Cohort has now released its final results for the year ended 2016.

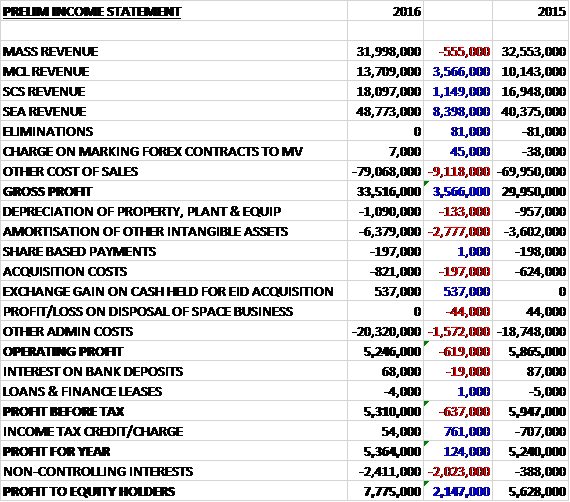

Revenue increased when compared to last year as a £555K decline in MASS revenue was more than offset by an £8.4M growth in SEA revenue reflecting a full year contribution from J&S and increased revenue on submarine projects, a £3.6M increase in MCL revenue reflecting a full year contribution rather than ten months last year and a £1.1M growth in SCS revenue. Cost of sales also increased to give a gross profit £3.6M above that of last year. Amortisation grew by £2.8M and acquisition costs grew by £197K but there was a £537K exchange gain on cash held for the EID acquisition and after a £1.6M increase in other admin costs, the operating profit declined by £619K. There was a £761K positive swing to a tax credit, however, which included a one-off tax credit of £900K, and a £2.4M loss attributed to non-controlling interest which gave a profit for the equity holders of £7.8M, an increase of £2.1M year on year.

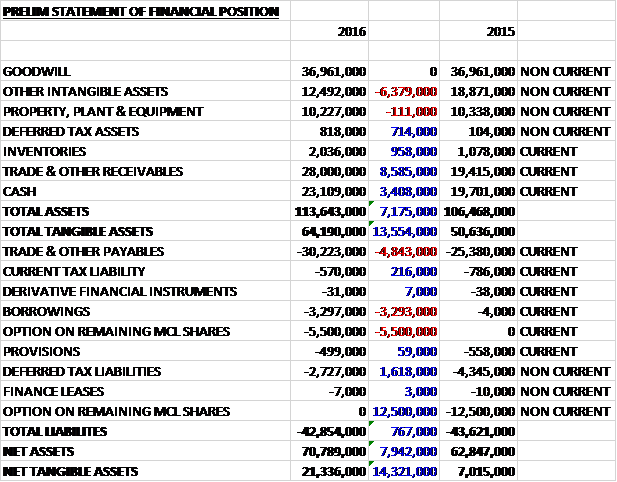

When compared to the end point of last year, total assets increased by £7.2M to £113.6M driven by an £8.6M growth in receivables, a £3.4M increase in cash and a £958K increase in inventories partially offset by a £6.4M decline in other intangible assets. Total liabilities declined during the year as a £7M fall in the option remaining on MCL shares and a £1.6M decline in deferred tax liabilities was partially offset by a £4.8M growth in payables and a £3.3M increase in borrowings. The end result was a net tangible asset level of £21.3M, a growth of £14.3M year on year.

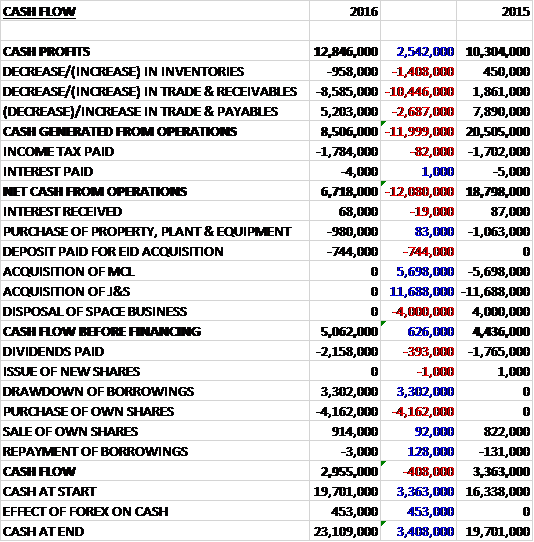

Before movements in working capital, cash profits increased by £2.5M to £12.8M. There was a cash outflow from working capital, with a large increase in receivables, and after tax and interest remained broadly flat, the net cash from operations came in at £6.7M, a £12.1M decline year on year. The group only spent £980K on capex and £744K as a deposit for the EID acquisition so there was free cash of £5.1M generated. This was used to pay £2.2M of dividends and to purchase £4.2M of their own shares to satisfy share option awards (this seems like a lot!) and after a £3.3M drawdown of borrowings, the cash flow for the year was £3M to give a cash level of £23.1M at the year-end.

The adjusted operating profit for the MASS division was £6M, a growth of £464K year on year despite a fall in revenue reflecting lower levels of activity in education. This was offset by work in Electronic Warfare and Strategic Systems. The support contract for NATO joint EW Core Staff, originally secured in 2014, was extended for a further year. As well as being a valuable work stream, this provides the division with further opportunities to access NATO customers with its EWOS and THURBON offerings.

After a strong operating cash flow last year, this year it was slightly weaker with a build-up of working capital linked to higher activity. As part of its cyber strategy the business is currently investing in facility upgrades to enable it to offer a more comprehensive service. This work will be completed in the summer of 2016 and will enable it to continue to grow its business in this area.

Looking forward the board expect the operating margin to fall back to a slightly lower level as the business grows its cyber offering. Although the cyber opportunities available to the business are substantial and growing, a larger part of this activity has bought in content. The order book reduced during the year as the business delivered on its longer term orders, a number of which are due to be replenished in the coming year. Its closing order book of £41.7M represents an £11.7M decline.

The adjusted operating profit for the MCL division was £1.4M an increase of just £77K when compared to last year despite this being the first full year contribution from the division with a ten month contribution last year with a lower net margin due to a higher proportion of bought in product and less support work in the revenue mix. The growth came from deliveries of hearing protection systems for the British Army. The business benefitted from a strong Q4 from its main customer, the MOD, despite evidence that it was under some budgetary pressure. Its strong order book of £7M, up from £2.8M at the end of last year, and pipeline of prospects give the board confidence of progress in the coming year.

The adjusted operating profit for the SCS division was £1.3M, a decline of £69K when compared to 2015 with an increase in the proportion of lower margin work following the end of several profitable projects. Training activity at the joint warfare centre increased following the end of the UK’s operations in Afghanistan but the withdrawal also resulted in the end of an in-country support contract which has reduced the margin achieved overall.

The business secured a further two years with a potential to go out to March 2020, of its high level training offering to the UK’s Joint Warfare Centre, a service they have provided for over 15 years. This capability forms the core of the business and has enabled it to win further customers in the UK and overseas. In other areas of the business, there was a mixed performance. It was unsuccessful in renewing its framework contract with NATO although it has continued to win revenue from them, albeit at a slower and lower rate. In Air Systems, the business continued to deliver its independent Technical Evaluation services for a number of air platforms.

Although the business enters the coming year with an increased order book of £11.7M its short term prospects are not as strong as elsewhere in the group and the performance of the business is expected to remain flat with an anticipated fall off in Air Domain activity in the coming year.

The adjusted operating profit for the SEA division was £5.4M, an increase of £1.5M year on year which included a full year contribution from J&S compared to seven months last year. The business is now fully integrated into the division and efficiencies realised have increased the net margin from 9.9% to 11.1%. Although the bulk of the increase in revenue was due to the prior year acquisition, the underlying business also increased its revenue by over 11% driven mostly by activity on the Common External Communications System for the UK’s submarine fleet, particularly on the Vanguard class. The project will move into its delivery phase in the coming year so will have lower engineering activity with the delivery of completed ship systems at a steady but lower run rate. With critical design milestones achieved in the year, however, they expect to see an increasing contribution of profit from the naval systems export work.

The research business had a steady year, including completing the Delivering Dismounted Effect programme for DSTL. Looking forward, they don’t expect any growth in the short term but the pipeline for 2018 and beyond looks good. The division’s transport activity was slightly down on last year but within this Roadflow sales grew considerably. Prospects in the UK market for Roadflow, particularly in the Red Light and Motion variants, along with further export opportunities give the board confidence that transport activity will grow in the coming years. The sale of Red Light systems for level crossings has been slower than hoped, mainly due to customer delays and they expect this to pick up going forward.

The Subsea engineering business, which primarily services the North Sea oil and gas market, had a very challenging year due to the poor market. The apparent growth in revenue was mostly due to the recognition of a full year’s trading compared to only seven months in 2015 but the business, which is mainly involved in operational support, remained profitable and any sustained improvement in the oil price should enable it to start growing again.

The division secured over £36M of orders in the year against a very strong 2015 comparator of £50M which included a number of large CECS orders which are being delivered now and into the future. The order book of £55.6M, a decline of £12.4M but underpins over half of the expected revenues for next year. The research and technical support division enters the coming year with lower order cover compared to recent years. It has recently completed its Delivering Dismount effect programme and is waiting for the replacement project, the Dismounted Engine Room, which will start later in the year. The division has a number of long term contracts due for renewal in 2017.

The order intake for the year at £94.8M was, as expected, lower than the strong performance seen last year at £114.3M and accounts for the lower closing order book of £116M compared to £134M at the end of 2015.

The acquisition of MCL included an option for the purchase of the remaining 50% of shares. This is exercisable by December 2016 and is capped at £12.5M which was the value of the option reported at the time of the acquisition. It has now been revalued and is estimated at £5.5M with payment expected before the end of 2017.

In August the group announced that it had signed a sale and purchase agreement to acquire EID for a cash consideration of €19M (£15M at the year-end point). At the time of the announcement the group paid a deposit of £744K. The acquisition is now expected to complete in two stages with the group acquiring 57% In June and a further 23% before the end of October. This will leave the group with 80% of the business with the Portuguese government owning the remaining 20%. On acquiring the 23% from the government, a shareholder agreement will be put in place between them and the group giving some strategic protection to the government whilst enabling Cohort to run the business day to day.

Although the UK defence market remains tight, the group has established itself on some key long term MOD programmes with a good pipeline of new opportunities. Export prospects continue to strengthen, particularly in SEA. Outside the defence market, MASS continues to make progress with its cyber capability and the board expect the order intake for the coming year to be stronger with a number of key long term renewals due.

It is too early to quantify the impact of the recent referendum result. This year, only £1M of revenues came from EU nations. The vast majority of the group’s business in Europe is with NATO and the UK’s exit from the EU is not expected to affect this market. The operation of EID provides the group with a long term operating platform within the EU. Any short term impact is likely to be driven by changes to UK government priorities and possibly spending in the aftermath of the referendum.

At the current share price the shares are trading on a PE ratio of 18.8 but this falls to 13.2 on next year’s consensus forecast. After a 20% increase in the total dividend, the shares are yielding 1.7%, increasing to 2% on next year’s forecast. At the year-end the group had a net cash position of £19.8M, broadly the same as at the end of the prior year but they paid for much of the EID acquisition after the year-end.

On the 28th June the group announced that it had acquired 57% of EID for a consideration of £8.9M from existing shareholders EFACEC Capital and Rohde & Schwarz. The group have agreed in principle to acquire a further stake from two agencies of the Portuguese government on the same terms so that their final holding in EID will be 80% at a total cost of £12.5M. Timing and completion of this further transaction is dependent on the necessary approvals from the government. The business will become a fifth operating division of the group and is a cash generative business with a strong order book so the acquisition is expected to be earnings enhancing in 2017.

Overall then this has been a decent year for the group. Profits increased, net assets were up and although the operating cash flow declined, this was due to adverse working capital movements and cash profits increased with decent free cash being generated, although the share purchases for reward schemes look very high. The MASS business performed well, with a better mix of product and the SEA division also showed good growth with five extra months of contribution from J&S along with an increase in UK submarine communications work, although this is likely to reduce somewhat going forward.

The MCL division performed less well, although the two extra months of contribution meant there was a modest increase in profits whilst SCS saw a decline due to the end of operations in Afghanistan and the loss of a NATO framework contract. The closing order book saw a marked decline, which is a bit of a concern and there will be some chunky cash payments in the coming year due to the EID and MCL acquisitions. The forward PE of 13.2 looks decent enough but the 2% yield is nothing to get excited about. I am not sure about this company, most divisions are performing well but the drop in the order book and likely large cash outflow next year give me cause for concern.

On the 25th July the group announced a contract win. MCL has been awarded the UK MOD Airborne Tactical Communications support contract. This contract is valued at up to £7.7M and is to provide support to certain specialist equipment and includes options covering additional development activities. Its duration will be between two and six years with a minimum value of around £900K depending on the options chosen by the customer. After many years delivering land based tactical communications. This is the first win in the tactical airborne environment.

On the 13th September the group released a Q1 update. The order book stood at £128M as of the end of August and the pipeline of orders beyond this along with the expected revenues, give the board confidence that the overall performance for the year will be in line with expectations, despite SCS’s market in technical consultancy remaining a challenge.

The net cash at the end of August stood at £14.4M with the reduction since the year-end stemming from the partial reversal of working capital inflow during a very strong Q4 last year. A further £9M is expected to be spent in the rest of the year in acquiring a further 23% of EID, taking the holding up to 80%, and the remainder of the shares of MCL, taking the group’s holding up to 100%.

This all seems fairly decent to me.

On the 11th October the group announced a reorganisation of SCS following increased challenges in its markets. The intention is to integrate the business’ Air Systems and Capability Development divisions into the SEA business, and its Training Support and Information along with the Communications Systems division into MASS. As a result, it is expected that SCS will no longer operate as a standalone subsidiary. An exceptional cost of £2 is expected to be incurred in the current with a predicted annual cost saving of around £1.6M.

On the 17th October the group announced that MASS has been awarded a nine year extension to its managed IT service contract for the Sentry Whole Life Support Programme at RAF Waddington. Valued at around £12M, the scope of the support contract now includes replacement of the maintenance, repair and overhaul software and adds an Enterprise Performance Management solution.

On the 7th November the group announced that SEA had been awarded contracts by TFL to further develop and provide ongoing support of its Digital Traffic Enforcement System and to develop and support a Parking Enforcement Solution mobile app. The combined orders are valued at around £7M and include ten years of support for both systems. SEA originally developed the DTES system on behalf of TFL which entered into service in 2009 and they have provided support over that entire period.