Cohort has now released their interim results for the year ended 2018.

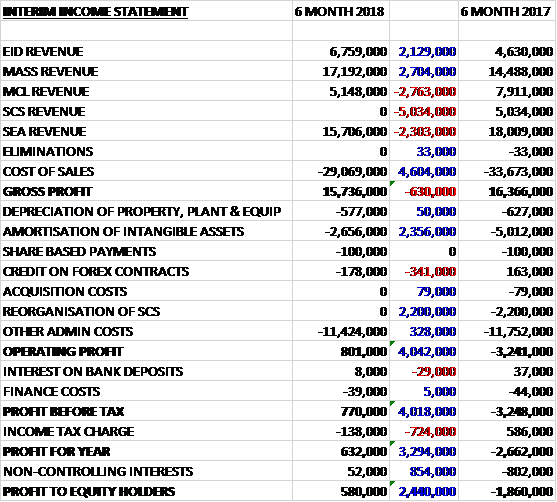

Revenues declined when compared to the first half of last year as a £2.7M growth in MASS revenue and a £2.1M increase in EID revenue was more than offset by the elimination of £5M of SCS revenue, a £2.8M decline in MCL revenue and a £2.3M fall in SEA revenue. Cost of sales also declined which meant that the gross profit was £630K lower. We then see a £2.4M reduction of amortisation charges and no reorganisation costs, which were £2.2M last time and after a £341K detrimental movement in forex contracts was offset by a reduction in other admin costs the operating profit improved by £4M. Interest charges were broadly similar but tax charges were up £724K to five a profit for the period of £580K, an improvement of £2.4M year on year.

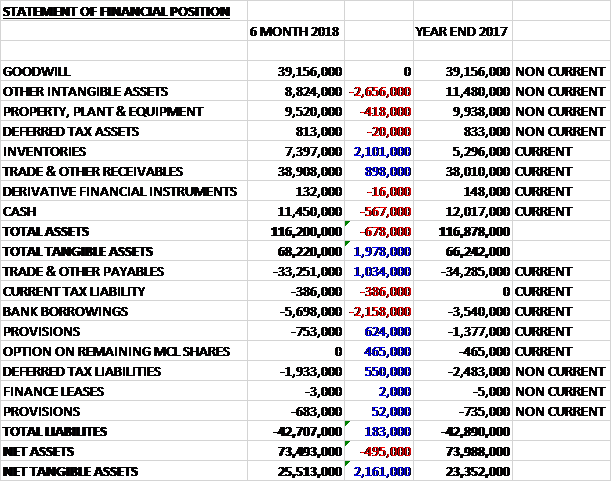

When compared to the end point of last year, total assets declined by £678K, driven by a £2.7M fall in intangible assets, a £567K reduction of cash and a £418K decrease of property, plant and equipment, partially offset by a £2.1M growth in inventories and an £898K increase in receivables. Total liabilities also declined during the period as a £2.2M growth in bank loans and a £386K increase in current tax liabilities were more than offset by a £1M decline in payables, a £676K fall in provisions, a £465K reduction in the option on the MCL shares and a £550K decline in deferred tax liabilities. The end result was a net tangible asset level of £25.5M, a growth of £2.2M over the past six months.

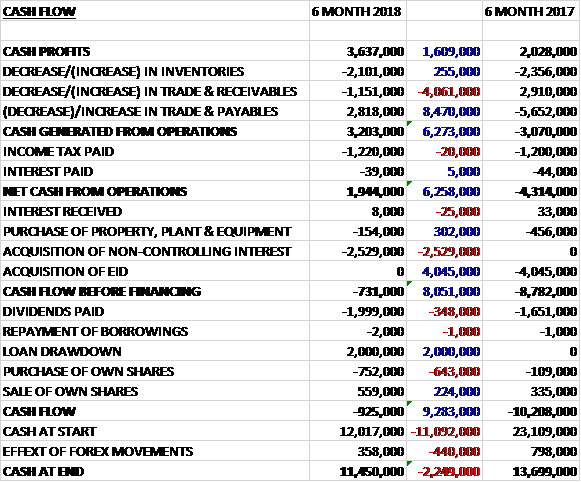

Before movements in working capital, cash profits increased by £1.6M to £3.6M. There was a modest cash outflow from working capital but this was less than last year and after interest and tax remained broadly similar, the net cash from operations was £1.9M, a growth of £6.3M year on year. The group spent £154K on capex and £2.5M on a non-controlling interest of one of their businesses which meant that before financing there was a cash outflow of £731K. The group then took out £2M of new loans to pay the £2M of dividends to give a cash outflow of £925K in the period and a cash level of £11.5M at the period-end.

The profit at EID was £1.2M, a decline of £203K year on year despite an increase in revenue. As expected, margins reduced from the unusually high level seen last year which, together with a smaller sales increase than expected due to the rescheduling of some deliveries into the second half, led to the lower profit. The second half will benefit from the 80% ownership of the business and the order book of £29.7M underpins all of the expected second half revenue.

The profit at MASS was £2.5M, a growth of £149K when compared to the first half of last year and included a £600K contribution from the Training Support business which was previously part of SCS. Elsewhere the business continued to deliver well in its key EWOS business and recent developments in this area give the board confidence that the business will remain a strong contributor to MASS.

There was growth from the cyber business, which includes the Metropolitan Police Service Digital Forensic Programme secured at the end of last year. There are opportunities to provide this service to other UK police forces as well as potentially to overseas customers although the priority at the moment is the delivery of the Met Police programme. The level of orders give the board confidence that MASS will have a stronger second half.

The profit at MCL was £167K, a decrease of £586K when compared to the first half of 2017 on lower revenues, which was below expectations. Some reduction was expected, reflecting the timing of deliveries of hearing protection systems but the result for the business was also impaired by the slippage of some milestones on one if its development projects where the UK customer rescheduled design acceptance.

Although reasonably well positioned for a much stronger second half, the business is seeing a reduction in expenditure in some of its UK market areas and this may affect second half revenue. The delayed project will also see revenue slip into 2019. The board nevertheless expect the performance for the year as a whole to be similar to last year.

The profit at SEA was £1M, broadly flat year on year with a decline of just £6K on lower revenues, despite the inclusion of some of the profitable parts of SCS. The margin saw an improvement due to increased deliveries of maritime systems to export customers offsetting a further reduction in research activity.

In the maritime division, deliveries of torpedo launch systems to export customers began, offsetting a relative lull in its activity on the UK submarine communication programmes due to a gap between substantive completion of design work for the Astute Class and the expected increase in activity on Dreadnought Class. Like SEA, the business is seeing a lower level of spend in the UK, especially in its maritime support framework contracts. Research has continued to be weak with most land activity halted and the remaining SEA work focussed on the maritime area. As a result the business has taken action to mitigate costs and absorbed the reduced research work into its simulation, support and product division.

Elsewhere in the business, SEA’s range of ROADflow products continue to see growth, especially of its new motion system which targets yellow box junctions and banned right turns. This division also contains some former SCS lines of business which contributed £200K of profit. The oil and gas sector remains challenging, although the business remains profitable due to some reduction in overhead costs.

The closing order book contains a significant amount of higher margin maritime systems work for export customers and the pipeline of opportunities gives the board confidence that the business will have a much stronger second half and overall they expect the performance of the business to be similar to last year.

The SCS business was discontinued and accounted for a £455K loss last time.

During the period the group acquired a further 23% of EID from the Portuguese government for £3.5M which takes their shareholding up to 80% with the government owning the other 20%. Also during the period a final amount of £2.5M was paid to the former shareholders of MCL.

Going forward, a stronger second half performance is in prospect which maintains the board’s expectations for the year. Nearly £55M of the £132.1M order book is deliverable in the second half and underpins 83% of the forecast revenue although it should be noted that the order book as a whole has fallen from £136.5M at the year-end. Prospects for further order intake in the second half are encouraging though and there will be the benefit of five months’ contribution from 80% of EID. Overall, allowing for the fact that they have proportionally more to do in the second half, and notwithstanding the pressures in the UK market, the board believe the group can maintain their expectations for the full year.

In their key markets, they continue to see a focus by the UK MOD on areas such as submarines, special forces, cyber defence and secure communications whereas in other areas such as research and product support for some in-service equipment, they have experienced lower demand, with purchases either reduced or delayed. Elsewhere Portugal is seeing a relatively robust level of spend with upgrades to both maritime land and communications systems and the recently announced Portuguese defence budget shows an increase in procurement spend of around 9%.

At the current share price the shares are trading on a PE ratio of 45.2 which falls to 13.9 on the full year consensus forecast. After a 16% increase in the interim dividend the shares are yielding 1.8% which increases to 2% on the full year forecast. At the period-end the group had a net cash position of £5.7M compared to £8.5M at the year-end.

Overall then this has been a bit of a difficult period for the group. Profits were up but this was due to lower amortisation costs (perhaps to do with impairments) and no reorganisation costs, without which profits would have been lower. Net tangible assets did improve and the operating cash flow also improved but no free cash was generated. All of the businesses saw profits down on an underlying basis with slippage of orders, lower UK spend in some areas and continued weakness in research. H2 is expected to be better but much hangs on delivering this expected performance. I don’t think the forward PE of 13.9 and yield of 2% adequately covers this risk so I think I might sit this one out for a while longer.

On the 30th January the group announced that SEA had been contracted by a UK government agency to lead a team in the area of Soldier System Research and Development. The contract has an initial value of £700K for 2018 but is likely to continue until 2021 with a potential value in excess of £3M. Under the contract the business will lead a team of specialist companies to develop a weapon system that combines novel and emerging small arms technologies to produce an integrated system that will deliver greater efficacy for the individual soldier on the battlefield.