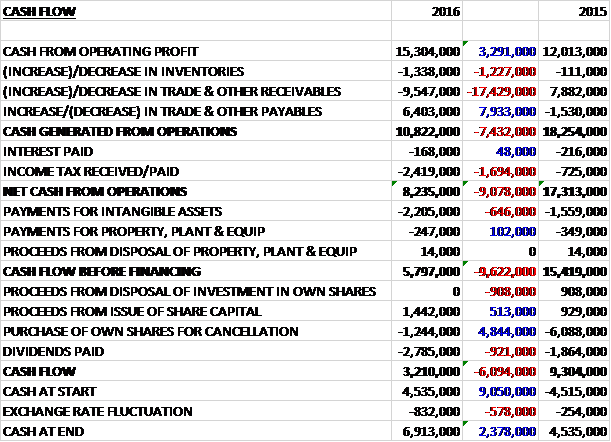

Before movements in working capital, cash profits increased by £3.3M to £15.3M. There was a cash outflow from working capital compared to an inflow last year and after tax payments increased by £1.7M the net cash from operations came in at £8.2M, a decline of £9.1M year on year. The group spent £2.2M on intangible assets and £247K on property, plant and equipment to give a free cash flow of £5.8M which easily paid for the dividends of £2.8M to give a cash flow for the year of £3.2M and a cash level of £6.9M at the year-end.

Peppa Pig remained the top brand this year and was joined by Little Live Pets and Teletubbies, relaunched at the start of the year, in the top three. The Little Live Pets range has recently been widened to include Snuggles My Dream Puppy which was names by the Toy Retailers association as one of the top 12 dream toys for 2016. Further additions to this range will be introduced in 2017.

The group also launched Stretch Armstrong on a global basis which saw initial sales exceed expectations. The Stretch product portfolio will be widened in the coming year and the board are excited about the brand’s potential to contribute significantly to future profitability.

During the year the group acquired 258,936 shares at a cost of £1.2M, although they seem to have raised £1.4M from new share capital so it seems a net gain in the number of shares in issue. They currently have an unutilised authority to buy back up to a further 2,791,298 shares and it remains part of the overall strategy to repurchase their shares when appropriate.

A significant proportion of the group’s purchases are made in US dollars so they are therefore exposed to currency fluctuations and the recent weakness in Sterling is not helpful. The increasing strength of the US dollar against sterling post-Brexit has the potential to cause an increase in the cost of sales, notably the factory cost of production and freight charges. A number of measures have been put in place to mitigate these effects and the growth in US sales has also helped maintain gross margin levels comparable with those achieved pre-Brexit.

Overall current trading continues to be in line with board expectations with pleasing levels of predictable contribution being generated from the established brands. The board are also satisfied with the inroads that they have made into overseas markets and expect this to be a prominent factor in delivering their growth ambitions going forward.

At the current share price the shares are trading on a PE ratio of 10.8 which falls to 10.3 on next year’s consensus forecast. After the final dividend was increased by 33%, the shares are trading on a PE ratio of 2.9% which increases to 3.2% on next year’s forecast.

On the 12th December it was announced that joint MD Kiran Shah sold 147,000 shares at a value of £772K. He still owns 2,140,001 shares and this is quite a substantial director sale.

Overall then this has been a fairly decent year for the group. Profits increased, net assets improved and although the operating cash flow deteriorated, this was due to working capital movements in cash profits increased with a decent amount of free cash being generated. The Teletubbies seem to be selling OK but the real breadwinner remains Peppa Pig, although Little Live Pets are doing well and Stretch Armstrong looks to have potential.

The deterioration in the value of Sterling is unhelpful but the group seem to have done a good job mitigating the effects. The large director sale is not a good sign but he has done this before so I am not overly concerned and with a forward PE of 10.3 and yield of 3.2% these shares look decent value to me and I am happy to remain invested.

On the 20th January the group released a trading update following their AGM. Whilst they are confident that the market expectations for 2017 shall be achieved, they expect the results for H1 to be lower than those reported in the first half of last year. In the four months to December, sales were marginally lower than the same period last year and UK gross margin was adversely affected by the devaluation of sterling. The steps taken to mitigate the reduction in margin are currently starting to take effect and they will be fully implemented in the second half. They are expecting both their international and domestic sales to grow in the remainder of the year.

The balance sheet, including the cash position continues to strengthen considerably and the reaction to the 2017 product ranges has apparently been excellent. This is a bit of a disappointing update but on the whole I am continuing to hold as the shares still look cheap.

On the 23rd January the group announced that finance director Mark Dowding purchased 9,554 shares at a value of £48K. He now owns 93,395 shares.

On the 14th March the group announced that finance director Mark Dowding purchased 6,605 shared at a value of £34K. He now owns 100,000 shares in the company. It was also announced that non-executive director Clive Crouch purchased 9,803 shares at a value of £50K which brings his holding up to 15,358 shares.