Dechra has now released its final results for the year ended 2015.

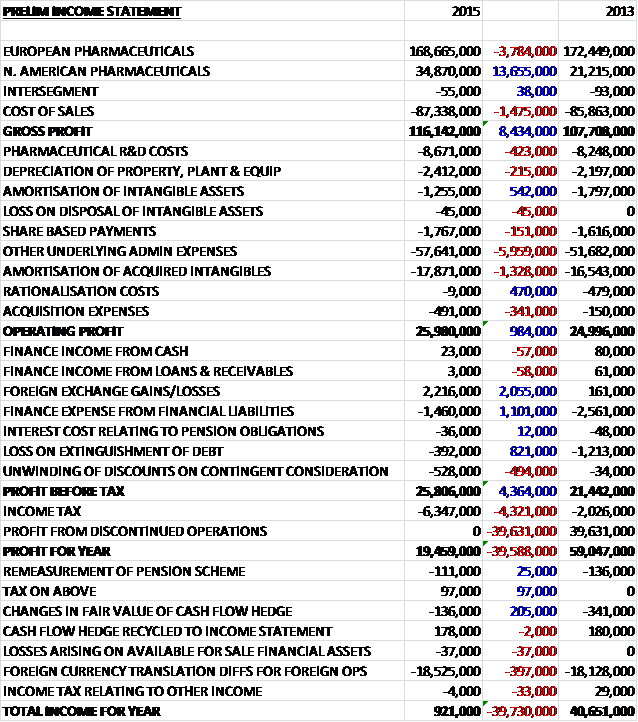

Overall revenues increased when compared to last year as a £3.8M decline in European revenue was more than offset by a £13.7M growth in North American revenue. Cost of sales also increased somewhat, to give a gross profit some £8.4M ahead of last year. R&D costs grew by £423K and there was a small increase in depreciation with a £6M growth in other admin expenses along with a £1.3M increase in the amortisation of acquired intangibles to give a pre-tax profit of £25.8M, an increase of £4.4M when compared to 2014. This was almost exactly wiped out by an increased tax bill (partially relating to prior year adjustments), however, and last year’s gain on the disposal of a subsidiary meant that profit for the year came in at £19.5M, a decline of £39.6M year on year. It is also worth noting that once again, foreign currency translations wiped off £18.5M of this when determining the total comprehensive income for the year.

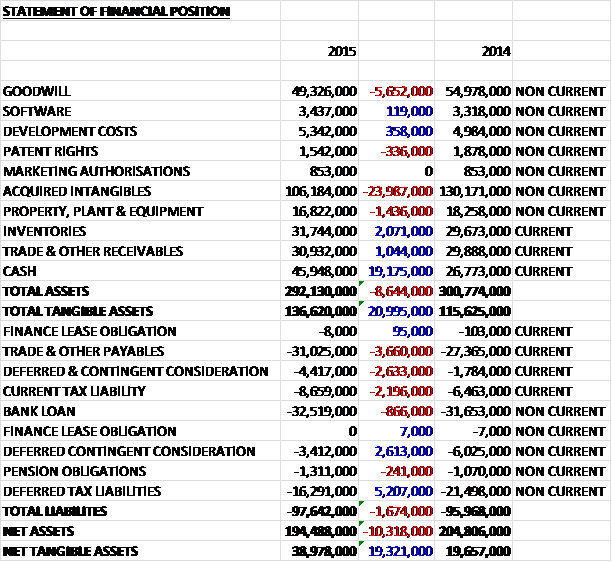

When compared to the end point of last year, total assets fell by £8.6M driven by a £24M decline in acquired intangibles (partly due to amortisation and partly due to foreign exchange movements), a £5.7M fall in goodwill due to currency translation and a £1.4M decline in property, plant and equipment, partially offset by a £19.2M increase in cash, a £2.1M growth in inventories and a £1M increase in receivables. Liabilities increased during the year as a £5.2M fall in deferred tax liabilities was more than offset by a £3.7M increase in payables and a £2.2M growth in the current tax liability. Also note that the deferred contingent consideration in transferred from non-current liabilities to current liabilities. The end result is a net tangible asset level (removing just goodwill and acquired intangible actually) of £39M, an increase of £19.3M year on year.

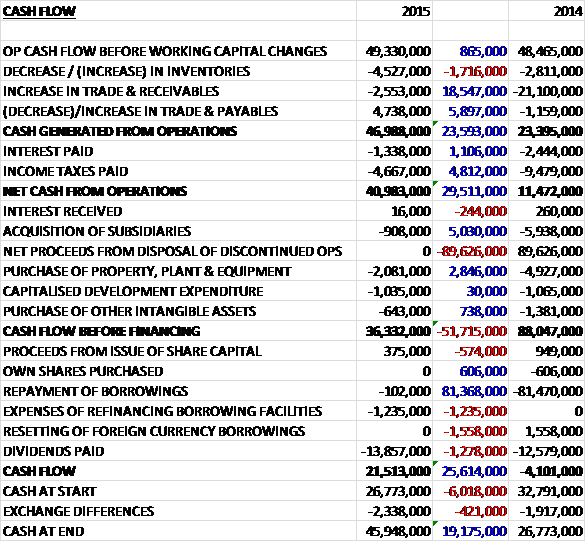

Before movements in working capital, cash profits increased by £865K to £49.3M before a much smaller increase in receivables than last year along with lower interest paid and taxes meant that net cash from operations increased by £29.5M when compared to last year at £41M. The group then only spent £2.1M in fixed assets, £643K on intangible assets and £1M on development expenditure and even after some deferred consideration of £908K was paid, free cash flow stood at an impressive £36.3M. The group then spent £1.2M relating to the refinancing of the borrowing facilities and even after £13.9M was paid out in dividends, the cash flow for the year stood at £21.5M with a cash level of £45.9M at the year-end.

The operating profit at the European pharmaceuticals division was £48M, a decline of £1M year on year due to adverse currency movements (profits were up just over 4% on a constant currency basis). There was solid growth at constant currencies as a strong performance across the companion animal products portfolio offset a decline in food processing animal products. Most markets grew in the year but the most significant double digit sales increases were seen in the UK, France, Spain and Belgium. Endocrinology, dermatology and anaesthetics all performed strongly. The dermatology portfolio was expanded with the launch of an in-licensed product, Sporimune in seven European markets and the launch of Osphos in the UK improves their position in the equine markets with preparations now being made for the launch of the product across the rest of Europe in the new year.

Food animal products continued to decline as the antibiotics market in Western Europe has a continued focus on prudent prescribing due to antibiotic resistance. This remains an ongoing headwind against the group’s overall performance, especially in Germany and Denmark, where there has also been competitive pressure. In the Netherlands, however, the rate of decline has slowed having reduced sharply over the last four years.

The therapeutic and life stage pet diets, branded “Specific”, have now fully recovered from the stock-outs created by the transfer of the products to a new manufacturer but sales declined slightly compared to the previous year. The range has now been repositioned and a new marketing campaign is being rolled out across Europe focusing on the high inclusion of fish protein, the ethos of deriving the nutrients of the products from sustainable sources, and the Specific brand being dedicated to the veterinary market.

The operating profit of the North American pharmaceuticals division was £10.6M, an increase of £4.6M when compared to last year. All major therapeutic areas grew, in particular endocrinology and dermatology sales increased by 24%. The sales increase in in endocrinology was driven by Vetoryl which continued to deliver double digit growth, and by the product launch of Levocrine chewable tablets which has outperformed management expectations.

The performance in North America benefited from the full year trading of Phycox, the re-launch of ophthalmics, the launch of Osphos and the opening of the Canadian subsidiary. Phycox, which was acquired in May 2014, has performed well throughout the year and the number of customers purchasing the product increased by over 50%. The ophthalmics products, which were re-launched following long term supply issues, achieved expected sales targets despite strong competition from human generic equivalents. The group also launched Osphos, the equine lameness product, and whilst the uptake has been a little slower than expected, they have penetrated approximately one third of the equine and mixed animal practices. Adjusting for these new products, the existing core products grew by nearly 22% on a constant currency basis.

Following a serious shortage of critical care intravenous fluids in the US market, the group obtained FDA approval for the emergency importation of their European critical care intravenous fluid Vetivex to supply the equine market. They are currently working with the FDA to achieve long term approval for a US labelled version of this product to add to the equine portfolio. To support growth in the US, there have been 16 new appointments, predominantly across sales and technical support.

Revenues of companion animal products were £113.9M, an increase of £15.7M fuelled by Vetoryl’s momentum in the EU and US, the launch of Phycox and the success of Dermapet in the US; revenues of equine products increased by £1.7M following the launch of Osphos; revenues of farm animal products were £27.3M, a decline of £4.5M due to the impact of the reduction in prescription antibiotics and increased competition in Germany and Denmark; revenues of diet products fell by £2.8M to £25.6M due to some supply disruption following the transfer of the manufacturing of dry diets to a third party manufacturer; and revenues of third party manufacturing were £19.7M, an increase of £1.7M as the business realised value from the new contracts signed last year.

The key objective of the manufacturing division is to produce own brand pharmaceuticals for the group but additionally they also utilise spare capacity to provide a third party manufacturing service. Within the year, these external sales, reported under the EU segment, have increased by nearly 12%. A number of projects were implemented across the sites including the premix department in Bladel to increase batch sizes for FAP products; a new faster encapsulating machine in Skipton which increased yield and doubles capacity; a blister packing line to increase capacity and flexibility through automation; and a larger creams and ointments vessel to facilitate a major third party contract and production of in-house creams, liquids and ointments in Skipton.

There have been a number of other developments within the division, the most significant of which is the successful pre-approval inspection of the Skipton facility by the FDA in preparation for the approval of Zycoral, to be manufactured at the site. The US site in Florida was acquired in May 2014 and has been fully integrated into the division. This year they have focused on increasing quality systems and production capacity following the launch of Levocrine which is manufactured there.

Following the launch of Osphos in the UK and US in the first half of the year, it has subsequently received approval in 17 additional EU countries and has also received marketing approval in Canada. TAF Spray was also approved in 14 European countries in the year. This is a generic antibiotic aerosol which is used to treat superficial wound infections in several species. A new low dose 5mg Vetoryl has been approved for the US which enhances the range of dosing options available to vets and helps continue growth from the group’s leading product. To support the geographic expansion goals, minor approvals were received for Octacillin and Soludox in the Philippines, and Sedaxylan in South Africa.

Complete dossiers have been filed in both the EU and US for a canine endocrine product, to be branded Zycortal and it is hoped that the first approval will be received during the new financial year. The group has three Food Animal products for poultry and swine under review in Europe and are preparing a further dossier for a decentralised application which will be submitted before the end of the 2015 calendar year. Owing to the nature of the development process, some projects in the feasibility phase have taken longer than projected before reaching the development phase but this is being partially mitigated by the overall number of projects in development. The group have reached a preliminary agreement with Jaguar Animal Health to secure marketing and joint development rights for their leading companion animal product. They have acquired a partially completed dossier for an additional canine endocrinology product and further development work will be required to gain full approval which will be conducted at the manufacturing facility in Skipton.

In the first half of the year the group opened their Canadian subsidiary which commenced trading in January and has already begun to establish a strong presence in the territory. The new subsidiary achieved sales targets for Vetoryl, Felimazole and the dermatology range but other products sales were impacted by surplus stock in the market from the previous distributor which had washed through the system by the end of the financial year. They have also established a trading subsidiary in Poland which came about as the distributor was acquired during the year and trading there commenced in May. The group are also at an advanced stage of planning the start-up in Austria, which should start trading before the end of the new year. They are also continuing to invest in the regulatory function to gain new licenses in other countries and whilst there are few locations where they have the relevant critical mass for a new start-up, the regulation process is important in order to expand beyond the core markets.

The roll out of the Oracle IT system remains one of the primary objectives for the group. Detailed plans are in place for the implementation to be completed by the end of 2017. Also, as far as IT is concerned, a group high speed network has been implemented across all major locations, a web-based portal for staff training has been designed, a new website has been launched in multiple languages and new hybrid PC tablets are being introduced for all sales staff.

During the year the group revised its borrowing facilities which now comprise of a £90M revolving credit facility and a £30M accordion facility committed until September 2019. Resetting of foreign currency borrowings within the prior year cash flow statement relates to the cash adjustment required to ensure the movements in foreign exchange rates do not result in the committed revolving credit facility being exceeded. Interest is charged at 1.3% over LIBOR.

During the year, the group launched Levocrine, a product acquired with the Phycox acquisition. There was a contingent consideration of $1.5M which was due upon the successful registration of the new product and a further $4.2M contingent on future sales, of which $500K was paid during the year. During the year the group paid a further £600K in respect of the acquisition of Dermapet relating to deferred consideration to be paid on the fourth anniversary of the completion date. The maximum further consideration payable was $5M, contingent on revenue exceeding $20M in any rolling 12 month period ending on the sixth anniversary of completion. After the year-end, this $5M has been paid leaving no further consideration to pay. I think it is fair to say that the Dermapet acquisition has been a costly one.

After the year-end, the group signed a conditional share purchase agreement to acquire 63.3% of the authorised shares in Genera, a Croatian listed pharmaceutical business. Under Croatian take-over rules, the group is required to make a mandatory offer for the remaining issued share capital of the business. They have offered €51.4M for the entire share capital which will be wholly payable in cash and is to be funded out of existing facilities. Genera has a strong market share in Croatia and the neighbouring countries with three divisions: Animal Health, which represents the majority of revenue; agrochemicals; and human pharmaceuticals. It is unclear what Dechra intends to do with the agrochemical and human pharmaceutical businesses. The principle reason for the acquisition is to enter the poultry vaccines market and three new geographic markets in Croatia, Slovenia and Bosnia as well as allowing access to a low cost manufacturing base.

Going forward, the board believes that the focus on key therapy areas, the continued rate of adoption of Osphos and sales in the new territories will drive progress in the short term. Current trading is in line with management expectations but the business continues to be exposed to exchange rate headwinds. In the long term, the delivery of new products and the integration of potential acquisitions give the board confidence in future prospects.

At the year end the group had net cash of £13.4M compared to a net debt position of £5M at the end of last year. At the current share price, the underlying PE ratio is a hefty 23.4 which falls to 21.5 on next year’s consensus forecast which still looks rather expensive. After a 10% increase in the total dividend, the shares are currently yielding 1.8% which increases to 2% on next year’s forecast which is decent but not that exciting.

Overall then this has been a solid year for Dechra. Profits fell year on year but this was only due to higher taxes and the gain from discontinued operations last year and profit before tax from continuing operations did increase. Net assets grew strongly driven by a higher cash level and it is here that we really see the strength of the group. Operational cash flows increased and there was a very healthy amount of free cash generated which enabled them to end the year in a net cash position. Operationally, Europe was a little difficult mainly as a result of the weakening euro. The reduction in antibiotic usage in food animals was another drag on results but this was offset by increased sales in other areas. In North America, things were much better. There was a very strong performance in both acquired products and like for like sales in all areas.

I am a little concerned about the comment regarding the fact that some projects in the feasibility phase are taking longer than expected to reach the development phase and perhaps in the medium term this will reduce profits a bit? The Genera acquisition looks a little expensive to me but the new area of poultry vaccination is probably a sensible strategic route to take given the continued pressures on antibiotic usage. Going forward, the business continues to struggle with the weak Euro but otherwise things seem to be going OK. On a forward PE of 21.5 and a forward yield of 2%, this is certainly not a value share but given the sheer quantities of cash being generated here I am happy to hold for the time being.

After enjoying a very strong run, it does seem as though the shares have entered a downtrend which is a little concerning.

On the 23rd October the group released a trading update covering Q1. Group revenue increased by about 21% at constant currency exchange rates (13% at actual rates). This performance was driven by a strong momentum in all business units, the phasing of sales in advance of regional price increases and the contribution from the new subsidiaries.

The European pharmaceuticals segment increased revenues by 11% at CER, but were flat at constant exchange rates. The growth was driven by companion animal products which were ahead of board expectations. Whilst it is only three months into the new year, the group saw some solid trading in food producing animal products too but diet sales declined. The new Polish subsidiary, which started trading in May, performed strongly in the period.

Total reported North American revenue increased by about 86% at a constant currency, but even more at actual exchange rates as the dermatology, endocrinology and ophthalmic ranges started the year strongly. Canada also contributed to the growth as it only started trading in Q2 last year. Sales of the Dermapet range reached the $20M threshold in August which triggered the final milestone payment of $5M from the acquisition in 2010 so it will be good to get that out of the way.

Zycortal, a novel canine endocrine product for the treatment of Addison’s disease, received EU approval in September. The group are now preparing for a phased launch in all European markets throughout the remainder of the year. The complete dossier is also under review by the FDA for approval in the US. Osphos, indicated for the treatment of navicular syndrome, is gaining market share in the US and it is expected to be launched in EU territories by the end of the 2015 calendar year.

The acquisition of Genera has been successful with the cost of acquiring the 92.26% controlling interest being €36.6M. During the period the group also entered into an agreement with Central Sales Ltd in Canada the IP of HY-50, an equine lameness product for C$750K. They already owned the trademarks and rights for the product in other countries and now have control of the brand worldwide. This all seems very strong to me and probably justifies its premium price.

On the 14th January the group released a trading update covering the first half of the year. European Pharmaceuticals increased revenues by 4% on a constant currency basis but saw a decline of 3% at actual exchange rates. Including the Genera acquisition, the growth was about 9% at constant currency. The growth was driven by companion animal products which increased by 4% (constant currency). Whilst the German market continues to experience challenges, the performance I the food producing animal business has improved due to growth in markets targeted for expansion and good trading in Poland. Overall Diets sales declined by 3%, however, although a recovery in some markets has been seen.

Total reported North American revenue increased by about 51% on a constant currency basis, and performance was even better at actual exchange rates, up 57% as the dermatology, endocrinology and ophthalmic ranges started the year strongly. The momentum in the US is being maintained as the group invests in sales, market and technical support. Canada, which only started trading in H2 2015, also contributed to this growth.

The group received FDA approval in the US in December for Zycortal, a novel canine endocrine product for the treatment of Addison’s disease which follows the EU approval in September with the launch expected in Q4 this year. Two FAP antibiotics, Solupen and Solamocta (for ducks and turkeys) were approved in the EU in Q4 2015 but the company terminated an early stage project for canine ophthalmology following inconclusive results during the feasibility studies.

In January, the group opened a subsidiary in Austria and they have alos acquired Laboratorios Brovel, a veterinary pharmaceuticals company based in Mexico. They paid $5M in cash with a further $1M contingent upon Brove reaching registration milestones for Dechra’s products in Mexico. The business has a diverse product portfolio with a turnover of £2.6M but I suspect the real reason for the acquisition is an entry into the Mexican animal health market with the initial focus on the registration of several existing Dechra products in this market.

Overall then, a pretty good update in my view.

On the 16th February it was announced that CFO Anne-Francoise Nesmes will be stepping down in July to take up the same role at Merlin Entertainments having been at the company since 2013. This is a bit of a shame but I guess she felt Merlin had more to offer.