Circle Oil has now released its final results for the year ended 2016.

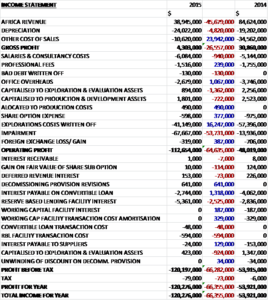

Revenue fell by $45.7M when compared to last year reflecting both lower oil prices and a decline in production and although depreciation was up $4.8M, other cost of sales declined by $23.9M to give a gross profit $26.6M below that of 2014. Salaries & consultancy costs increased by $940K but office overheads declined by $1.1M. We then see a $1.4M decrease in the amount capitalised to exploration and a $722K fall in the amount capitalised to development. There was a $16.2M decline in exploration costs written off but impairment costs increased by $53.7M which meant that the operating loss increased by $64.6M. We then see a $641K favourable decommissioning provision revision and a $1.3M decrease in in the interest payable on the convertible loan, partially offset by a $2.5M growth in the reserve based lending facility interest and a $594K increase in the RBL facility transaction cost. This all meant the loss for the year came in at $120.3M, a growth of $66.4M year on year.

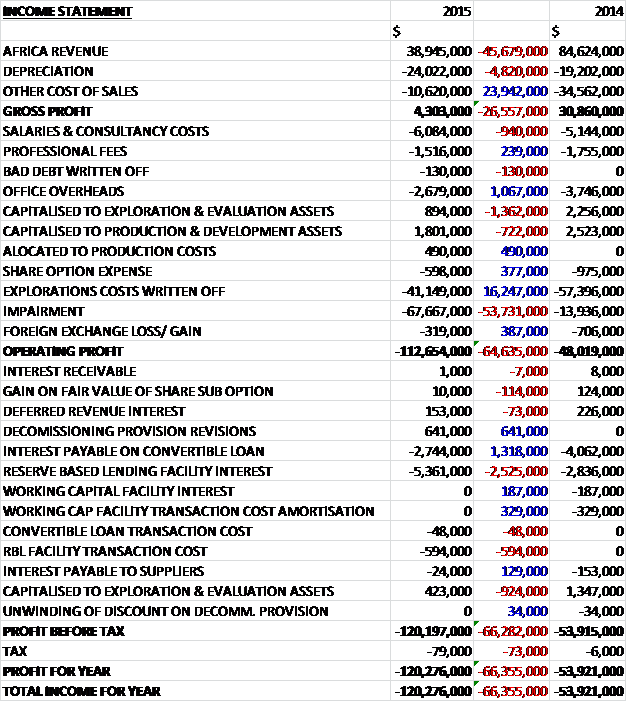

When compared to the end point of last year, total assets declined by $134.9M driven by a $33.9M decrease in exploration assets, a $70.6M decline in production assets, a $26.3M fall in cash and a $2.9M decrease in trade receivables. Total liabilities also fell during the year as a $9M decline in the convertible loan and a $21.9M fall in trade payables was partially offset by a $14.1M growth in other bank borrowings and a $2.3M increase in the decommissioning provision. The end result was a net tangible asset level of $9.5M, a decline of $85.8M year on year.

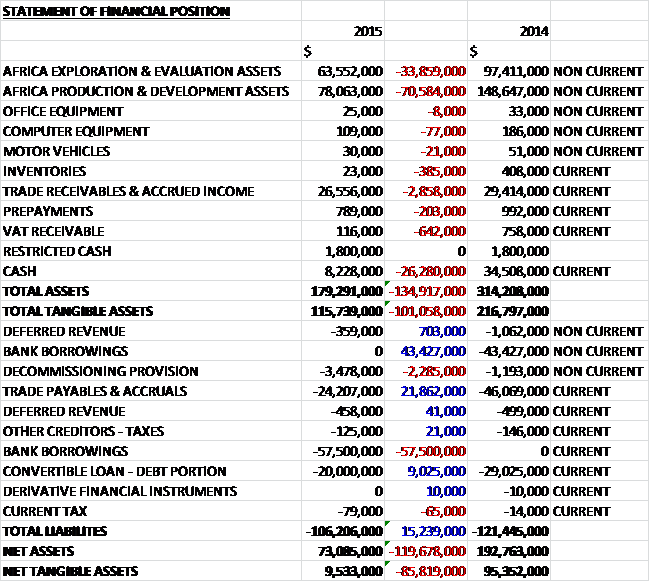

Before movements in working capital, cash profits declined by $22.6M to $21.2M. There was a cash inflow from working capital, in particular a fall in receivables, although this was less pronounced than last year which meant the net cash from operations was $26.8M, a decline of $29.4M year on year. The group spent $28.2M on production and $21.1M on exploration which meant that before financing there was a cash outflow of $22.5M. In addition the group forked out $4.9M on interest which meant that there was a cash outflow of $26M and a cash level of just $10M at the year-end.

Total net production for the group was 1.58MMboe made up of 1.08MMbo and 1.29bcf from Egypt and 1.61bfc (227K boe) from Morocco. Production in Egypt averaged 2,970bopd, 3.54MMscf/d and 3,581boepd and there was an average gas production of 4.39MMscf per day and 757boepd in Morocco. Egypt operating cost was $5.22 per barrel and in Morocco operating costs were 85c per Mcf. The average realised oil price fell from $94.8 per barrel last year to $48.27 per barrel in 2015 and in Morocco, the average realised gas selling price fell from $10.12 per Mscf to $8.64 per MScf.

The group have completed a competent persons report on the status of reserves. The report showed that the 2P gross producing and undeveloped reserves were estimated to be 18.04MMboe or 7.65MMboe net to the group compared to a net 16.2MMboe at the end of last year. In addition, the P50 gross unrisked contingent resources are estimated at 5.644MMboe (2.81MMboe net to the group).

In Morocco the predominant theme during the year was reduction of the operational cost base. Service contracts were terminated and replaced or renegotiated to make use of lower cost providers. The drilling rig contract was not extended beyond the minimum period with a view to conserving cash and taking advantage of lower day rates for future campaigns. Staff numbers have been gradually reduced and a restructuring commenced to ensure more efficient operations over the next year.

In the currently lapsed Oulad N’zala concession which was not producing at the year end, discussions are advanced to apply for a new exploration permit in the Sebou area which could include all or part of the old Oulad N’zala concession and it would be anticipated that Circle would have a 75% working interest in such a permit.

Gross gas production averaged 5.85MMscf per day throughout the year. They started the year supplying three companies in the Kenitra industrial zone but the smallest of these, Keyes-Cemok, ceased trading at the end of January. The two remaining customers regularly take more gas than the minimum contracted and have both been keen to extend or increase consumption pending negotiations of further contracts with other parties. Total sales to the CMCP paper factory are now in excess of 4.71bcf and to Super Cerame they were 5.46bcf.

The third Sebou drilling campaign recommenced in February 2015 with well KAB-1bis, a red-drill of the KAB-1 well which had failed to log the target anomaly due to mechanical difficulties associated with the geology. Unfortunately the results confirmed an anomalous time/depth relationship and the expected anomaly was intersected close to a fault cut. The remaining gas potential up-dip of the fault is anticipated to be too small to be economic. Drilling then moved to the Lalla Mimouna block where the first well LAM-1 intersected the objectives close to prognosis and an unexpectedly thick sand sequence at its base. Subsequent test results provided good natural glows to surface but were not as promising as expected in terms of indicated volumes and the well was suspended for further analysis and potential workover.

The second well, ANS-2, also encountered the anticipated anomaly levels which were found not to yield good wireline pressure readings and the well was suspended for further investigation at a later date. The third well, NFA-1, targeted a larger, shallower, but weaker anomaly class and did not encounter the expected anomaly sands. The rig was then moved back to Sebou and drilled an exploration well targeting a new anomaly type at KSS-A. This well was abandoned for mechanical reasons without reaching the objective. The following two wells, CGD-13 and KSR-A were successfully drilled, tested, and put on stream, also completing the suspended SAH-W1 well adding at least 1.2bcf to reserves. KSR-A, being an additional well to the first submitted Sebou programme was allowed against the commitment to drill six wells in Lalla Mimouna.

The commercial environment for further gas contracts in the Kenitra area is good for both traditional ceramic and other industries and newly arriving companies in the Atlantic Free Zone adjacent to the pipeline. SBS Porcher has already signed an MOU to take a new gas contract, and other companies are in discussions with demand providing upward pressure on any new prices. For the future a planned Peugeot assembly line or its suppliers could also use natural gas rather than bottled propane for part of their operations.

In Egypt, as with Morocco there has been a drive to reduce the cost of production in the non-operated fields in the country. The operator has responded to the reduction in the oil price by repatriating some staff and reducing local staff costs. Capex has been reduced by delaying the planned drilling campaign and reducing from three firm and operational additional wells to two firm wells, one of which was started in December. Essential workovers and maintenance has continued, however, in order to maintain production as the field matures and water front advance/reservoir pressure maintenance require appropriate interventions.

The gross remaining 2P reserves are 16.68MMboe with an additional contingent 2C resources of 3.74MMboe. About 87% of the reserves are in AASE. Gross production from 2009 to the end of 2015 was 20.4MMbo and 22MMscf of gas. During the year total sales of gas were 9.45MMScf with 91,005bbls of condensate and 20,201 tonnes of LPG. Gross production averaged 7,426bopd an 8.86MMscf per day of wet gas. Processing of the produced gas provided 67bpd of condensate, 15 tonnes of LPG per day and 7,009MMscf per day of dry sales gas.

Seven workovers were conducted during the year, three production zone switches, one conversion to injector, and three ESP maintenance interventions. One recompletion was unsuccessful. No new wells were drilled but the two well campaign that started in December has been completed after the year-end. AASE-23 has encountered a fault and was sidetracked to the reservoir, flowing at over 4,000bopd on test before being put into production at 740bopd in January. AASE-24 also encountered a fault and the sidetrack found both reservoirs. The well flowed at over 1,700bopd on test and commenced production at 490bopd in May. A further programme of workovers is underway since the year-end.

In Tunisia exploration activities have been minimal. The costs of necessary seismic acquisition and drilling fell during the year making it challenging to know when best to undertake remaining commitments.

In Mahdia permit work was completed on the analysis of the El Mediouni-1 well which encountered light oil shows through a 133 metre section of Ketatna carbonates. Formal government approval was granted for an extension of the permit through January 2018, with a work commitment of two further wells and 300km2 of 3D seismic. Further technical work was undertaken by the company to formulate future work plans and development scenarios. The work indicated that based on management assumptions, the development of the Mahdia prospect would be economically feasible at existing oil prices. A farm out process on the block was initiated in late 2015, but has since been superseded by the strategic review process.

Tender processes were conducted for a 3D survey on the Beni Khalled concession. These were inconclusive in the light of falling rates for the seismic and the uncertainties in sharing mobilisation for a survey of less than 60km2. Efforts to finalise an award for conduct of this work continue in the coming year. The Bir Drassen gas discovery on this concession tested at 23.5MMscf per day of gas and 28bcpd in 1991. At the time this was not of commercial interest. The Beni Khalled field, discovered in 2004, initially produced at 550bopd but it is currently produced sporadically according to the prevailing price and usually yields less than 80bopd.

On the Ras Marmour permit, the location for a well on the Isle of Djerba, originally planned to be drilled in 2014, has been the subject of disputes due to changing legislation and the permit is currently considered to be in Force Majeure while these issues are being resolved.

In Oman, at the start of the year the group operated onshore exploration block 49 and offshore exploration block 52. During the year the decision was taken to relinquish both interests in order to minimise future exploration commitments and a managed withdrawal was completed within the year. This was an inevitable process in the light of the prevailing oil price, lack of proven success and lack of time to complete further commitments when resources might become available. During the year the group drilled the Shisr-1 exploration well on block 49. The well was operating until February 20th. During the 8.5” section losses occurred in the carbonate section and the drill assembly became stuck and was abandoned in the hole after unsuccessful fishing attempts. The well was plugged and abandoned to avoid excessive cost overruns and the failure of this well made relinquishment inevitable.

In February 2016 the group announced the signing of a MoU with SBS Porcher whereby Porcher would pay for the construction of a pipeline extension to central Kenitra and off-take a minimum of 0.35MMscf per day at a price of $12/MMscf representing a substantial increase in current prices and an additional 6% of annual production volumes.

During the year there was an impairment of $21M on the carrying value of the NW Gemsa permit in Egypt, caused primarily by the fall in the oil price and the new reserves figure. The impairment on the carrying value of the Sebou permit in Morocco is $46.7M.

At the year-end there was $13.4M of receivables relating to amounts due from the EGPC of which $10.8M was overdue.

In April 2015 the convertible loan was extended for two years. Under the terms of this agreement, the group repaid $10M to KGL bringing the overall loan amount down to $20M. The interest rate was increased to 8% per annum plus a payment in kind fee and the conversion price was reduced to 13.6p per share.

At the end of the year the total loan commitments under the reserve based lending facility amounted to $67.5M with an interest rate of up to 5.5% plus LIBOR. In June the IFC advised that the borrowing base amount was to be substantially reduced from the $67.5M then available and the discussions with the IFC have culminated in the group signing a waiver letter that suspended the redetermination process and postponed any principal repayments due, and required them to undertake a strategic review process. This current waiver expires on 22nd July.

After the year end, the group’s financial position remains under significant pressure given the unpredictable and infrequent payments from EGPC. As a result, the group requires additional funding during July in order to be able to discharge its financial obligations from August. The strategic review process is ongoing but the directors believe that it is likely that there will be no value attributable to equity holders at the end of the review.

The auditors consider that the directors have not taken adequate steps to satisfy themselves that it is appropriate for them to adopt the going concern basis because the circumstances of the company and the nature of the business require that such information be prepared and reviewed by the directors and auditors for a period of at least twelve months from the date of approval of the financial statements. Consequently it was not possible to obtain sufficient appropriate audit evidence regarding the use of the going concern assumption in the preparation of the financial accounts and the auditors do not express an opinion on the financial statements.

At the year-end, the group had an unrestricted cash level of $8.2M and net debt was $67.5M, which increased to $69.6M by the end of May 2016.

Overall then, this has been a desperate year with the high debts the company has racked up, along with some failures with the drill meaning that they have been unable to deal with the decline in the oil price. The board have stated that there is likely to be no value attributable to equity holders in the end so until the review is over and financing has been sorted, there is no point looking at this company as an investment.