Galliford Try is a UK housebuilding and construction group. The housebuilding division comprises Linden Homes which develops both private and affordable homes for sale, and Galliford Try Partnerships, a specialist affordable housing business. In construction the group is a major UK contractor, operating mainly under the Galliford Try and Morrison Construction brands. Their business works across the public, regulated and private sectors.

Linden Homes delivers around 3,000 houses and apartments each year, the majority of which are for private sale. The business has a south of England focus with an increasing presence in the North and Midlands and they embark on worth that include brownfield, refurbishment and regeneration projects. Galliford Try Partnerships is a specialist affordable housing contractor, providing services to housing associations and local authorities. It has a strong presence in the South East, Midlands and North East England and a growing business across the rest of the country. The business also develops mixed tenure projects, providing housing for sale on regeneration-led sites.

The construction sector contains Building, Infrastructure and PPP Investment businesses. Building serves a range of clients across the UK and was further enhanced by the acquisition of Millar Construction in 2014. Infrastructure carries out civil engineering projects, primarily in the highways, rail and aviation, environmental, water and waste, and power and security markets. PPP Investments delivers major building and infrastructure projects through public private partnerships. It leads bid consortia and arranges finance, makes equity investments, manages construction through its operations, and ultimately realises its investment to fund new projects.

In construction contracts, revenue comprises the value of construction executed during the year and contracting development sales for affordable housing. The results for the year include adjustments for the outcome of contracts, including jointly controlled operations, executed in both the current and prior years. In fixed price contracts, revenue is recognised based upon an internal assessment of the value of the works carried out. Profit is not recognised in the income statement until the outcome of the contract is reasonably certain. Adjustments arise from claims by customers or third parties in respect of work carried out, and claims and variations on customers or third parties for variations on the original contract.

In cost plus contracts, revenue is recognised based upon costs incurred to date plus any agreed fee. Where contracts include a target price consideration is given to the impact on revenue of the mechanism for distributing any savings or additional costs compared to the target price. Any revenue over and above the target price is recognised once the outcome is virtually certain. Profit is recognised on a constant margin throughout the life of the contract.

Provision will be made against any potential loss as soon as it is identified. Bid costs relating to PFI/PPP projects are not carried on the balance sheet as recoverable until the group has been appointed preferred bidder or has received an indemnity in respect of the investment or costs. Costs that are carried on the balance sheet are included within amounts recoverable on construction contracts, within trade and other receivables.

The company operated schemes under which part of the agreed sales price for a residential property can be deferred for up to 25 years. The fair value of these assets is calculated by taking into account forecast inflation in property prices and discounting back to present value using the effective interest rate. Provision is also made for estimated default to arrive at the initial fair value. The unwinding of the discount included on initial recognition at fair value is recognised as finance income.

It has now released its final results for the year ended 2015.

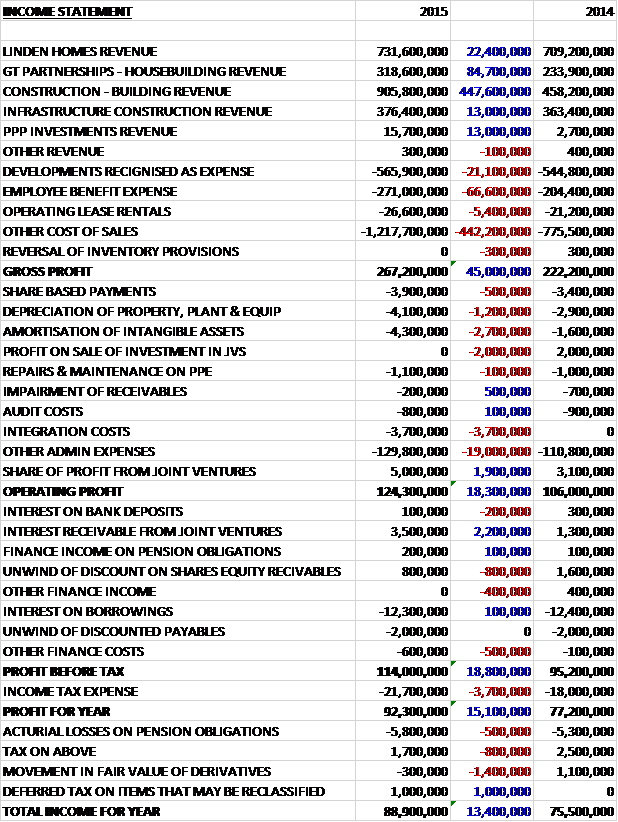

Revenues increased across all businesses when compared to last year with a £447.6M growth in construction building revenue, of which £400M was related to the acquisition of Millar Construction, an £84.7M increase in GT Partnerships housebuilding revenue and a £22.4M growth in Linden Homes’ housebuilding revenue. Developments as an expense increase by £21.1M, staff costs were up £66.6M and operating costs grew by £5.4M along with other cost of sales which increased by £442.2M to give a gross profit some £45M ahead of last time.

Depreciation and amortisation both grew modestly and we also see the lack of a £2M profit from the sale of investments in joint ventures that occurred last year along with £3.7M in integration costs relating to the integration of Millar Construction and other admin costs that grew £19M, partially offset by a £1.9M increase in the profit from joint ventures which meant that the operating profit was up £18.3M when compared to 2014. The interest receivable from joint ventures increased by £2.2M but this was offset by the £800K reduction in the unwinding of the discount on the shares as equity receivables, a £400K fall in other finance income and a £600K growth in other finance costs as well as a £3.7M growth in tax which gave a profit for the year of £92.3M, an increase of £15.1M year on year.

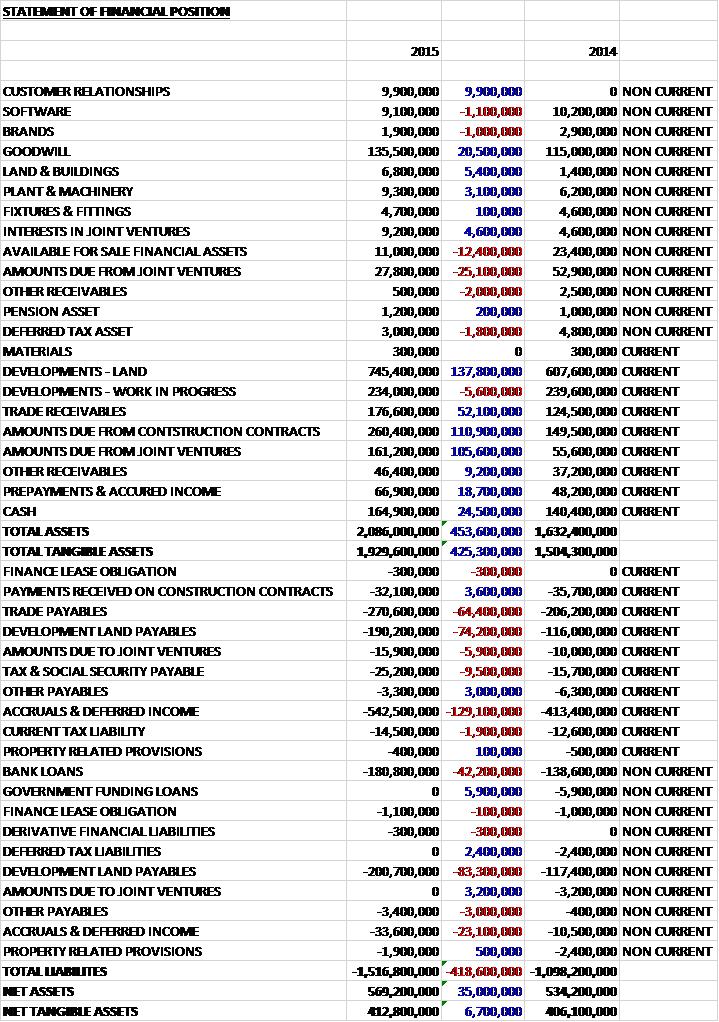

When compared to the end point of last year, total assets increased by £453.6M, driven by a £137.8M growth in land developments, a £110.9M increase in amounts due from construction contracts, an £80.5M growth in amounts due from joint ventures, a £52.1M increase in trade receivables, a £24.5M increase in cash and a £20.5M growth in goodwill. Total liabilities also increased during the year due to a £152.2M growth in accruals & deferred income, a £157.5M increase in development land payables, a £64.4M increase in trade payables and a £42.2M growth in bank loans. The end result was a net tangible asset level of £412.8M, an increase of £6.7M year on year.

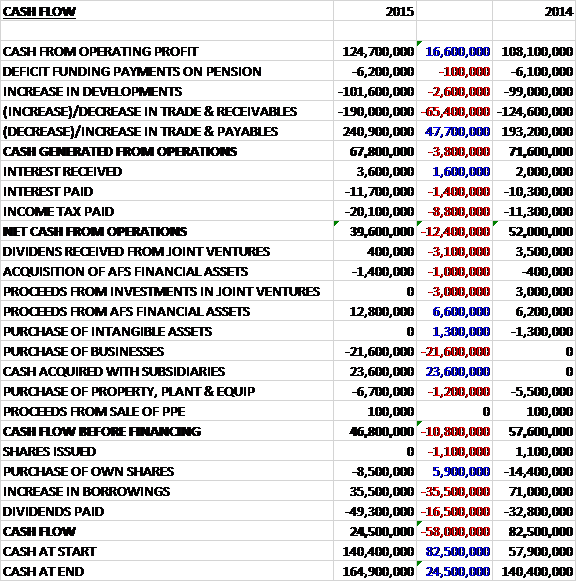

Before movements in working capital, cash profits increased by £16.6M to £124.7M. There was an outflow of cash through working capital, however, with a particularly large growth in receivables which, when combined to an £8.8M increase in tax paid, meant that the net cash from operations came in at £39.6M, a decline of £12.4M year on year. The group spent £6.7M on property, plant and equipment but received a net £11.4M from available for sale financial assets relating to the sale of most of the assets along with a net £2M from business acquisitions to give a cash flow of £46.8M before financing. For some reason the group took out an extra £35.5M in borrowings so it could pay its dividends and buy enough shares for employee schemes to give a cash flow of £24.5M for the year and a cash level of £164.9M at the year-end.

Government policy affects both demand and industry regulation. The Help to Buy scheme continues to benefit the market, particularly outside the South, as does the recent change to stamp duty. The planning environment remains positive but a shortage of planning officers in local authorities continues to cause delays. Housing associations are the main procurers of new affordable homes but provision of new homes by local authorities remain at very low levels.

Linden Homes increased both revenue and margin, with mortgage availability, the planning environment and the land market remaining positive. Galliford Try Partnerships grew faster than expected and the board see substantial potential for this business. Construction is benefiting from a rapidly improving market and the acquisition of Millar Construction with a good pipeline of opportunities at appropriate margins. Conditions in the supply chain remain challenging, however. The availability of materials has improved but it is still difficult to obtain skilled tradespeople, leading to cost inflation. The group took advantage of the continuing favourable land market to further increase the number of plots to a record 15,750, including 515 plots acquired with Shepherd Homes. In all, they have secured all the plots needed by the housebuilding businesses for 2016, and 87% for 2017.

The pre-tax profit at Linden Homes was £78.8M, a growth of £4.5M year on year with an operating margin of 16% compared to 15.1% last year on revenues that grew by 3% to £779M. The increase in revenues reflects a higher average selling price which rose 7% to £327K due to a product mix that moved towards more expensive homes and some price inflation, partially offset by a small reduction in unit numbers with completions down from 2,748 to 2,566. Prices benefited from a greater proportion of larger houses and further price inflation in an improving market. This revenue included sales of land into strategic joint ventures of £51.1M compared to just £7.2M last year. The margin improvement is attributed to the margin improvement plan, higher margin sites coming through from the land portfolio and a continued reduction in the proportion of legacy land. It is worth noting, however, that excluding the land sales, the operating margin increased from 14.6% to just 14.7%.

In July the business implemented operational restructuring in the South in order to improve their overhead leverage, generating savings in 2016 of £500K and annualised savings of £2M going forward. In June the group completed the sale of Linden Homes’ shared equity portfolios for £18.6M which was in line with the carrying amount on the balance sheet. The business had 62 active selling sites compared to 65 last year with sales per site per week declining slightly from 0.63 to 0.61 and they finished the year with sales in hand of £300M compared to £308M. The strategic land holdings stood at 1,500 acres at the year-end compared to 1,405 acres last year and they expect to generate more than 8,000 plots from this land.

Providing a proportion of affordable housing on their sites is often a condition of obtaining planning permission. During the year they formed new joint ventures with Home Group at Newhall in Harlow, and with Spectrum Housing Group, through which they will deliver new homes in the South West over the next fifteen years. The existing joint ventures with Thames Valley Housing, Aster Homes, Notting Hill Housing and Devon & Cornwall Housing all performed well.

Public land releases through the HCA’s delivery partner panel and the GLA have provided good land acquisition opportunities and the group continue to secure public land on deferred payment terms. The changes to social rent setting policy announced in the recent budget will have an impact on the tenure profile of affordable housing, but will not reduce underlying demand. The board anticipate some uncertainty in the short term as registered providers assess the impact and local authorities consider the potential in alternative tenures. Going forward, the housing market remains positive for the business but while supply chain conditions have eased somewhat during the year, the main challenge continues to be to deliver homes within expected timescales and costs.

The pre-tax profit at Galliford Try Partnerships was £8.6M, an increase of £4.2M when compared to 2014 with an operating margin of 2.9% compared to 2.1% last year on a 36% increase in revenues to £329.4M, of which £56.1M came from mixed tenure developments and £273.3M came from contracting. The operating profit was depleted by cost inflation incurred on the conclusion of some older contracts, in particular in the SE, but benefited from a transfer of land into a joint venture housing association. Looking forward, the intention is to allow the business to operate with a net debt position of up to £30M to accelerate its mixed tenure growth compared to a net cash position of £15M this year.

In June the business signed a development agreement with the GLA to construct 1,100 mixed tenure homes in Canning Town, with an approximate development value of £380M. This is the largest standalone housing scheme the group has ever undertaken and it is being delivered through the existing joint venture with Thames Valley Housing. The business also secured and commenced work on the £81M Great Eastern Quays project in East London for Notting Hill Housing. Other key wins included a £36M contract with ExtraCare Charitable Trust for a new retirement village which represents the seventh development for this client.

The increase in mixed tenure revenue contributed to the rise in margins as the business implemented its strategy to fund these developments using cash generated by the contracting operations. Their capability in land-led developments also contributed to the higher margin. For these schemes, the group finds sites, obtains planning permission for affordable housing and then sells the site on to a housing association client. At the year-end, the business’ contracting order book was £825M compared to £513M at the end of last year and at the same date the business had £43M of unit sales in hand. Going forward, the board see strong prospects for the business and have an opportunity to accelerate their growth in mixed tenure developments, by investing up to £30M of extra funding over the next few years to buy land for these schemes.

In construction, with strengthening market demand, the group are winning work with improved appraisal margins, although the results for this year are still constrained by older contracts. Revenue increased by 55% to £1.293BN, reflecting underlying growth and the contribution from Millar Construction. Profit from operations was £15.7M, an increase of £7.7M which represented a margin of 1.2%, up from 1% last year. The improving UK economy has led to increased activity, particularly in London and with clients in the hotels, leisure and office sectors.

As of the year-end, the order book was £3.5BN compared to £3BN the year before. Of the total order book, 72% was in the public sector (29%), 15% was in regulated industries (19%) and 13% was in the private sector (52%). Some 69% of the order book is in frameworks and the Miller Construction acquisition contributed to the increase and the change of sectoral split. In Building, the order book consists of a number of sectors with Education being the most important, followed by facilities management, health and commercial whilst in Infrastructure, the largest component of the order book is highways, closely followed by water with rail, flood alleviation and utilities making up the bulk of the rest of the order book.

The pre-tax profit in the building construction business was £1.3M, a decline of £2M year on year with a margin of 0.9% compared to 0.7% last time as cost inflation continued to impair profitability on contracts priced before current supply chain constraints arose. Last year’s results also benefited from £3.1M from disposing of three investments. Among the major contract wins, the business was one of six contractors appointed to all three lots of the Southern Construction Framework which allows all public bodies and local and central government in the Southern region to procure projects or programmes valued at £1M or above and the four year framework is worth up to £3.9BN in total.

The business was also one of 11 contractors appointed to the Medium Value lot of the North West Construction Hub, which has a framework value of up to £400M over four years. This allows public sector bodies across the North West to procure projects valued from £2M to £9M and follows their appointment to the high value lot in July 2014.

In the Education market they signed a £160M Priority School Building Programme contract with the Education Funding Agency, covering the NE of England. This was the first batch funded by the government’s new PF2 model to reach financial close. The construction contract is worth more than £103M, with a further £56.6M maintenance and life-cycle contract for the facilities management business. They also won EFA contracts for the North and NE Lincolnshire batch, worth £47.6M, and the Greenwich, Lewisham and Croydon batch (£45M). The Highland council awarded them a £48.5M Hub North Scotland contract to deliver a community campus in Wick, which will replace three existing schools.

Continuing their long term relationship with Frasers Property, they were awarded a contract to deliver three further phases of the Riverside Quarter residential development in Wandsworth. The contract has a total value of £69M and will involve the group building apartments for sale, affordable homes and commercial units. In Scotland, they won a place on the Next Generation Estates Contract framework for the MOD. This framework is worth up to £250M over four years, for projects with values of up to £12M, and is extendable for a further three years. They have also signed contracts with Birmingham City University to build a new £46M conservatoire in the Eastside region of the city.

The pre-tax profit in the Infrastructure business was £8.5M, a growth of £3M when compared to last year representing a margin that increased from 1.3% to 2%. The business continued to secure substantial new contracts. In December, as part of the Connect Roads consortium, they were appointed to design, build, finance and operate the £550M Aberdeen Western Peripheral Route. Two further major highway wins included their appointment by Highways England to its Collaborative Delivery Framework, where they are one of six contractors due to deliver up to £1.15BN of work over five years, and their appointment as part of a joint venture to its Smart Motorways programme, worth a total of £1.55BN.

In regulated markets, their joint venture with MWH Treatment and Black & Veatch was appointed preferred bidder by Scottish Water for its non-infrastructure Quality and Standards IV framework which is worth about £560M to the joint venture over six years. Southern Water appointed two of their other joint ventures to its AMP6 framework. These appointments ae expected to be worth around £215M over five years. Following the acquisition of Miller, infrastructure was also appointed to participate in the delivery of £250M of Network Rail Frameworks over five years.

Going forward, improving markets in the public and private sectors are leading to a positive pipeline of opportunities. The group remain focused on selecting work with appropriate risk and margin profiles and the Miller acquisition has significantly increased the order book and the number of frameworks they are now involved with, giving them a broader range of opportunities for which they can tender. Supply chain conditions remain challenging but the group’s cost estimates on new work reflect the inflationary conditions. They expect to increase margins during 2016 and remain on track for the 2018 margin target of 2%.

The pre-tax profit in the PPP Investments business was £3M, a positive movement of £4.8M year on year and included profit from sales of investments of £6.6M. The PPP market in England has seen the first PF2 funded projects finance work on the Priority School Building Programme and the group are awaiting announcements of further projects. In Scotland there continues to be a healthy and visible pipeline of PPP projects. The country uses the non-profit distribution model to finance a number of these projects. This is designed to ensure that contractors earn fair returns on their developments and a pilot programme is planned for Wales which could open up opportunities in that market.

During the year the group made new equity investments totalling £11.7M including the purchase of the Miller portfolio, and disposed of four investments generating the profit of £6.6M. PPP Investments continued to provide good opportunities for Galliford Try Partnerships and Facilities Management businesses, with projects closed during the year adding around £600M to the order books of these divisions and included the Aberdeen Western Peripheral Route and the first ever PF2 contract with the EFA.

Going forward the board believe the PF2 model works well and will allow public sector clients to drive good value for money for their projects. The project pipeline in Scotland and their strengthening position through Miller Construction makes them confident about the prospects for PPP Investments.

Galliford Try Partnership’s good prospects mean the board are increasing their revenue and margin expectations going forward. Having targeting 2018 revenue of around £350M, they are now aiming to exceed £400M. The margin target is now at least 4% against the original target of 3.5% to 4%. Due to the acquisition of Millar Construction, they are increasing Construction’s 2018 revenue target from £1.25BN to £1.5BN while retaining their margin target of 2%. They also intend to growth the housebuilding land bank to around 14,000 and then maintaining it at around this level. In construction, they are looking to increasingly become a collaborative investment partner for public sector clients to give access to a pipeline of projects rather than one-off bids.

Last year the group disposed of its investment in gbconsortium2 ltd for £3M giving rise to a profit of £2M. Their available for sale financial assets comprise PPP investments and shares equity receivables. During the year they sold the majority of their shared equity portfolio which meant that the net investment in shared equity receivables fell by £21.5M and the sale generated a profit on disposal of £400K. The £10.3M of additions represent equity securities acquired with Millar Construction and additional subordinated loans of £1.4M were made to its PPP investments, and the group disposed of interests held at £2.6M for a profit of £6.6M.

In July 2014 the group acquired the Millar Construction business from Millar Group Holdings for a total price of £16.6M in cash. The business is a UK only construction company which delivers building and infrastructure projects to both the public and private sectors. The acquired order book of £1.4BN doubled the group’s existing order book in construction to £2.8BN. The acquisition generated goodwill of £20.2M and came with further intangible assets of £12.1M. The group has so far spent £3.7M in exceptional integration costs and is expecting to generate synergy saving of more than £8M per annum compared to initial expectations of £7M.

In May 2015 the group exchanged contracts with Shepherd Homes to acquire its Yorkshire based housebuilding land assets comprising six current sites and five sites in planning totalling a land bank of 515 plots. The consideration of £30.9M is subject to finalisation based on actual results and £25.9M remained unpaid at the end of the year and is included within development land payables. The acquisition generated goodwill of just £300K and contributed £1.7M in gross profits since its acquisition.

There is a good split of customers with the largest being major water industry customers accounting for about 4% of revenues. Other risks include the level of UK house prices which are affected by factors such as mortgage availability, employment levels, interest rates and consumer confidence. At the end of the year the group’s house price linked financial instruments consisted of shared equity receivables held as available for sale financial assets and the sensitivity to house price inflation and discount rates was not significant. As well as being indirectly susceptible to interest rate increases, the group also has some debt and a 1% increase in rates would result in an £800K fall in profits, all else being equal. There remains some £211.4M of undrawn borrowings available to the group.

As can be seen, the pension scheme is currently running at a small surplus, which is a great state of affairs and with the present value of all the obligations standing at £218.9M, the scheme doesn’t really represent a massive risk in my view given the size of the company. The contributions expected to be paid into the scheme in 2016 are £5.8M.

The fact that the group has both housebuilding and construction businesses gives them some diversity. Housebuilding adapts quickly to economic changes, particularly during a recovery, while long contracts and lead times make Construction late cycle. This means that if one business turns down the other remains strong, reducing economic risk. Construction generates cash from regular payments whilst Housebuilding uses cash to pay for land and development so once again, these are complementary but unfortunately being earlier in the cycle, the cash absorbing Housebuilding comes before the more regularly cash generating construction business.

There were a number of board changes during the year. Amanda Burton retired as a non-executive director and Ian Coull stepped down as Chairman due to his other commitments. Having announced his intention to retire as CEO at the end of 2015, Greg Fizgerald became Executive Chairman on an interim basis and will become non-executive chairman from January 2016. In October, Peter Truscott joined as the new CEO and Peter Ventress joined as deputy Chairman, replacing Peter Rogers who retired. Peter Ventress will take over as non-executive Chairman in November 2017. The group also appointed Gavin Slark as non-executive director and promoted Ken Gillespie to COO.

Going forward, in housebuilding the UK’s supply of new homes continues to fall short of demand. The outlook for Linden Homes remains strong with the mortgage and land market and the planning environment all positive. The main issue is building to schedule, given the shortage of skilled people. In Galliford Try Partnerships, affordable housing remains high on the political agenda, with renewed emphasis on home ownership products. Despite the challenges in welfare reform and the recent rent cuts, housing associations remain financially robust and are continuing to leverage their balance sheets to support mixed-tenure developments. This gives the group continued confidence of growth at the business and will support longer term margin improvement as clients require mixed tenure expertise. Construction’s markets are improving and, with increasing opportunities for new work, the board remain confident that margins will move up to their 2018 target.

After a 28% increase in the dividend for the year, the shares are yielding 4.9% which increased to a hefty 5.7% on next year’s forecast with the group looking to reduce dividend cover from 1.7 times to 1.5 times which is cutting it a bit fine in my view. At the current share price the shares are trading on a PE ratio of 12.6 which falls to 11.1 on next year’s consensus forecast. At the end of the year, the group had net debt of £17.3M compared to a net debt position of £5.1M at the end point of last year. Although it should be noted that the year-end position if flattering and the average net debt during the year was £168M with the group increasing their use of debt to fund the growth of the housebuilding operations.

On the 13th January the group released a trading update covering the first half of the year. All three of the businesses are trading in line with board expectations in positive market conditions. Net debt increased to £95M from £35.9M at the same point of the prior year, reflecting additional investment in Linden Homes and Partnerships.

At Linden Homes, good progress was achieved on operating margin against the same period of last year. Revenue is expected to be 5% higher from a net 1,171 of unit completions, down from the 1,278 recorded last time and within this total, private sales were higher while affordable sales of 233 units were below the previous period. Average outlets increased to 76 compared to 62 at the year-end point and the average selling price for private sales was up 8% at £334K with the combined private and affordable average selling price increasing to £295K. Initiatives to rationalise operating processes targeting a reduction in overheads by about £5M per annum have been put forward with the effect being at least earnings neutral in the current year with the full savings expected in 2017. Also, the group have brought forward plans for an additional business unit in West Yorkshire, building on the integration of Shepherd Homes.

In GT Partnerships, contracting revenue was below the first half of last year, reflecting some delays in procurement by registered providers immediately following the changes announced in the summer budget. The impact of these changes have now largely been assimilated with the effect likely to be positive for the business. The operating margin is likely to be ahead of the first half of last year, reflecting progress in increasing the proportion of mixed tenure, and the board are considering options to accelerate the growth of the business, including bringing forward the opening of a sixth office this year.

In Construction, the order book increased from £3.2BN to £3.7BN in an improving market. Some 98% of projected revenue for the current year is secured with 66% of the revenue for 2017. The business continue to make progress in concluding legacy contracts whilst seeing improved margins on new work.

Overall market conditions have remained positive, with build cost increases stabilised to a manageable level. Looking ahead to the second half of the year, the board believe they are in a strong position to deliver results in line with their expectations.

Overall then, this has been a good year for the group. Profits were up, and net tangible assets increased modestly. The operating cash flow did decline but this was due to a growth in tax and receivables and the cash profits increased. There was a decent amount of free cash generated but this was not enough to cover both the dividends and the shares for the share schemes. Linden Homes is really the main profit driver and is performing well at the moment, driven by an improved mix of homes and some price inflation.

The other divisions are all pretty low margin operations. GT Partnerships is performing well, with margins increasing to 2.9% and the order book look strong, although in the first half of 2016 the business has been affected by the budget announcement which caused some delays to projects. The Infrastructure business increased its wafer thin margins to 2% and seems to be winning some good business but the Building Construction business has margins that are still under 1% due to the effects of cost inflation on some legacy contracts.

The fact that the CEO has stepped down does add some extra risk in my view and of course, the group is very susceptible to the general market sentiment, although the infrastructure division might add some stodge I guess. The dividend yield of a hefty looking 5.7% going forward but the cover is too thin for my taste to be honest, although the forward PR of 11.1 does suggest some value here. A tricky one this, it does seem a quality business and I might look to enter on weakness if the market doesn’t completely collapse!

Having had a further think about this, I am a little uncomfortable with the reduction in the dividend yield at the same time as the gearing up in debt as I don’t think this is how a company should be run. Therefore, unless something changes on this regard I won’t be updating this company regularly.