Cohort has now released its interim results for the year ending 2017.

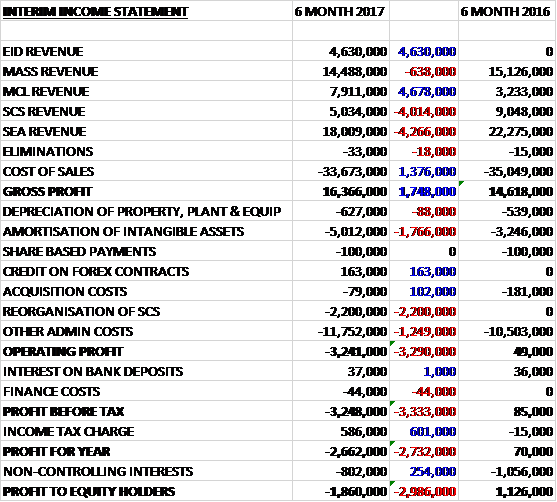

Revenues grew when compared to the first half of last year as a £4.7M growth in MCL revenue and a maiden £4.6M contribution from EID was partially offset by a £4.3M decline in SEA revenue, a £4M fall in SCS revenue and a £638K decrease in MASS revenue. Cost of sales declined to give a gross profit £1.7M ahead of last time. Amortisation charges grew by £1.8M and there were £2.2M of charges relating to the reorganisation of SCS which, along with a £1.2M growth in other admin costs, meant that the operating profit loss saw a £3.3M detrimental movement. The income tax rebate (relating to deferred tax) represented an improvement of £601K, however, to give a loss for the period of £1.9M, a detrimental movement of £3M year on year.

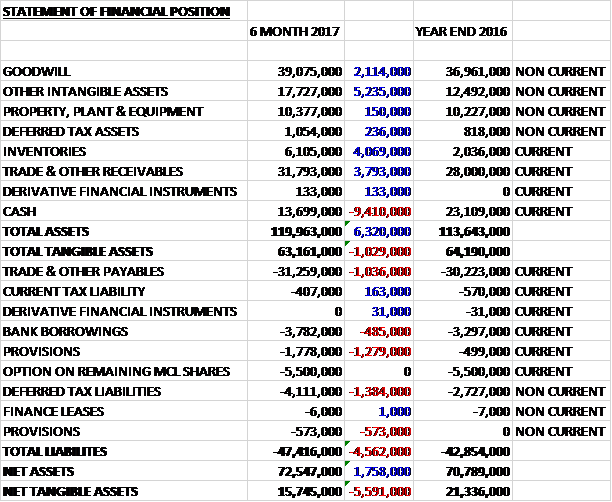

When compared to the end point of last year, total assets grew by £6.3M driven by a £2.1M rise in goodwill, a £5.2M increase in other intangible assets, a £4.1M growth in inventories and a £3.8M increase in receivables, partially offset by a £9.4M decline in cash levels. Total liabilities also grew during the period due to a £1.4M rise in deferred tax liabilities relating to the EID acquisition, a £1.9M increase in provisions and a £1M growth in payables. The end result was a net tangible asset level of £15.7M, a decline of £5.6M over the past six months.

Before movements in working capital, cash profits declined by £1.9M to £2M. There was a large cash outflow from working capital, but less so than last year and after tax payments increased by £455K, the net cash outflow from operations was £4.3M, an improvement of £1.3M year on year. The group spent £456K on capex and £4M on the acquisition of EID to give a cash outflow of £8.8M before financing. The group then spent £1.7M on dividends to give a cash outflow of £10.2M and a cash level of £13.7M at the period-end – not a sustainable situation.

Adverse market conditions at SCS and delayed customer funded research work at SEA resulted in a weaker like for like group performance with the trading profit down 29% excluding the impact of EID.

The EID division contributed a maiden operating profit of £1.4M in the four months that it has been a part of the group. This strong performance resulted from long-term projects for various European navies and continued delivery of tactical communications systems for export customers including Egypt and Australia. Since acquisition, the business has secured nearly £5M of orders including £2.6M from its domestic customer, giving confidence in a strong second half.

The operating profit in the MASS business was £2.4M, broadly flat year on year with a £28K increase with electronic warfare countermeasures and software development work replacing education and other relatively low margin revenue. The business continues to grow its cyber offering with revenue in this market increasing by £1M to £3.4M. The business continues to be a key supplier to the UK MOD in a number of important strategic areas and this was recently underlined by the extension of its contract to support the Sentry air platform for a further nine years with a value of £12M. Of the closing order book of £43M, £11.7M is deliverable in the second half of the year which gives the board confidence it will have a stronger second half to the year.

The operating profit in the MCL division was £753K, a growth of £734K when compared to the first half of last year. The improved performance was a result of the delivery of Tactical Hearing Protection Systems to the British Army which started in the second half of last year. A further order has now been secured to extend deliveries to the end of the year and they expect follow-on orders to continue for some time thereafter.

MCL has continued to be a key supplier to the UK’s Special Forces and related agencies and has seen increased activity from these customers. Its strong position in this market was reinforced by the securing of a contract to design, develop, build and support an Airborne Tactical Communications System with an eventual value expected to be over £7M. As in the past, MCL’s performance is expected to be weighted to the second half and its closing order book of £4.5M, almost all of which is deliverable this year, along with a pipeline of opportunities that includes further hearing protection contracts, gives them confidence that the business will deliver a stronger second half.

The operating loss in the SCS business was £455K, a detrimental movement of £758K year on year. The division will be reported as part of MASS and SEA going forward. This performance reflects challenging market conditions and the loss of one of its air system contracts in a competitive renewal process.

The operating profit in the SEA division was £1M, a decline of £745K when compared to the first half of 2016 relating to reduced activity in the research division and the timing of deliveries of larger maritime projects. In the research division, following completion in March of a four year research programme, Delivering Dismounted Effect, the expected follow-on programme has been delayed by the customer until the end of this year. As a result there has been a sharp fall-off in activity levels that will persist into H2.

The closing order book of £45.8M includes £19.5M of revenue to be delivered in the second half, a significant proportion of which is higher margin maritime systems work for export customers. The pipeline of opportunities and the recently announced renewal and extension of the DTES solution for TfL gives the board confidence that the business will have a stronger second half. Challenges remain in the offshore energy market where the low oil price continues to put pressure on customer spending, although SEA’s activity in this area is continuing to generate profitable revenue. Overall they now expect SEA’s performance for the full year to be similar to last year.

Order intake for the first half was £37.1M excluding the acquired order book of EID (£23.1M) compared to £55.7M at this point of last year. The order intake in the first half was lower than last year with a number of contracts that had been expected to be renewed slipping into the second half. Some of these renewals are included in nearly £16M of orders received since the period-end. These include the nine year, £7M, DTES support contract for TfL, an order to extend elements of the Common External Communications System to the Royal Navy’s Trafalgar class subs and a number of longer term support contracts.

In June the group acquired a controlling interest in EID of 57% for a total of £5.2M, generating goodwill of £2.1M, and they have agreed in principal with the Portuguese government to increase their holding to 80% on the same terms and at the same Euro valuation. They expect the cash consideration for the additional 23% to be around £3.5M. In connection with this transaction, they have agreed terms of a shareholders agreement with the government, which will retain the remaining 20% of the business. The agreement will provide certain rights to them, but ensure Cohort has day to day management control over EID.

The group are also close to an agreement on acquiring the whole of the minority shareholding of MCL from its management and they expect to complete this by the end of December. The shares will be acquired on the basis agreed in the original agreement and the expected cost for the group will be £5.5M. This cost excludes the share of the surplus cash in the business as at the end of 2017 payable to the minority shareholders, which is estimated at £2M.

The reorganisation of SCS has now been completed, with the operating divisions being transferred to MASS (training support) and SEA (capability development and air systems). The board expect a positive contribution from this action in the second half trading performance, mostly from the saving in overheads, which is estimated at £1.6M per annum. The market for the consulting element of SCS has deteriorated over time and worsened considerably in the first half of this year, making a major restructuring essential. The cost of the reorganisation is estimated at £2.2M including redundancy and transition costs, asset write-downs and the provision for an onerous lease on its operating site at Theale. The group will look to mitigate this last cost by increasing the use of the site by other Cohort businesses as well as investigating other options such as sub-letting.

Going forward, the board are confident of a strong second half performance reflecting their normal seasonality, order book visibility, the benefit of a full second half contribution from EID and the elimination of SCS losses. £49.5M of the order book is deliverable in the second half and underpins nearly 80% of the consensus forecast revenue for the full year. Prospects for further order intake are encouraging. Overall, the order book and pipeline gives them confidence they will make further progress this year and they maintain their expectations for the full year.

The initial view on the impact of Brexit remains largely unchanged. The group are not exposed to significant amounts of EU revenue through their UK operations but the weakening of Sterling has resulted in an immediate improvement to the reported value of the Euro operating profit from EID, an increase of around £100K compared to initial assumptions. In the longer term, sustained weakness in Sterling would continue to be of net benefit, the enhancement to the export competitiveness outweighing any impact from increase cost inputs.

At the period-end the group had a net cash position of £9.9M compared to £11.4M at the same point of last year. At the current share price the shares are trading on a PE ratio of 21.7 which falls to 16.2 on the full year consensus forecast. After the interim dividend was increased by 16%, the shares are yielding 1.5% which increases to 1.7% on the full year forecast.

Overall then this has not been a great period for the group. The losses worsened, net assets declined and although the operating cash outflow improved, this was due to improvements in working capital outflows and cash profits reduced. The weakness came from the SCS business where a poor market and loss of a contract seem to have resulted in terminal losses as the group has now reorganised the division. The other poor performer was SEA, which has suffered from less research work, which will continue into the second half, and the slippage of some large maritime contracts which should improve in H2.

The other divisions saw improvements or flat performances and most are also expected to improve in the second half. The order intake has been disappointing but there seems to have been a lot of orders after the end of the first half which should make that look a bit more healthy. With a forward PE of 16.2 and yield of 1.7%, I am not sure if this offers good value and the group really needs to improve in the second half, although it does seem as though this is happening. Tricky, I continue to hold for now.

On the 9th January the group announced that the Portuguese government authorised the acquisition of tactical radios for their Army from EID. The details of the contract will be subject to negotiation but the approved value is €7.5M and delivery is expected to take place between 2017 and 2023.

On the 25th January the group announced that MASS has been selected to deliver the Met Police’s digital forensics managed service. The contract is expected to have a seven year duration and a value of about £15M with the option to extend for a further three years. The contract is available to other police forces within the UK which provides the possibility to increase the contract value during the ten year term to a national potential of around £230M.

On the 1st February the group announced that it had acquired the minority holding in its subsidiary MCL for a cash consideration of £5.1M in line with the arrangements stated at the time of the acquisition. The consideration has been paid out of existing financial resources and a further payment of £2M is expected to be made before the end of July reflecting a further earn out linked to the business’ order book. The impact of the acquisition is expected to be earnings enhancing in the remainder of the year.

On the 9th March the group announced that MCL had been awarded a contract by the MOD to supply and support hearing protection systems and communication ancillaries for specialist land, maritime and air applications. The initial value of the four year contract is £9.9M and it includes options for a one year extension and a complete mid-life enhancement of the capability. The contract follows previous MOD contract awards for hearing protection announced in 2015 with the solution being developed in partnership with a Danish audio technology company.

On the 2nd June the group released a contract announcement. MCL has been awarded two contracts by the MOD to supply and support hearing protection systems and communication ancillaries for land, maritime and air applications worth a combined £5.5M. They comprise a follow-on order worth £3.2M for Tactical Hearing Protection Systems for Dismounted Close Combat Users that provide hearing protection for RAF, Royal Navy and Reservist personnel; along with a new contract to provide Ear Communication Devices for RAF pilots and air crew with an initial value of £2.3M over five years with options for a further two years.