Easyjet has now released their interim results for the year ending 2017.

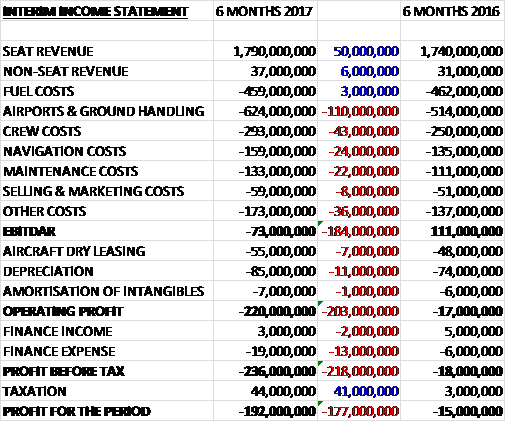

Revenues increased when compared to the first due to a £50M growth in seat revenue and a £6M increase in non-seat revenues. Fuel costs declined by £3M but all other costs grew with a £110M increase in airport and ground handling costs, a £43M growth in crew costs, a £24M increase in navigation costs, a £22M growth in maintenance costs and a £44M increase in other costs to give an EBITDA £184M worse than last time. There was also an £11M increase in depreciation, a £7M growth in aircraft dry leasing costs and a £13M increase in finance expense to give a pre-tax loss £218M higher than last time. After tax income increased by £41M the loss for the period came in at £192M, an increase of £177M year on year.

When compared to the end point of last year, total assets increased by £377M to £5.861BN, driven by a £380M increase in money market deposits, a £62M growth in property, plant and equipment and a £33M increase in receivables, partially offset by a £83M decline in derivative financial instruments and a £41M fall in cash. Total liabilities also increased during the period as a £107M decline in derivative financial liabilities, a £54M fall in payables and a £33M decrease in deferred tax liabilities was more than offset by a £730M growth in unearned revenue, partly as a result of Easter falling in April, and a £199M increase in borrowings. The end result was a net tangible asset level of £1.807BN, a decline of £370M over the past six months.

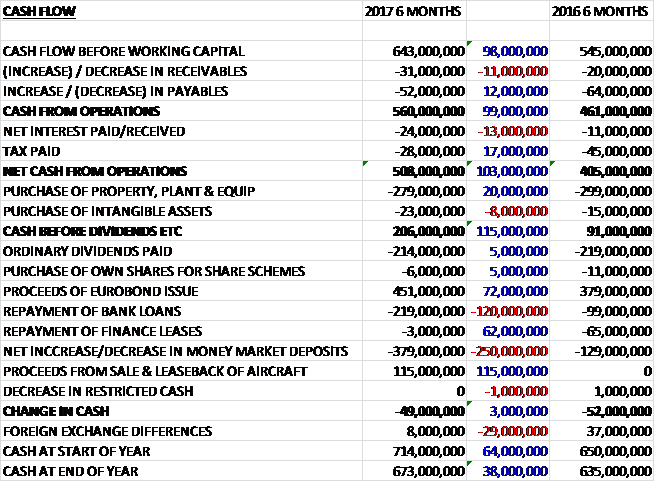

Before movements in working capital, cash profits increased by £98M to £643M. There was a cash outflow from working capital, which was broadly the same as last time and after a reduction in tax payments, the net cash from operations came in at £508M, a growth of £103M year on year. The group spent £279M on property, plant and equipment along with £23M on intangible assets which meant the free cash flow was £206M. This did not quite cover the £214M of dividends and despite £115M of cash from the sale and leaseback of some aircraft and the £451M proceeds from the Eurobond issue, an increase in money market deposits meant that there was a cash outflow of £49M in the period and a cash level of £673M at the period-end.

Within the headline pre-tax loss of £212M, the impact of Easter moving into the second half of the year apparently caused a loss of £45M and forex movements impacted losses negatively by £82M. The short haul market in the group’s markets grew by 9% with particularly strong growth in Spain and Germany.

Revenue per seat decreased by nearly 5% to £48.80 due to increased overall market capacity, along with low pricing sustained by a low fuel price; the movement of Easter into the second half of the year; and increased levels of disruption due to strikes, severe weather and airport issues. This was partially offset by good progress in growing non-seat revenue, which increased by 18% driven by improvements to inflight food and drink ranges; some recovery in markets after the shock events of last year; and an increased load factor, up 0.5ppts to 90.2%.

Headline cost per seat increased by 4.9% to £54.45 driven by a forex impact of £175M, partially offset by lower fuel prices. At constant currency the headline cost per seat decreased by 4.1% due to the reduced fuel prices with costs excluding fuel and forex movements flat. The 16% reduction in constant currency fuel price was helped by a lower hedged fuel price, mitigating market price increases. The group has hedged 83% of fuel requirements in the second half at $577 per tonne with 60% hedged in 2018 at $516 per tonne. During the period the average market fuel price increased from $409 per tonne to $500 per tonne.

The group’s business passenger segment has performed well during the period. The total number of business passengers has increased by 6.2% against a backdrop of capacity investment weighted towards leisure routes. Business passengers remained at 19% of the group’s customer base, reflecting the mix of routes flown. The business passenger premium has remained steady year on year, helped by the recovery from shock events and the move of Easter into April. The group is now looking to evolve the product offering, drive better distribution and reduce costs. A new organisational structure is now finalised, contracts with travel management companies are being renegotiated and six major new corporate and government contracts were signed in the period, for example with the state of the Netherlands.

In the period the group has seen strong growth in its ancillary revenue, offsetting pressure on ticket yields. For example, they have seen good early results from new initiatives in their baggage strategy. They also have opportunities to build on their partnerships with brands in car rental and hotels as well as exploring other value channels with a number of projects in the pipeline for the next year. Non-seat revenue increased by 18% driven by improvements to inflight food and drink ranges with premium products being added.

During the first half of the year the group has focused their growth on maintaining market share in the UK and Switzerland and growing in France. They also invested in high capacity growth in Venice and Naples to improve their number one position; and maintained share in the slot-constrained Berlin and Amsterdam where the airport is now at full capacity. Having capitalised on time-sensitive opportunities to bolster its positions in primary airports such as Amsterdam during the period, further capacity growth is likely to be at a lower rate in 2018.

The group are now seeing signs that competitors are reducing their growth rates or even overall capacity for the forthcoming summer. Vueling is expected to reduced its capacity by around 5%; Norwegian is focusing more on low cost long-haul, reducing its short haul network at Gatwick; the combination of Air Berlin and Lufthansa in Germany is expected to result in a reduction of around 20 aircraft; Alitalia is in a state of administration (again) in Italy; and Flybe is expected to reduce capacity in 2018.

In the UK the group increased their capacity by 8% with significant growth targeted at maintaining their share of the London market through Luton and Gatwick and increasing capacity at Bristol and Manchester. In France they increased capacity by 12%, significantly ahead of the overall market, to consolidate their presence in Paris and increase their share in the regions. In Italy they increased capacity by 6%, further increasing their investment in Venice, Naples and Milan Malpensa.

In Switzerland they increased capacity by 9% increasing their share in both Geneva and Basel, against an overall market growth of 8%. In Germany they increased capacity by 9% as they maintained their strong market share of the Berlin market. In the Netherlands they have increased capacity by 7% as they began to annualise the high growth from the previous two years, focusing on adding frequencies to existing destinations. In Portugal they increased capacity by 17% as they continued to establish their position at Lisbon and Porto; and in Spain they increased capacity by 16% as they continued to build their presence in Barcelona. In March they opened their first seasonal base in Majorca with three aircraft based there over the summer.

During the period, cancellations and delays increased by 18% to 3,302 and OTP was 80%. The challenges of working at Gatwick, where the group outperforms most of its direct competitors on OTP, continue to have an impact on the rest of the network. In addition the group was affected by severe weather at peak times of the year; strikes at French ATC, Italian ground handling and Berlin ground handling; and reduced capacity as French ATC perform systems upgrades at Bordeaux. Since the Gatwick North Terminal consolidation the group has been able to improve operations and customer experience with more efficient ground handling processes and consistent turn times.

There were a number of non-underlying costs during the period. The sale and leaseback of the group’s ten oldest A319 aircraft resulted in a loss on disposal of the assets of £10M and a £6M maintenance provision. This is the first of a rolling programme of about ten aircraft a year to 2021 to de-risk the exit from the business of the ageing A319 fleet.

The implementation of an organisational review has resulted in costs of £2M with a further £8M expected over two years. Following the Brexit vote, the group is in the proves of establishing an AOC in another EU member state which has incurred £1M in setup costs with the one-off costs expected to total £10M over three years, mostly driven by the costs to re-register aircraft.

As of the period-end the group was contractually committed to the acquisition of 157 A320 family aircraft at a cost of $14.1M with 14 in the second half of the year, 34 in 2018 and 109 before the end of 2022. The group has agreed to purchase 30 A321 NEO aircraft under its existing agreement with Airbus with the first arriving in summer 2018. This is a conversion of 30 existing A320 NEO orders and will increase their ability to grow in slot constrained airports and manage costs.

Going forward, forward bookings are ahead of last year, at 77% for Q3 and 55% for the half year. The group’s capacity growth in the second half of the year is expected to be at a similar level to the first six months and RPS in Q3 is expected to decline by low single digits. Headline cost per seat excluding fuel at constant currency for the full year is expected to increase by around 1% which is better than initially expected. Overall the board’s current expectations for the full year are in line with current market expectations.

At the current share price the shares are trading on a PE ratio of 11.6 which increases to 13.8 on the full year consensus forecast. After a 1.4% reduction in the dividends paid the shares are yielding 4.3% which falls to 2.9% on the full year forecast. At the period-end the group had a net debt position of £333M compared to £424M at the year-end.

Overall then this has been a bit of a difficult period for the group. Losses widened, not helped by unfavourable forex movements and Easter being in the second half of the year, although even excluding these effects, losses worsened. The net asset level also declined but the operating cash flow improved with some free cash being generated. Operationally the revenue per seat decreased at the same rate at which the costs increased with continued competition expansion driving down prices in a low fuel cost environment. The costs were up due to forex movements. Excluding these, and fuel costs, which came down, and costs per seat were flat.

The non-seat revenue did do quite a bit better, however, and going forward the board seem to be expecting their competition to slow their growth. Despite this, however, I don’t think that the forward PE of 13.8 and yield of 2.9% offer enough compensation for the issues here.

On the 2nd June the group announced that Chief Commercial Officer Peter Duffy sold 5,000 shares at a value of just under £71K.

On the 14th July the group announced that their application for an AOC certificate to Austria’s Federal Ministry for transport, Innovation and Technology for an airline operating license. The accreditation process is now well advanced and they hope to receive the AOC and license in the near future. This will allow them to establish a new airline, EasyJet Europe, which will have an HQ in Vienna and will enable them to continue to operate flights across Europe after the UK has left the EU.

On the 20th July the group released a trading update covering Q3 with headline pre-tax profit guidance for the full year expected to be between £380M and £420M. Although the board expect capacity to continue to put pressure on yields, their progress this year has enabled them to upgrade this year’s forecast and demonstrates that the group once again has positive momentum.

Seats flown increased by 9.5% in the quarter and passengers increased by 10.8% which means load factor has increased by 1.1 percentage points to 93.1%. Revenue per seat at constant currency increased by 2.2% to £55.7. This was driven by the movement of Easter into the quarter, which saw a benefit of £55M; the increased load factor; and an underlying revenue trend that continued to improve into the second half of the year. This was offset by a continued low fuel price environment which is sustaining inefficient capacity in the market, driving fares down.

The group has launched a new website in all markets with enhanced functionality that makes it easier to use across all devices and simpler for customers to add ancillaries, and they have further optimised pricing algorithms. This has driven increased conversion rates, particularly in bag revenue.

The headline cost per seat improved by 5.5% in the quarter at constant currency, to £48.98, due to low fuel prices and a strong underlying cost focus offsetting inflationary pressure. Excluding fuel at constant currency increased as expected by 1.6% with a 0.6% increase in the year to date. For the full year the group is on track to deliver savings of around £80M and they remain on track to deliver flat headline cost per seat, excluding fuel at constant currency, from 2015 to 2019 assuming normal levels of disruption.

During the quarter the group appointed DHL to take over their ground handling operations at Gatwick starting in November. Net cash at the period-end was £426M compared to £368M at the same point of 2016.

The group has also announced that it has been awarded an AOC in Austria along with an airline operating license by Austria’s Ministry for Transport. These allow them to establish a new airline, headquartered in Vienna, and will enable the group to continue to operate flights within Europe following the UK’s exit from the EU.

It is estimated that at current exchange rates and with jet fuel remaining between $450 and $520 per tonne, that the fuel bill for the second half of the year is likely to decease by between £150M and £165M compared to the same period last year. Exchange rate movements are likely to have around a £20M adverse impact to profits in the second half and a £100M adverse impact in the year as a whole.

About 67% of expected bookings for Q4 have been secured. Based on this, revenue per seat at constant currency for the second half is expected to decline by around 2% and cost per seat excluding fuel is expected to rise by 1% in the full year. With the ongoing low cost of fuel allowing capacity to stay in the market, the group currently expects continued pressure on yields into the next financial year.

On the 15th September the group announced that they had submitted a proposal to acquire parts of Air Berlin’s short haul business. With Ryanair’s well-publicised problems and Monarch’s collapse, I actually think things should be quite good for Easyjet and I have bought back in here.

On the 6th October the group released a trading update. Passenger numbers for the quarter were a record 24.1M, driving a record load factor of 95.6%. There was a year on ear reduction in revenue per seat at constant currency of 3.7% during Q4 and a reduction of 1.4% in H2, which is slightly better than guidance due to the high load factors and a strong ancillary revenue performance. The group have grown capacity by 8% in Q4.

Headline cost per seat excluding fuel at constant currency is expected to increase by around 1% for the full year, in line with guidance. Headline cost per seat at constant currency including fuel is expected to decrease by 4.4% and non-headline costs are expected to be around £23M. Exchange rate movements resulted in a net adverse impact of £100M on pre-tax profit but the fuel bull is expected to decrease by between £230M and £235M with the full year headline pre-tax profit expected to be between £405M and £410M, at the upper end of previous guidance. Net cash at the year-end is expected to be £357M.

The group plans to grow capacity by around 6% for the coming year. Whilst revenue momentum continues to improve, the board expect continued pressure on yields reflecting ongoing market capacity growth that is currently forecast to be around 5% in Q1. Based on today’s fuel prices, unit fuel costs for the year are expected to benefit the group by between £125M and £145M and the total expected forex impact us expected to be a headwind of around £20M.

On the 27th October the group announced that it has signed an agreement with Air Berlin to acquire part of its operations at Berlin Tegel for a consideration of €40M. The acquisition will result in them entering into leases for up to 25 A320 aircraft and taking over other assets including slots. This, in addition to the existing base at Berlin Schonefeld will mean that they would be the leading airline in the city.

Overall I feel that things are improving for Easy Jet and I have made a purchase. As an aside, the group’s insistence in using the world “easyjet” at every opportunity (without capitals) instead of terms like “the group” or “them” makes the updates very hard to read – one of the worst I have seen actually!