Cohort has now released their final results for the year ended 2018.

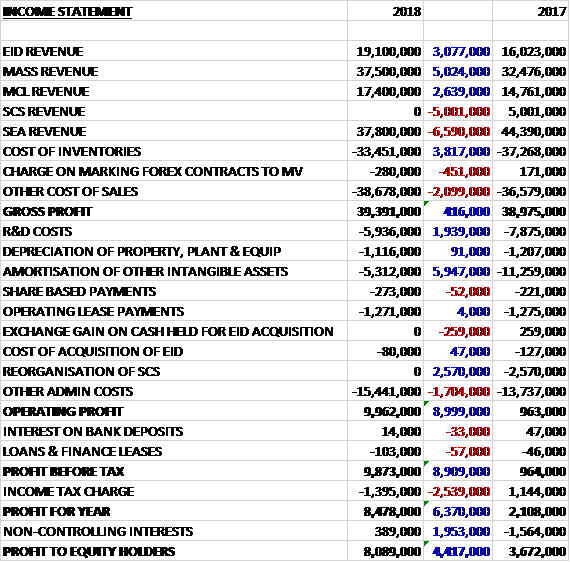

Revenues declined when compared to last year as a £5M growth in MASS revenue, a £3.1M increase in EID revenue and a £2.6M growth in MCL revenue was more than offset by the £5M reduction in SCS revenue and a £6.6M fall in SEA revenue. Cost of inventories declined by £3.8M but other costs of sales increased to give a gross profit £416K higher. R&D costs fell by £1.9M, amortisation reduced by £5.9M and there were no reorganisation costs, which were £2.6M last year. Other admin costs rose by £1.7M but the operating profit increased by £9M. There was a modest increase in finance costs and the tax charge increased by £2.5M to give a profit for the year of £8.1M, a growth of £4.4M year on year.

When compared to the end point of last year, total assets declined by £1.3M driven by a £5.1M decline in trade receivables, a £5.3M fall in intangible assets and a £1.5M decrease in the amounts recoverable under contracts, partially offset by an £8.5M increase in cash, a £2.1M growth in prepayments and accrued income and a £1.1M increase in inventories. Total liabilities also declined during the year as a £5.6M growth in the bank loan and a £2.4M increase trade payables and accruals was more than offset by an £8.1M decrease in accruals and deferred income and a £1.1M decline in deferred tax liabilities. The end result was a net tangible asset level of £32.8M, a growth of £5.4M year on year.

Before movements in working capital, cash profits increased by £2.9M to £16.4M. There was a cash outflow from working capital but this was much less than last year and after tax payments reduced by £807K the net cash from operations was £13.2M, a growth of £12.6M year on year. The group spent £747K on capex, £3.5M on the EID acquisition and £2.5M on deferred consideration on the MCL acquisition which meant that the free cash flow was £6.4M. The group spent £1.5M buying their own shares and paid out £3M in dividends so after a drawdown of a further £5.5M on the loan the cash flow was £8.2M and the cash level at the year-end was £20.5M.

The operating profit in the EID business was £4.7M, a growth of £443K year on year. Although the board expected the net margin to fall, driven by less naval support work, the outcome for the year was better than expected with some higher margin R&D projects. The order intake of £8.9M included a significant order for upgrading a class of Portuguese patrol vessels. The order was lower than expected, however, with some important orders for the Portuguese army slipping into the coming year.

The closing order book of £18.2M provides some good underpinning to the coming year in the Naval division and some good prospects, particularly in the tactical systems division. The board expect the business’ revenue to grow in the coming year. The mix of work at the business is expected to change with lower levels of naval support activity and increased deliveries of intercom and radio products. The latter generate a lower margin so margins are expect to fall to around 20%.

The operating profit in the MASS business was £7.1M, an increase of £1.2M when compared to last year with revenues increasing by £5M. The inclusion of the training support division from SCS contributed £2M of revenues. In April 2018 the business completed a large biennial joint forces exercise, increasing margin and revenue for the year. The other main growth driver was the higher level of cyber activity, including initial deliveries of the digital forensics services to the Met police and the completion of several cyber vulnerability investigations.

This offset a decline in EWOS work. A countermeasure project for an export client finished early in the year and the Shepherd development project came to an end in the year. Shepherd is now entering its five year support phase and the board expect to secure extra tasking in the coming years. Some long term export EWOS activities continued to be funded on short term, lower value rolling purchase orders, while the prime contractor worked to finish the lead contract. They expect to see these support contracts secured at their full long term value in the coming year.

The business’ net margin increased slightly to 18.9% due to higher margins in cyber and only slight increases in overheads. The order intake was slightly lower than last year which included two long term contracts which were mot repeated. The most significant order in the year was a two year extension of the joint forces command support for £10.5M. Other orders included £6M in cyber and £10M in EWOS.

The business enters the current year with a strong order book and pipeline of opportunities including exports and renewals. They will see the conclusion of their current long term contract with the UK MOD, supporting the UK’s strategic defence capability. The MOD is holding a competition for the follow on contract with a decision expected in the autumn.

The operating profit in the MCL business was £2.1M, broadly flat with an increase of just £19K with revenues increasing by 18% due to increased deliveries of hearing protection systems to the UK MOD, which has a lower margin than some of the other work. Overheads increased somewhat due to an increase of work force and higher levels of overseas supplier activity. The business secured several key contracts in the year including a further £6M of orders for hearing protection systems and other equipment development, production and support for specialist military users. The order book has slipped back somewhat, which is viewed as temporary.

The operating profit in the SEA business was £4.4M, a decline of £861K when compared to 2017 with revenues falling by £6.6M. The business had another challenging year with growth in its maritime export deliveries and a return to growth of its research activity more than offset by a significant contraction in its submarine activity.

This trend has been accompanied by reduced revenue predictability as the revenue generated by long term contracts has declined. This is expected to continue in the medium term while they await the next major ECS contract which will be to provide the system for the new Dreadnought class of ballistic missile submarines. In the meantime the business is seeking to expand its export business, especially in maritime markets.

In the maritime division the UK submarine communications work moved in 2016/17 from design and testing of systems to delivery. During the year, the level of work dropped further with minimal deliveries of systems and the ongoing design work now mainly in respect of technical developments and upgrades. Activity is expected to remain at this low level for the next two years until significant Dreadnought class work starts, which is currently expected in 2020. Good progress on the communications system development work has significantly de-risked the programme, allowing contingency to be released.

Excluding Submarines, SEA’s maritime business grew. The level of torpedo launch systems was above that of last year with delivery completed for one customer, continuing for a second and starting for a new third customer. They expect a marketed increase in this work in the coming year as the two customers receive systems. Within the maritime division the business suffered further losses on a one-off development project for a specialist sonar array, a contract inherited with the J&S business acquired in 2014. This programme is now almost complete, and no further loss is expected.

SEA’s SSP division increased revenue somewhat, mostly derived from increased orders for traffic enforcement systems and other defence products. Total transport revenue dropped slightly as the delivery of the upgrade to TFL for its digital traffic enforcement systems fell following peak activity in the second half of last year.

Improved margins in the maritime, research and SSP divisions, along with volume increases partly offset the marked deterioration in submarine activity. Following the fall in activity at the research division over the past two years, the business secured a new contract to carry out research into soldier systems, the Future Individual Lethality System. As a result, revenue has stabilised and they expect it to increase in 2019, although not back to the peak levels of three years ago.

SEA’s subsea division saw its revenue increase by around 5% and its profitability maintained despite the low oil price holding back spending by oil producers in the North Sea. The gross margin stayed high due to the proportion of refurb and repair activity. The division absorbed the former SCS divisions of capability development and air systems last year which added £1M to revenues. The closing order book of £33.1M included nearly £16M of revenue to be delivered in the coming year.

Following two years of declining revenue and profitability, and in the expectation that SEA’s submarine activity will remain low in the near term, the group have acted to reduce the cost base of the business by around £1M per annum. This restructuring, costing £500K, has already started and will complete in the first half of 2019, delivering an expected saving of £800K in that year.

The decrease in the group’s order intake was across the group. This was partly due to slippage of some significant renewals into the current year, especially at MASS. The falls at EID and MCL were to some extent expected, with large orders for naval systems and hearing protection having been received in 2017. SEA’s order intake was also down, primarily in submarine activity, but they did see another good export win for their torpedo launch system.

The SCS business was discontinued having made an operating loss of £455K last year.

In August 2017 the group paid £2.5M as the final settlement of the earn out from the MCL acquisition and in November they paid £3.5M for a further 23% of EID, taking their holding up to 80%. EID contributed £4.7M of the operating profit for the year.

Going forward, the political and economic context within which the group operates has not changed much since last year. On the one hand the security environment calls for greater resources to be devoted to defence and counter terrorism but on the other hand the pressures on public expenditure in the UK are strong. Although the UK defence market remains tight, MASS continues to make progress with its cyber capability and SEA with its Road Flow product range. They have begun to introduce their wider product range in the new markets brought to the group by EID. Lower order intake was mainly due to delays rather than losses or a lack of opportunities and the closing order book provides a reasonable underpinning for the current year.

There are several important long-term opportunities that are likely to be decided in 2019 and will have a major impact on the group’s prospects for growth. The renewal of a major support contract for MASS, the MOD is conducting a competition to select the supplier; further export EWOS contracts for MASS, particularly for the supply of countermeasures and the provision of local support in the Middle East; a large opportunity for EID to supply vehicle intercom systems to a customer in the Middle East; an extension of MCL’s contract to provide tactical intelligence gathering equipment to the Royal Navy; several competitive opportunities for SEA to provide its Torpedo launch system for export customers and to supply communications equipment to the Royal Navy’s Type 31 Frigate.

At the current share price the shares are trading on a PE ratio of 20.5 which falls to 12.9 on next year’s consensus forecast. After a 15% increase in the dividend the shares are yielding 2% which increases to 2.3% on next year’s forecast. At the year-end the group had a net cash position of £11.3M compared to £8.5M at the end of last year.

Overall then this has been a rather mixed year but overall fairly positive. Profits increased, mainly due to lower costs. Net assets grew and the operating cash flow improved with some decent free cash being generated, despite the deferred consideration payments made. The EID and MASS business both performed well, although margins are expected to lower at EID. The MCL business struggled a bit, although the hearing protection work seems to be going well. The real drag was SEA which saw lower profits due to less submarine work, with little prospect of this changing over the medium term.

The forward PE of 12.9 and yield of 2.3% looks OK given the net cash position. I do think this company is actually performing well but the question remains over the lower order books and general malaise in some of the end markets. A tricky one this, prudence should dictate staying out but I like the company.

On the 8th October the group announced that SEA had been awarded contracts worth more than £3M by Network Rail to supply and install its Metro Red Light enforcement system at selected level crossing sites. The system uses video analytics to detect and capture evidential images and video of any vehicle which crosses a level crossing while the red lights are activated. Under these contracts the business will deliver and install over thirty systems.

On the 25th October the group announced that MASS has been selected as preferred bidder for an eight year contract valued at over £50M following a highly competitive tender process. Under the contract, they will provide in-service support for the UK MOD including operational analysis studies, IT infrastructure management modelling and simulation and software engineering. This is a continuation of work undertaken since 2000. The contract will run until March 2027.

On the 3rd November it was announced that MASS had been awarded a £3.2M 18 month contract to provide business analysis support for the MOD.

On the 13th November it was announced that EID had been awarded two contracts to supply vehicle intercom systems valued at a total of €11M. The contracts are for supply to existing export customers and deliveries will take place over the next two years.

On the 20th November the group announced that SEA had been awarded a follow on five year contract by an existing customer worth £5.4M to support maritime equipment for the Royal Navy.