Games Workshop has now released its interim results for the year ending 2016.

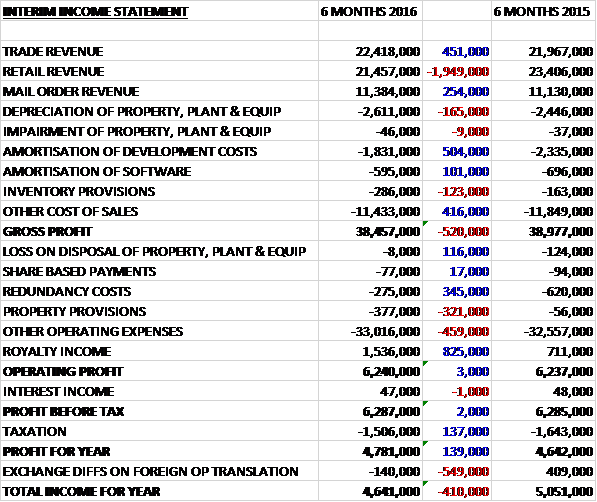

Revenues declined when compared to the first half of last year (although there was a modest increase on a constant currency basis) as a £451K growth in trade revenue and a £254K increase in mail order revenue was more than offset by a £1.9M decline in retail revenue. Depreciation was somewhat higher but amortisation fell by £600K along with other cost of sales but this was not enough to prevent a £520K fall in gross profits. We then see a £345K improvement in redundancy costs offset by a £321K increase in property provisions and a £123K growth in other cost of sales but due to an £825K increase in royalty income, the operating profit was flat. After a £137K reduction in the tax charge, the profit for the half year came in at £4.8M, an increase of £139K year on year.

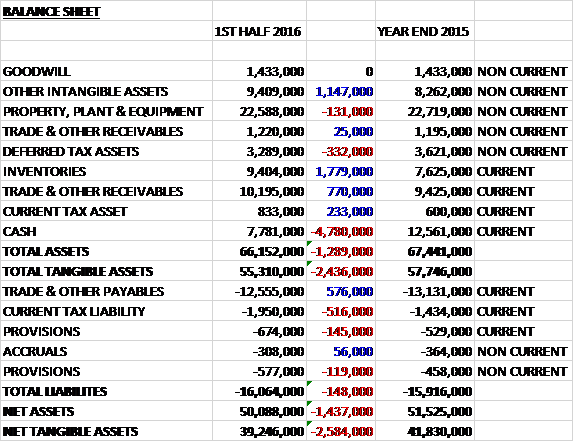

When compared to the end point of last year, total assets declined by £1.3M driven by a £4.8M fall in cash, partially offset by a £1.8M growth in inventories and a £1.1M increase in intangible assets. Total liabilities increased modestly as a £516K growth in the current tax liability was offset by a £576K fall in payables. The end result is a net tangible asset level of £39.2M, a decrease of £2.6M over the past six months.

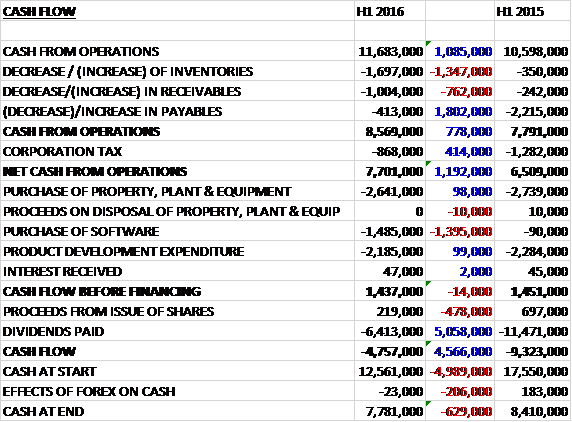

Before movements in working capital, cash profits increased by £1.1M to £11.7M. This was eroded somewhat by a growth in working capital requirements but after a decline in tax paid, the net cash from operations was £7.7M, a growth of £1.2M year on year. The group spent £2.6M on fixed tangible assets, £2.2M on product development and £1.5M on software which gave a few cash flow of £1.4M. This was nowhere near enough to cover the £6.4M paid out in dividends so that the cash outflow for the half year was £4.8M and the cash level at the period-end was £7.8M.

Overall, the fall in operating profits was almost entirely due to currency difference which accounted for a loss of £900K during the period. On a constant currency basis, profits were broadly flat.

Within the Trade division, there was an increase in revenue in Europe, North America and Asia with declines in Australia and non-core trade. The operating profit in the division was £5.8M, a decline of £188K year on year. During the period, the net number of trade outlets increased by 61 accounts and to broaden the core trade products reach, a small new product range has been designed and distribution agents have been signed up to sell the product to North America.

Within the Retail division, there was in increase in non-core revenue but declines in all other areas due to adverse currency effects, although North America and Asia were both nearly the same year on year. The operating loss in the division was £2.5M, a deterioration of £1.4M when compared to the first half of last year. The group opened 22 one man stores and three multi-man stores in the period. They also started their trial of four multi man format stores in high footfall locations in Sydney, Munich, Paris and Copenhagen. After closing 13 stores the total number of stores at the period-end was 430.

Within the Mail Order division, there was a strong growth in Citadel and Forge World revenue, partially offset by a decline in non-core revenue due to falls in sales in digital, export and the book trades. The operating profit in the division was £6.2M, an increase of £297K year on year. The group did well to increase royalties, more than doubling to £1.5M during the period, and the operating profit in the Product and Supply division was £4.1M, a growth of £601K when compared to the first half of 2015.

At the period-end, the group has capital expenditure contracted for but not yet incurred of £867K which included the replacement of the local area network in Nottingham and tooling & machinery spend. Recent projects include the European ERP system replacement which remains on track, the Forge World mail order store which was launched in August, and the Mail order warehouse system replacement which has been postponed until after the busy December trading period.

December sales were below expectations across the group and at this stage in the year, internal projections indicate that pre-tax profit for the year as a whole unlikely to exceed £16M.

Overall this has been a mixed half year period for the group. Profits did increase, but this was attributable to a fall in tax and pre-tax profits were flat year on year. Net assets declined over the period but the operating cash flow improved, although due to higher capex, the free cash flow was flat and not enough to cover the dividends. The main issue actually seems to have been adverse forex movements without which, profit would have been much improved. The operating profit in the trade business fell, and the losses increased in the retail business.

Performance was better in the mail order business along with the product and supply division, and there was a strong increase in royalty income.

Unfortunately the second half of the year has not started well with December sales below expectations so I will not be buying shares until this improves.

On the 6th June the group released a trading update covering the year ended 2016. The board expect profit to be slightly above market expectations due to earning more licensing income than expected. Over the year, sales have been largely flat year on year, however. Strangely this update led to Peel Hunt lowering its prediction for profit which has thoroughly confused me!