Easy Jet has now released its final results for the year ended 2015.

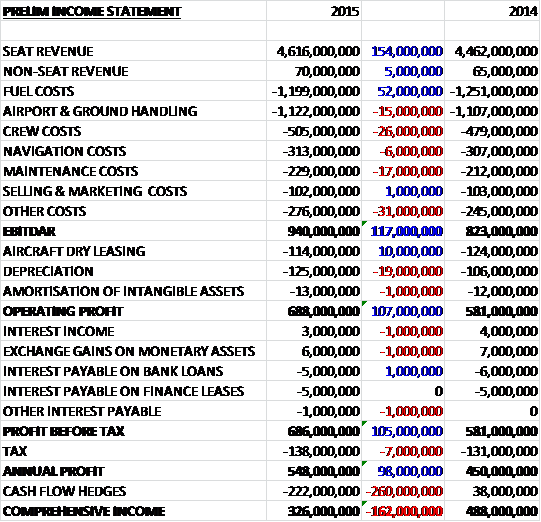

Revenues increased by £159M when compared to last year with passenger volumes increasing by 6% and revenue per seat up 1.5% on a constant currency basis to £64.28, offset by currency headwinds, whilst fuel costs fell by £52M with sales and marketing costs broadly flat. There was a £26M increase in crew costs, though, along with a £17M growth in maintenance costs, a £15M increase in airport and ground handling costs, a £6M increase in navigation costs and a £31M growth in costs to give an EBITDA some £117M above that of last year. We then see a £10M fall in aircraft dry leasing more than offset by a £19M growth in depreciation and after a small fall in finance income and a modest increase in tax, the annual profit was £548M, an increase of £98M year on year. I must say that as an aside, the Easy Jet accounts are a joy to analyse compared to some other companies, with no one-off charges and a good, sensible, split of underlying costs.

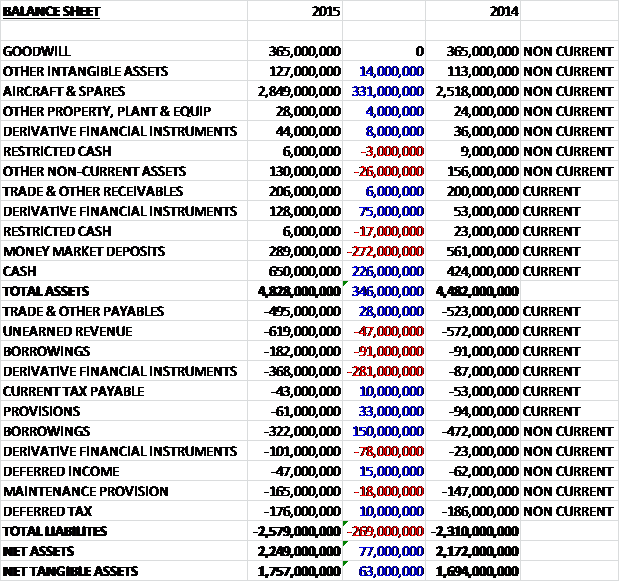

When compared to the end point of last year, total assets increased by £346M driven by a £331M growth in the value of aircraft and spares, a £75M increase in derivative financial instruments, a £226M growth in cash and a £14M increase in other tangible assets, partially offset by a £272M fall in money market deposits, a £26M decline in other non-current assets and a £17M fall in restricted cash. Total liabilities also increased during the year as a £359M increase in derivative financial liabilities, related to the fuel price hedge, a £47M increase in unearned revenue and an £18M growth in the maintenance provision was partially offset by a £59M fall in borrowings, a £28M decline in trade and other payables and a £15M decrease in deferred income. The end result is a net tangible asset level of £1.757BN, an increase of £63M year on year.

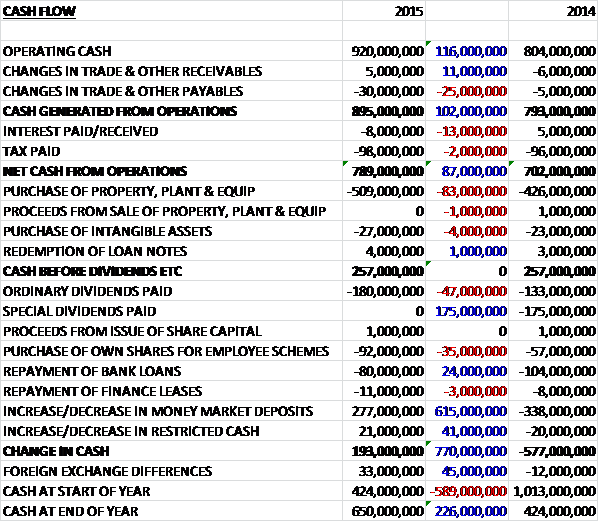

Before movements in working capital, cash profits increased by £116M to £920M but this was eroded somewhat by a decline in payables, a net interest payment and a small tax payment so that the net cash flow from operations was £789M, an increase of £87M year on year. The group spent £509M of this on property, plant & equipment, mostly related to the 20 new planes, and £27M on intangible assets to give a free cash flow of £257M. Of this, £180M was spent on dividends, £92M was spent on shares for employee schemes (that sounds like a lot!), and some £91M was spent on the repayment of loans and finance leases. A £277M fall in money market investments, however, meant that there was a cash inflow of £193M for the year to give a cash level of £650M at the year-end.

The short haul European aviation market has seen strong underlying demand throughout the year particularly in Easy Jet’s primary markets in Western Europe. Economic trends are currently favourable with GDP growth in the group’s main markets with an improving outlook across all of their other major regions which is reflected in strong demand for their services. The total European short haul market grew by 5% year on year, sustained in part by the continued low fuel price. Low cost carrier share of the short haul market increased by about one percentage point to 42%. In the same period, the group’s competitors increased capacity by 7% in its markets, with particularly strong growth in the UK market. In comparison, Easy Jet increased capacity by 5% with growth of 4% in the first half increasing to 6% in the second half. Legacy carriers are also transferring capacity from their flag airlines to lower-cost subsidiaries such as Vueling, Eurowings and Transavia.

During the year the group added a net sixty routes to the network, slightly more than last year. These were allocated to new bases such as Amsterdam, Hamburg, Naples and Porto and to markets where they want to consolidate their position and grow share, such as Switzerland and Italy. The group have also recently announced new base openings in Venice and Barcelona.

In the UK the group are continuing to reinforce their already strong position in the market, both London-based and regional. They remain the number one carrier by market share at almost all of its UK bases, including Gatwick, Luton, Bristol, Belfast and Edinburgh. Their positioning, market share and airport bases are driving both leisure and business passengers. The group increased capacity by 3% during the year, launching new routes such as Gatwick to Stuttgart and Luton to Essaouira, while continuing to increase frequencies on selected routes while their competitors increased capacity in the group’s markets by 9%.

Easy Jet is France’s second largest short-haul airline with a 14% market share with 26 aircraft based in the country. The board see opportunities to grow their market share in France, adding capacity at Charles De Gaulle through up-gauging and strengthening their domestic network. They increased capacity in France by 6% in the year against competitor growth of 5%, launching eight new routes in the year such as Toulouse to Seville and Paris Orly to Split.

Easy Jet has a 12% market share in Italy with 29 aircraft based in the country. The group continues to target increasing market share in Italy, by reinforcing their existing strong positions and investing more in the higher value catchment areas. They are the biggest operator at Milan Malpensa with 22 touching aircraft, have recently opened a new base at Naples and will open a base in Venice early in 2016. They are supporting this by redeploying aircraft from Rome Fumicino. Overall the company increased capacity in Italy by 7% launching 23 new routes in the year including Milan Malpensa to Munich, Milan Linate to Paris CdG and Milan Linate to Amsterdam.

Easy Jet is Switzerland’s second largest airline with a 23% total market share with 23 aircraft based in the country. The group are the number one operator at both Geneva and Basel airports. They increased capacity by 9% during the year, building and reinforcing their leading positions at both airports. Competitor capacity growth in their markets was also 9% and Easy Jet launched eleven new routes in the year such as Geneva to Menorca and Basel to Luton.

Easy Jet has a 4% market share in Germany with 12 aircraft based there. This is a large market, although with a more regional structure than other European countries. The group has focused on its two bases at Berlin Schoenefeld where it is the number one airline, and Hamburg, which they opened last year. They target continued growth in Germany, taking market share from the incumbent operators and have increased capacity by 15% during the year with competitor growth of 6%. They have launched sixteen new routes in the year such as Hamburg to Lanzarote and Hamburg to Paris Orly.

Easy Jet has a 13% market share in Portugal and an 8% market share in Spain with six aircraft based in the former. These two countries are principally an in-bound market for the group with strong demand from the rest of Europe. They increased capacity by 8% in Portugal and 2% in Spain reflecting in particular the investment in a new base in Porto from which they launched six new routes to Luxembourg, Nantes, Stuttgart, Manchester, Bristol and Luton. They also announced that a new base in Barcelona would be opening in February 2016. Competitor market share grew faster, however, with 10% growth in Portugal and 7% in Spain.

The company is the second largest short haul airline in the Netherlands with a 9% market share and 3 based aircraft. The country is a significant opportunity where they currently carry four million passengers a year. In March they opened a new base at Schipol airport in Amsterdam where they are now the second biggest operator, and are continuing to invest in growth of their market share. As a result they have increased capacity by 17% during the year against competitor growth of 9% with nine new routes launches such as Amsterdam to Nice.

Passengers increased by 6% to 68.6M with a record load factor in August of 94.4% and the annual load factor increased by 0.9% to 91.5%. Revenue per seat increased by 1.5% year on year on a constant currency basis whilst capacity grew by 5% to 75M seats. Cost per seat decreased by 3.4% with benefit from fuel and currency but cost per seat on a constant currency excluding fuel increased by 3.6% due to cost pressures that include regulated airport price increases, increased de-icing costs and significant disruption costs which have been mitigated through £46M of sustainable savings with a pipeline of structural cost improvements to deliver future savings.

Excluding fuel, cost per seat decreased by 0.9% to £37.35 but increased by 3.6% on a constant currency basis. This increase includes higher disruption costs following French ATC strikes in April and the impact of two fires at Rome Fiumicino airport. There were also additional costs due to increased airport charges, mostly in Italy, and the early recruitment of crew in the winter to provide a resilient operation ahead of three crew base openings, along with a one-off settlement of £8M with Eurocontrol in the second half of the year. Fuel costs fell by £52M overall to £15.98 per seat and profit per seat increased 12.6% to £9.15 per seat.

Maintenance cost per seat increased by 3.8% at constant currency. 2014 benefited from a reduction in the cost of heavy maintenance following a revised engine contract, and a significant proportion of this reduction was one-off in nature and did not recur this year. This impact was partially offset by the reduced maintenance from the return of five leased aircraft during the year, and some benefits of a reduced maintenance contract in the year. Other costs per seat increased by 9.6% at constant currency. There were increased disruption costs during the year due to the French ATC strikes in April and the two fires at Rome Fiumicino airport. Investment in the development of their digital customer proposition also contributed to the increased cost per seat.

Aircraft dry leasing cost per seat fell by 9.7% at a constant currency due to the return of five leases aircraft during the year and the extension of twelve aircraft leases at lower monthly rentals. Depreciation costs have increased by 11.8% on a per seat basis driven by the acquisition of twenty new A320 aircraft, which increased the average number of the owned fleet to 164. Fuel cost per seat decreased by 9.1% at constant currency. During the period the average market jet fuel price fell by 36% to $619 per tonne from $973 per tonne in the previous year. The operation of the fuel hedging policy meant that the average effective fuel price movement only saw a decrease of 10.7% to $820 per tonne.

The group is launching a loyalty programme but it doesn’t seem to be very similar to other airline offerings and instead of offering free flights, they are offering things such as free name changes and a low price promise, which sounds a bit wishy-washy to me. This scheme will be rolled out in early 2016.

The group is also targeting business customers and are focused on providing a bespoke business offering through distribution platforms, travel management companies and direct to small and medium sizes enterprises. They signed up a hundred corporate customers during the year and despite a strong comparable benefit in 2014 due to the Air France strike, the group nevertheless continued to increase the business yield premium during the year. Sales of business products performed well with a 58% increase in the sale of flexible business fares when compared to last year. Sales through global distribution systems grew by 32% in the year as the group continued to leverage its relationships with the travel management companies. Bookings from corporate customers direct also went up by 30%. They continue to see opportunities to sell its business product across Europe and they have recently strengthened their corporate sales capability through a new market, customer and industry structure.

The group will be investing substantially in their digital capability over the next three years. Their initial focus will be on enhancing the digital customer interface, to be delivered in summer 2016, followed by the development of support systems that will lead to them having the first fully integrated e-commerce platform in the airline industry. In the longer term they are committing to the acceleration of their use of data science to improve efficiency, increase revenue and drive greater customer satisfaction. The digital programme will offer increasing amounts of personalisation, introducing a more relevant booking journey bases on previous behaviour to drive higher footfall and higher conversion rates. It will also enable more self-management capability through the entire journey chain, from booking to check-in and through the airport.

The group are now in their second year of a seven year contract with Gatwick airport, as the largest operator there, and in Luton where they have signed a ten year contract. In ground handing they signed an arrangement with GH Italia covering all of the nine airports that they are present in Italy and they expect to agree a number of new contracts in both areas over the next two years. During the year they also completed a new component support arrangement with AJW Group, consolidating previous arrangements and again leveraging their increasing scale and the group expect to drive significant maintenance savings over the term of the contract.

The group is contractually committed to the acquisition of 150 Airbus A320 aircraft with a total list price of $13BN with 20 for delivery next year, 30 for delivery in 2017 and 2018 and 100 new generation aircraft for delivery between 2017 and 2022. In November 2015 the group secured an agreement with Airbus to take delivery of an additional 36 aircraft, of which 30 are new generation, with a total list price of $3.2M. The up-gauging of the fleet from a majority 156-seat A319 composition to a fleet that is over 70% 186-seat A320s is expected to have a 13% to 14% cost per seat benefit, which translates into over £110M of comparable savings. The total fleet at the end of the year stood at 241 aircraft and increased by a net 15 with five A319s retired over 2015.

The group still have a great deal of their future fuel requirements hedged. Over the next six months, 85% of the requirement is hedged at $852 per tonne, for the whole of next year, 83% is hedged at $830 per tonne and in 2017, 60% is hedged at $664 per tonne and a $10 movement per metric tonne impacts next year’s fuel bill by $3.5M.

The board expect to see passenger growth of 7% over the year with margins sustained through rigorous cost control and the benefit of fleet up-gauging, resulting in positive profit momentum. They will continue to expand in their new bases of Hamburg, Amsterdam and Porto as well as consolidating their strong position in the UK, Switzerland, France and Italy. Demand remains resilient and with forward bookings in line with last year, the board are confident for the future.

Based on current market fuel prices they expect the unit fuel bill to decline by between £140M and £160M during the year but much of the benefit will be passed on to customers so there will be a slight decline in revenue per seat during the first half of the year. The board expect a slight decline in total cost per seat at constant currency including fuel and excluding the fuel effect, cost per seat is expected to increase by 2% which will be weighted to the first half and primarily reflects increases in regulated airports costs and navigation charges, disruption costs and an expected cold winter.

Exchange rate movements are likely to have an adverse impact of approximately £15M in the first half compared to this year and £40M for the year as a whole and the board’s expectations are in line with the market.

At the current share price the shares are trading on a PE ratio of 12.4 which falls to 11.8 on next year’s consensus forecast. After a 22% increase in the annual dividend, the shares are currently yielding 3.2% which increases to 3.6% on next year’s forecast. Including aircraft leases, net debt fell by £83M to £363M.

Overall then, this has been a good year for Easy Jet despite a number of setbacks. Profits increased, net assets were up and operating cash flow grew which gives plenty of free cash, although a lot of it is taken up by a near £100M spent on the employee share scheme! Overall, markets are doing well with the European short haul market improving well. The group increased their presents in all their main markets but Germany and the Netherlands seem to be growing particularly well. The load factor for the year has grown to 91.5% and capacity was up 5%.

Cost wise, fuel costs came down but the group is still suffering somewhat from its hedged position that means it is not feeling the full benefit of the decline. Some other costs did increase, regulated airport prices were up, mainly in Italy, de-icing costs increased, there were more disruption costs due to the French ATC strike and fires at Rome, and there was an investment in aircrew ahead of the new bases opening. The group is also investing heavily in its fleet of aircraft and the larger A320 planes should improve costs per seat over the A319 that still dominate the fleet.

The one cloud hanging over the company is the potential effect of terrorist actions in their North African markets of Egypt and Morocco and the knock on effect on these destinations but with a forward PE of 11.8, a dividend yield of 3.6% and a sensible gearing level, these shares seem rather cheap to me and having sold them just prior to the results I am contemplating coming back in here.

On the 4th December the group released its passenger stats for November. Passenger numbers were up 9.6% year on year to 4,807,922 but the load factor only increased from 89.5% to 90.3% and is below the twelve month rolling total figure of 91.8%. There were 378 cancellations in the month compared to just 16 in November last year. Sharm-el-Sheikh accounted for 176 of these cancellations with the rest due to adverse weather earlier in the month.

On the 7th January the group released their passenger stats for December. Overall passenger numbers were 4.8M, an increase of 4.6% year on year despite the predicted reduction in bookings in the weeks following the terrorist attacks in Paris but load factors fell by 1.8% to 86.6%. The group is France’s second largest airline and about 23% of their capacity during December was on French touching routes, hence the decline in the load factor which is now recovering to normal levels so management do not anticipate any change to full year expectations.

On the 26th January the group released a Q1 trading update. Overall, the board’s expectations for pre-tax profits this year remain in line with market expectations. Passengers carried increased by 8.1% to 16.1M as capacity grew by 7.3% and the load factor increased by 0.6 percentage points to 90.3%. Strong revenue per seat performance in October was offset by the impacts of the terrorist atrocities in Egypt and Paris, resulting in lower demand and yield in November and December. The impact of the cancellation of flights to Sharm El Sheikh was to reduce revenue per seat by about 1.5% whereas the events in Paris impacted revenue per seat by 2%. Business passengers grew by 6.5% in the quarter, which seems pretty good. Forward bookings for Q2 are showing a marked improvement, however, in revenue per seat. For Q1 as a whole, revenue per seat was down by 3.7% at constant currency.

Total revenue was down just 0.1% on the prior year as revenue generated by increased passenger volumes and a higher load factor and a 12.7% increase in non-seat revenue due to a good performance in inflight sales helped offset the lower revenue per seat and negative forex movements of £32M. Cost per seat decreased by 3.7% at a constant currency due to the continuing benefit of a lower fuel price but excluding fuel, cost per seat increased by 1.3%. This was better than originally expected, however, due to airport discounts on additional passenger volumes, engineering and maintenance savings, savings in overhead costs and up-guaging of the fleet from A319s to A320s.

The group’s on-time performance improved from the summer with 82% of flights arriving on time during the quarter, although this was lower than the 86% in Q1 last year. At Gatwick the operating performance improved over the summer but the group have been affected by systems changes at Brest Air Traffic Control as well as increased security and immigration controls across the network.

The group have announced a £3BN Euro Medium Term Note programme which is apparently part of the capital review and will facilitate access to new sources of funding. Cash deposits stood at £743M, however, and net cash was £266M at the end of the quarter, down from £353M at the same point of last year due to pre-delivery payments and the acquisition of aircraft.

As far as hedging is concerned, they have hedged 87% of their fuel requirements for the next six months at $846 per tonne; 86% of their requirements for the full year at $823 per tonne and 69% of their requirements next year at $644 per tonne so they should really see some benefits coming through in 2017.

The group plan to grow capacity by around 8% over the half year period and 7% for the full year. Going forward, they expect revenue per seat at constant currency to decline by mid-single digits in Q2 due to the impact of Egypt and Paris. Cost per seat, excluding fuel at constant currency is expected to increase by 1% in the first half of the year with a between 0% and 1% increase over the whole year. They are continuing to derive a cost benefit from low oil prices with jet fuel remaining between $350 to $450 per tonne which would lower the fuel bill by between £75M and £85M over the half year period. On the same basis, the saving over the full year would be likely to be between £165M and £180M. Exchange rate movements for the half year period are likely to have a £25M adverse impact which doubles to £50M for the full year but due to the strong cost performance and low fuel price, the board expects pre-tax profit for the year to be in line with expectations which is a good performance given the issues they have faced. Clearly there are downsides here but on balance I think I will continue to hold.

On the 4th February the group released their passenger stats for January. Passenger numbers increased by 6.3% to 4,276,821 but the load factor fell slightly, down from 85.1% last year to 85%.

On the 4th March the group announced its passenger stats for February. During the month they carried 4,932,212 passengers, an increase of 9.8% year on year although the load factor of 90.5% is below the 90.9% in February last year and the twelve month rolling average of 91.6%.

On the 22nd March it was announced that director Peter Duffy purchased 1,532 shares at a value of £22,597.

On the 6th April the group released its passenger stats for March. Total passenger numbers increased by 4.3% year on year but the load factor was down by 1.3 percentage points to 91.3% with the rolling annual load factor standing at 91.5%. There were 611 cancellations during the month with the majority due to strike action in France.

The increase in passenger numbers is good but the reduction in load factor, although still not too bad, is not great and the French strike action is definitely having a detrimental effect on trading.