GSK has now released its results for Q2/H1 2015.

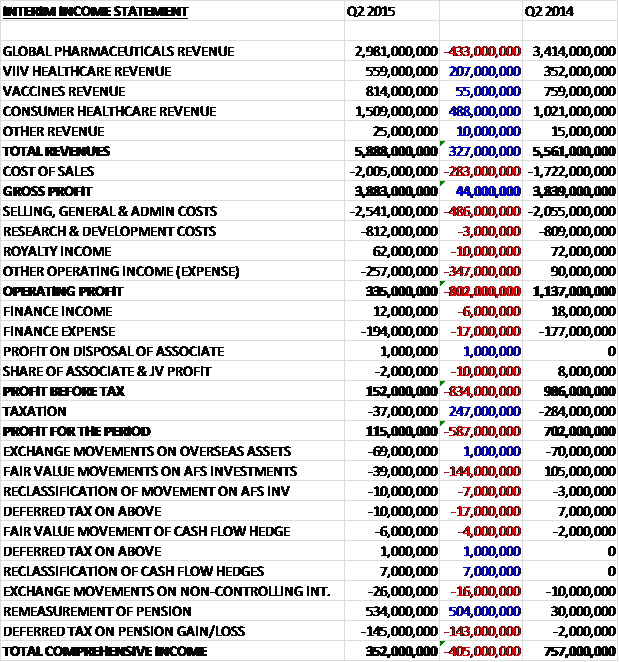

When compared to Q2 last year, total revenues increased by £327M as a £433M fall in global pharmaceutical revenue was more than offset by a £488M increase in consumer healthcare revenue, a £207M growth in ViiV healthcare revenue and a £55M increase in vaccines revenue. Cost of sales also increased to give a gross profit some £44M ahead of last year. Sales and admin costs increased by £486M and there was a £347M negative swing in other operating expense which meant that the operating profit was £802M lower than in the same quarter of last year. After finance expenses of £194M and a considerably smaller tax bill, the profit for the quarter stood at £115M a crash of £587M when compared to the same period of 2014.

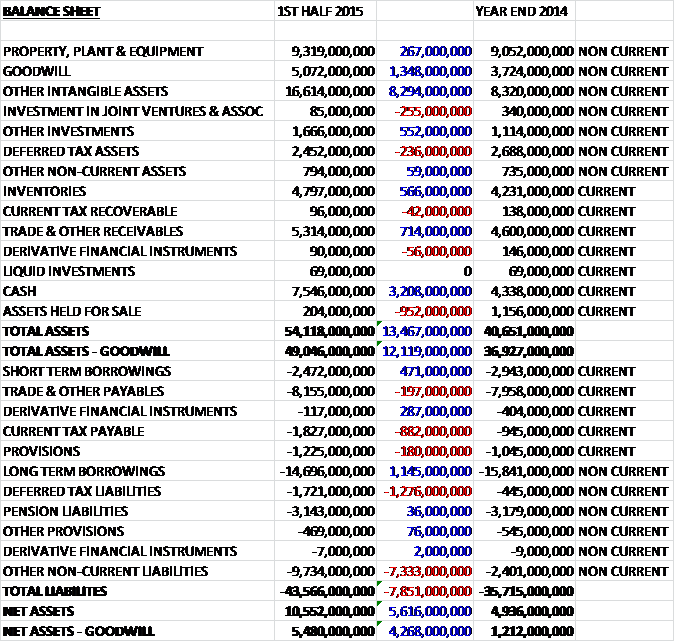

When compared to the end point of last year, total assets at the half year point were some £13.467BN higher, driven by an £8,294BN increase in intangible assets, a £3.208BN growth in cash, a £1.348BN increase in goodwill, a £714M increase in receivables, a £566M growth in inventories and a £552M increase in other investments, partially offset by a £952M fall in assets held for sale, a £236M decline in deferred tax assets and a £255M fall in the value of investments in associates and joint ventures. Liabilities also increased during the half year as a £7.333BN increase in other non-current liabilities relating to the potential requirement of GSK to purchase the rest of the consumer healthcare joint venture with Novartis, a £1.276BN increase in deferred tax liabilities and an £882M growth in current tax payable was partially offset by £1.145BN fall in long term borrowings, a £471M decline in short term borrowings and a £287M fall in derivative financial instruments to give a net asset level, excluding goodwill, of £5.48BN, an increase of £4.268BN when compared to the end of 2014.

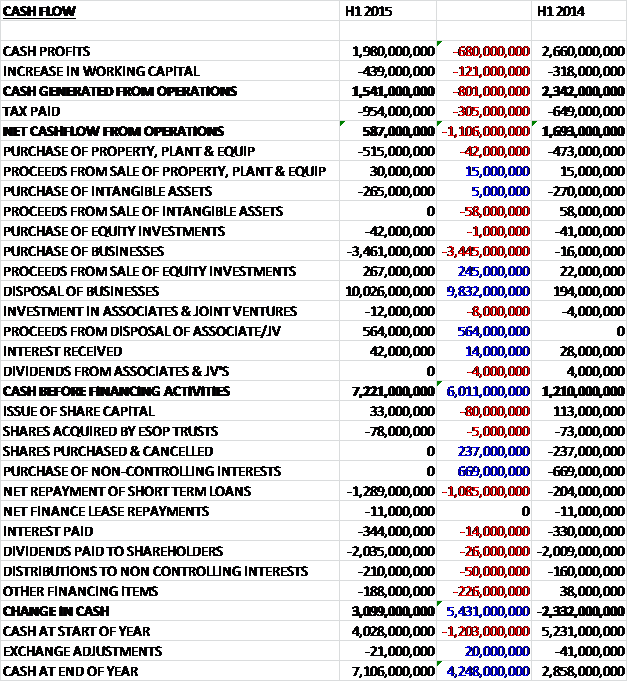

Before movements in working capital, cash profits fell by £680M to £1.98BN. This fall was exacerbated by adverse working capital movement and a higher tax bill to give a net cash from operations of £587M, a decline of £1.106BN year on year. The bulk of this cash (£515M) was spent on fixed assets and intangible assets accounted for £265M so that there was no free cash flow. The group then spent £3.461BN on acquisitions but received £10.026BN from the disposal of the businesses to Novartis and £564M in proceeds from the disposal of an associate so that the cash inflow before financing stood at a hefty £7.221BN. The group used some £1.289BN in repaying loans, £344M went on interest payments and over two billion pounds was spent on dividends to give a cash inflow for the half year of £3.099BN to give a cash level of £7.106BN at the period-end.

The total operating profit of £335M was considerably impacted by non-core items which resulted in a net charge of £1.014BN. The core profit for the period would actually have been £936M comparted to £982M this time last year so much better than it initially appears. There was an intangible asset amortisation charge of £125M but this seems to occur each year so I am not sure if this is really “non-core”. The major restructuring charges probably are, though, to some extent as within the £515M charge this quarter was the acceleration of a number of restructuring projects following the completion of the Novartis transaction. Legal charges of £50M are probably ongoing costs in a company like this so should not be ignored. The £322M charge relating to acquisitions and other items included the unwinding of the discounting effects on both the contingent consideration for the ViiV healthcare joint venture and the consumer healthcare joint venture put option. Other items also included equity investment and asset disposals, one-off regulatory charges in R&D and certain other items.

Overall sales grew 7% on a reported basis and 2% on a pro-forma basis (the reported figures include four months turnover for the former Novartis vaccines and consumer healthcare products and exclude sales of former GSK Oncology products from the start of March). New product performance was positive in all three of the businesses with the standout performance coming from the new HIV drugs, Tivicay and Triumeq. Both of these are tracking ahead of recent launches and together generated sales of £294M. Elsewhere saw continued strong uptake for Flonase OTC, an improving market share for Beo Ellipta following the indication for asthma granted in April and continued uptake for the newly acquired Meningitis vaccines Bexsero and Menveo. Interestingly the growth of the new products is now more than offsetting declining sales of Seretide which is a great result really.

Sales of respiratory pharmaceuticals fell by 6% to £1.467BN quarter on quarter. Seretide sales fell by 13% to £960M, Flixotide sales decreased 10% to £159M and Ventolin sales rose 2% to £160M. Breo Ellipta recorded sales of £53M and having been launched in the US, Europe and Japan recorded sales of £15M. In the US, sales declined by 12% to £704M reflecting a 5% volume growth but a 17% negative impact of price and mix. This decline included the price and mix impact of new contracts agreed last year in response to competitive pressure in the market where Advair and Breo Ellipa compete. European respiratory sales were down 8% to £369M with Seretide down 16% to £267M reflecting the expected pressures of increased competition from generics and the transition of the portfolio to newer products. Relvar Ellipta, approved in Europe for both COPD and Asthma, recorded sales of £19M in the quarter while Anoro Ellipta, with launches underway in many countries throughout the region, recorded sales of £3M. Respiratory sales in the ROW region grew by 5% to £394M with emerging markets up 4% and Japan benefiting from comparison with a weak Q2 2014, up 17%.

Sales in the cardiovascular, metabolic and urology category rose 5% to £242M with the sales of Prolia increasing by 38% to £11M reflecting the impact of the termination of the joint commercialisation agreement with Amgen in some European markets, Mexico and Russia in Q2 2014. In the US, generic competition to both Avodart and Jalyn is expected to begin in Q4 2015 which will impact sales next year. Immuno-inflammation sales were up 27% to £56M driven by US sales of Benlysta and in other pharmaceuticals, sales were down 6% to £542M as dermatology sales fell by 8% as a result of supply constraints due to capacity limitations while Augmentin sales increased by 2% to £143M. Relenza sales more than doubled to £33M, partly driven by the timing of US CDC orders and sales of products for rare diseases increased by 2% to £94M including sales of Volibris which were up 8% quarter on quarter.

Established products turnover fell 5% to £655M with sales in the US down 16%. Lovaza sales fell 22% to £24M as the impact of generic competition started to annualise. Europe was down 13% to £121M with Serevent sales down 23% to just £9M. ROW sales were up 3% to £366M with higher sales of Amoxil, up 77% to £22M and Valtrex, up 71% to £33M following the regaining of exclusivity in Canada until October. These gains were partially offset by a 26% decline in sales of Zeffix in China.

The one saving grace really was HIV sales which increased by 59% to £559M in the quarter with the US up 84%, Europe up 46% and ROW up 26%, all driven by Tivicay and Triumeq. The ongoing roll-out of Tivicay resulted in sales of £145M and Tiumeq, now launched in the US and much of Europe recorded sales of £149M. Epzicom, which benefited from use in combination with Tivicay, increased 1% to £185M but Selzentry sales fell 18% to £31M. There were also continued declines in mature portfolio, mainly driven by generic competition to both Combivir and Lexiva.

Vaccine sales grew 11% to £814M with the US up 13%, Europe up 27% and ROW down 2%. The business benefited from the sales of the newly acquired products, primarily Bexsero in Europe and Menveo in the US. On a pro-forma basis, sales for the quarter actually declined by 5% primarily reflecting the phasing of tenders in international markets for Synflorix and Havrix, together with competitive pressures on Infanrix. In the US, reported sales grew 13% but declined 5% on a pro-forma basis due to the 12% decline in Infanrix sales as a result of the return to the market of a competitor vaccine, partly offset by growth in the Meningitis portfolio, Rotarix and Boostrix sales.

In Europe sales grew 27% on a reported basis and 12% pro-forma. This growth primarily reflected increased sales from Bexsero, mainly driven by the UK NHS immunisation programme along with Portugal and Italy. The period also benefited from improved supplies of Boostrix, up 31% which was partly offset by a 15% decline in sales of Hepatitis vaccines, reflecting supply constraints as well as tender phasing, together with an Infanrix sales decline of 3% which was also impacted by the introduction of a competitor vaccine and the phasing of shipments in several countries. ROW sales fell 2% on a reported basis and 16% on a pro-forma basis due to a decline in Brazil, the Middle East and North Asia due to the phasing of tenders, partly offset by growth of Synflorix in Africa.

In Consumer Healthcare, turnover grew 51%, benefiting significantly from the first full quarter’s sales of the newly-acquired products. On a pro-forma basis, growth was 6%, of which 4% related to volume and 2% related to price. This principally reflected the strong growth in the US following the launch of Flonase OTC. Also, momentum from Q1 launches drove innovation contribution with sales from products introduced in the last three years representing about 15% of sales in the quarter. US sales grew 28% on a pro-forma basis.

As mentioned, Flonase was the region’s primary growth driver and with quarterly sales of £45M the brand has contributed to the category growth of 15%, achieving 11% market share in the period. Oral health sales were driven by Sensodyne, which continued its strong performance with growth of 27%, helped by improved supply and the launch of Sensodyne Repair and Protect Whitening. Excedrin grew 25% in the quarter due to a strong base business performance combined with new variant launches and price increases. Nicorette Mini lozenges and alli continued their recovery from supply shortages last year and Tums started to recover from Q1 interruptions.

Sales in Europe grew 7% on a pro-forma basis. Oral health products reported growth of 11%, helped by improved supply relative to Q2 2014, but also reflecting strong performances from Sensodyne due to new advertising in key markets and the roll-out of Sensodyne True White in the UK, Sensodyne Repair and Protect in Germany, and Sensodyne Mouthwash across a number of markets together with some supply recovery of Aquafresh. In Wellness, Voltaren grew 18% with strong performances across the region, particularly in Germany with strong marketing support behind a new advertising campaign.

ROW sales declined by 2% on a pro-forma basis. India continued to perform well with double digit growth reflecting distribution expansion, enhanced marketing campaigns and the achievement of a four year market share high for Horlicks. Oral health sales continued to show growth in the region, up 9%, driven by Sensodyne but sales in Wellness were affected by the negative impact of reducing channel inventories in the acquired consumer businesses.

The core operating profit at the pharmaceuticals business was £1.116BN, a fall of 1% when compared to Q2 last year on a constant currency basis. The core operating margin was 2.5 percentage points higher on a pro-forma basis, reflecting strong growth in HIV partly offset by continued pricing pressure in global pharmaceuticals, particularly respiratory products. Vaccines operating profit fell by 32% to £177M with the operating margin down 12.5% on a constant currency basis, primarily driven by the cost base of the former Novartis business. The pro-forma margin declined by 1.3 percentage points reflecting mix changes and additional supply chain investments, partially offset by reductions in R&D. Consumer Healthcare operating profit was £108M, an increase of 41% quarter on quarter but on a pro-forma basis, the operating margin was 0.6 percentage points lower driven by a one-off sales tax settlement which impacted the operation margin by 1.3%.

The new pharmaceutical and vaccine products that have been tasked with providing growth for the next five years showed a £322M sales growth, a rate in excess of 100% and they now represent about 10% of Pharmaceuticals and vaccines turnover. As already mentioned, it was the new HIV drugs that really drove proceedings with Triumeq sales of £149M and Tivicay sales of £145K. Sales of Relvar/Breo Ellipta are also starting to gain traction, more than doubling at £53M with the next most important contributor being Bexsero which more than doubled to £30M. In all, it is expected that the new pharmaceutical and vaccine products will deliver at least £6BN in revenue per annum by 2020.

Since the end of Q1, it has been quite a quiet period for the group’s pipeline of new products but there have been a number of milestones. There was the start of a phase 3 study of the combination use of Dolutegravir and Rilpivrine; the FDA AdCom recommended US approval of Nucala for adult patients with severe asthma with eosinophilic inflammation; Nucala was filed in Japan for sever eosinophilic asthma; and there was a positive CHMP opinion for Mosquirix.

Core EPS for 2015 is expected to decline at a percentage rate in the high teens due to continued pricing pressure on Seretide in the US and Europe, the dilutive effect of the Novartis transaction and the inherited cost base of the Novartis businesses. In 2016 the group expects to see a significant recovery in core EPS with a double digit percentage growth as the adverse impacts of 2015 diminish and the sales and synergy benefits of the Novartis transaction contribute more meaningfully. The strong Sterling continued to adversely affect the group and if the rates were to hold at the current level for the rest of 2015, the estimated adverse impact on turnover would be around 2% and the adverse effect on core EPS would be 6% so this is significant.

At the period end, the net debt stood at £9.553BN compared to £14.377BN at the end of last year. The group has maintained the quarterly dividend at 19p per share which represents a rolling annual dividend of 5.8% which is rather spectacular.

Overall then, things continue to be difficult for GSK but these results may not have been as bad as people were expecting. Profits in the quarter were indeed lower than Q2 last year, but strip out the restructuring following the Novartis transaction and things don’t look so dire. Net assets improved over the end of last year, mainly due to intangible assets gained from Novartis and the cash position is much better, again due to cash received from Novartis although operational cash flow seems rather poor and there is no free cash at the moment.

Seretide sales continue to be battered due to lower prices in the US and Europe but the good news is that the new product sales are stepping up to take the slack with the two new HIV drugs doing particularly well. Seretide is still by far the biggest contributor to sales though so there is probably still further to go and now it seems Avodart could be in trouble next year. There are also foreign exchange headwinds to look out for with the strong pound really taking its toll on top of the operational issues. Despite this though, with the strong contribution from the HIV drugs and the stonking 5.8% dividend yield still on offer this looks to me like it might be worth investing in again and I am thinking about re-entering.

On the 20th August the group announced that they had divested the rights in ofatumumab for auto-immune indications including MS to Novartis for a potential consideration of $1M. Novartis had already required the oncology indications for the drug and after this transaction they will own rights to all indications. Novartis will pay $300M in cash initially with a $200M payment subject to the start of a phase 3 study in relapsing remitting MS. Further contingent payments of up to $534M will be payable on the achievement of certain other development milestones. Novartis will also pay royalties of up to 12% on any future net sales of ofatumumab in auto-immune indications. This looks like a sensible deal to me.

On the 8th September the group announced the results from the study to understand mortality and morbidity in COPD for Relvar/Breo Ellipta. The study involved 16,485 patients who had COPD with moderate airflow limitation and either a history or increased risk of Cardiovascular disease. For the primary end point of the study, the risk of dying was 12.2% lower than on a placebo, which was not statistically significant.

For the first of the two secondary endpoints, the drug reduced the rate of lung function decline by 8mL per year compared with the placebo but as the primary end point was not met, statistical significance cannot be inferred from this results. For the secondary endpoint, the risk of experiencing an on-treatment cardiovascular event at any time was 7.4% lower than the placebo patients, which was not statistically significant.

This seems like a bit of a disappointing result. Whilst it seems the drug is somewhat effective, the results were not good enough to be statistically significant.

On the 17th September it was announced that director Dr Dexter purchased 7,655 shares at a value of nearly £100K.

On the 23rd September, ViiV Healthcare announced data from the phase III SRTIIVING study which evaluated the efficacy, safety and tolerability of switching from an antiretroviral therapy to the once-daily fixed dose Triumeq in virology suppressed adults with HIV. The study met its primary endpoint, demonstrating that viral suppression was non-inferior for patients switching.

On the 24th September the group announced that the CHMP of the EMA issued a positive opinion recommending marketing authorisation for mepolizumab, which will be commercialised under the brand name Nucala, as an add-on treatment for severe refractory eosinophilic asthma in adult patients. The final decision will be made by the European Commission and is expected before the end of 2015. This drug is not currently approved for use anywhere in the world and regulatory applications have been submitted in the US and Japan also.

On the 20th October the group announced positive results from two studies comparing the efficacy and safety of Incruse Ellipta to two available bronchodilator treatments (tiotropium and glycopyrronium) when used by patients with COPD. Results from one study achieved a statistically significant improvement in lung function at 12 weeks compared to tiotropium and the other study shows that it was non-inferior to glycopyrronium.