GSK has now released its results for Q3 2015.

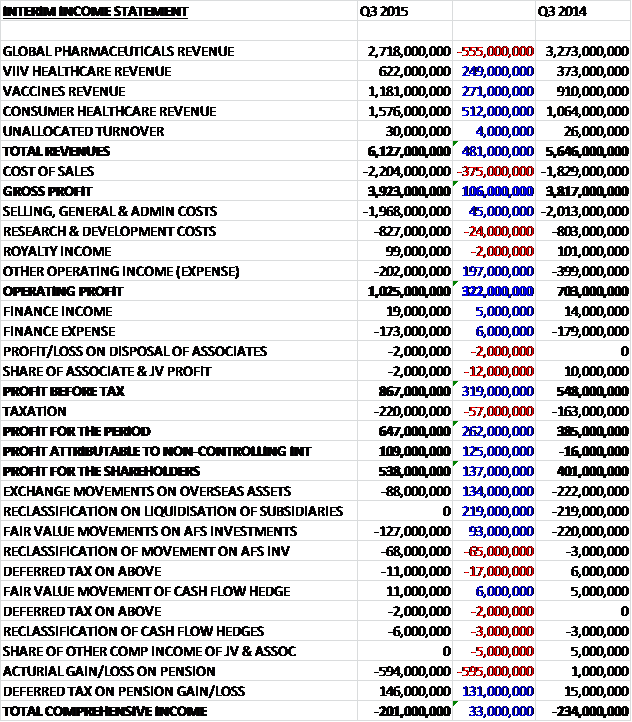

Revenues increased when compared to Q3 last year as a £555M fall in global pharmaceuticals revenue was more than offset by a £512K increase in consumer healthcare revenue, a £271M growth in vaccines revenue and a £249M increase in ViiV healthcare. Cost of sales also increased to give a gross profit £106M higher than last time. Selling costs actually fell during the period and other expenses declined by £197M so that the operating profit increased by £322M. Finance costs were broadly similar but tax was higher and there was a much larger increase in the profit attributable to non-controlling interests due to the greater contribution from ViiV healthcare. The end result was a profit attributable to the equity owners of £538M, a growth of £137M year on year.

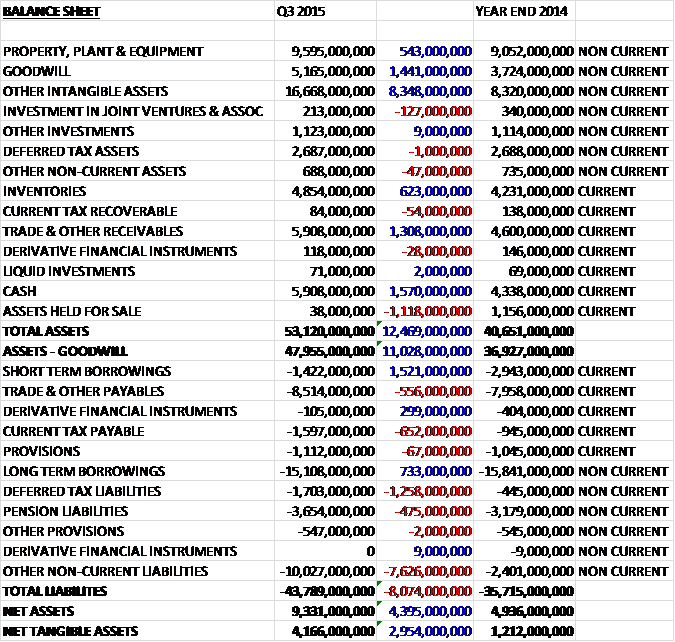

When compared to the end point of last year, total assets increased by £12.469BN driven by an £8.348BN growth in other intangible assets, a £1.441BN increase in goodwill, a £1.57BN growth in cash, a £1.308BN in receivables and a £623M growth in inventories. Total liabilities also increased as a £7.626BN growth in “other” non-current liabilities which relates to the agreement with Novartis and Pfizer for GSK to be required to purchased their holdings of a couple of joint ventures, a £1.258M increase in deferred tax liabilities, a £652M growth in current tax payable and a £556M growth in payables was partially offset by a £1.521BN decline in short-term borrowings and a £733M fall in long-term borrowings.

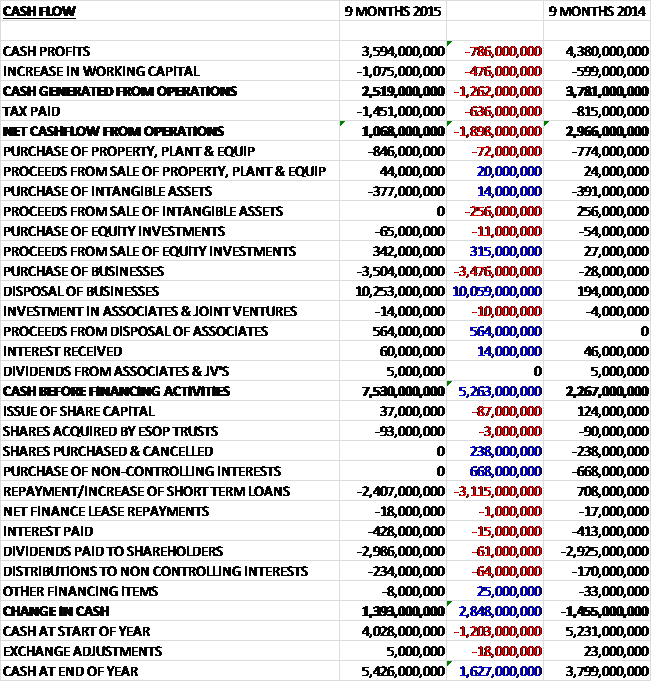

Before movements in working capital, cash profits fell by £786M to £3.594BN and there was also a cash outflow associated with working capital movements, primarily reflecting an increase in receivables from seasonal flu vaccine sales, and tax was some £636M higher than in the first nine months of last year which included a tax payment of £268M on the sale of the oncology business, so that the net cash from operations was £1.068BN, a decline of £1.898BN year on year. The group spent £846M of this cash on property, plant and equipment and £377M on intangible assets so that there was no fee cash but there was a net £6.749BN cash inflow from business disposals and £564M from the sale of part of the shareholding in Aspen so that before financing there was a cash inflow of £7.53BN. The group used £2.407BN to pay back loans, £428M went on bank interest and £3.22BN was spent on dividends to give a cash flow of £1.393BN for the first nine months of the year and a cash level of £5.426BN at the period-end.

Actual profits increased year on year but this was only due to a reduction in non-underlying profits, primarily as a result of a £246M fall in legal charges where last year’s quarter included the fine payable to the Chinese government; and a £350M fall in acquisition costs which included the re-measurement of the liability and the unwinding of the discounting effects on both the contingent consideration for the acquisition of the former Shionogi-ViiV healthcare joint venture and on the consumer healthcare joint venture put option (the ViiV contingent consideration increased in Q3 2014). There was a cash payment of £53M this quarter relating to the ViiV healthcare contingent consideration.

Core operating profit was £1.718BN, 5% lower on constant currency terms than Q3 2014 despite an increase in turnover. The decrease included an impact from the Novartis transaction, reflecting the disposal of GSK’s higher margin oncology business and the acquisition of lower margin products, and also then benefit last year of a £219M credit from a release of reserves following simplification of the group’s entity structure and its trading arrangements. On a pro-forma basis, core operating profit was flat on a turnover increase of 5%. Excluding the impact of the reserves release, the core operating margin increased by 2.1%, benefiting from an improved product mix in the quarter as well as initial contributions from the pharmaceuticals restructuring and Novartis integration programmes.

The cost of sales were broadly flat on a pro-forma basis as the benefits of favourable product mix, driven by strong growth in new products, particularly Tivicay and Triumeq, together with improved supply and pricing in consumer healthcare and accelerated flu vaccines sales in the US, were offset by continued adverse pricing pressure in pharmaceuticals, primarily respiratory, and increased investments in vaccines to improve the reliability and capability of the supply chain. Sales and admin costs increased in the quarter reflecting the comparison with last year’s costs that included the reserve release. Excluding this, costs reduced reflecting savings in global pharmaceuticals, including the benefits of the restructuring programme, and integration benefits in vaccines and consumer healthcare, offset by promotional support for new launches and seasonal activity, particularly in consumer healthcare.

The operating profit in the global pharmaceuticals division was £1.116BN, a decline of £382M year on year. Respiratory sales during the quarter declined by 9% to £1.272BN. Seretide/Advair sales were down 19% to £794M, Flixotide/Flovent sales decreased 4% to £144M and Ventolin sales fell by 3% to £152M. Relvar/Breo Ellipta recorded sales of £64M and Anoro Ellipta, now launched in the US, Europe and Japan, recorded sales of £22M. In the US, respiratory sales declined by 10% with a small decline in volume and a big negative impact of price and mix. This decline included the price and mix impact of new contracts agreed last year in response to competitive pressures where Advair and Breo Ellipta compete. Sales of Advair fell 18%, Flovent sales were down 8% and Ventolin sales fell by 7%.

European respiratory sales were down 13% to £313M with Seretide down 23% reflecting increased competition from generics and the transition of the respiratory portfolio to newer products. Relvar Ellipta, approved in Europe for both COPD and asthma, recorded sales of £20M while Anoro Ellipta, with launches now underway in many countries throughout the region, recorded sales of £5M. Respiratory sales in the ROW region declined by just 2% with emerging markets down 6% partially offset by Japan, up 9% where sales of Relvar Ellipta more than offset the decline in Advair sales. In emerging markets sales of Seretide were down 15% due to additional generic competition and price reductions in a number of reimbursed markets, together with some tender phasing, while Ventolin grew 6%.

Sales in the cardiovascular, metabolic and urology category rose 1% to £225M. The Avodart franchise fell 5% to £176M with 9% growth in the sales of Duodart/Jalyn more than offset by an 11% decline in sales of Avodart. In the US, generic competition in Avodart started in October and generic competition to Jalyn is expected later in Q4 2015. Sales of Prolia increased 50% to £11M. Immuno-inflammation sales grew 3% to £72M. Benlysta turnover in the quarter was £59M, up 22% with Benlysta US sales up 23%.

Sales in other therapy areas grew 1% to £523M. Dermatology sales declined 7% to £94M, adversely affected by supply constraints, which also affected Augmentin sales, down 8% to £116M. Relenza sales more than doubled in the quarter to £15M, partly driven by the timing of US CDC orders. Sales of products for rare diseases declined 7% to £91M, despite including sales of Volibris which were up 3%. Established products turnover fell 13% to £614M with sales in the US down 21% and Lovaza sales down 66%. Europe was down 10% to £115M, with Serevent sales down 18%. ROW was down 11% with lower sales of Zeffix, down 28% driven by China, and Seroxat down 14%. Valtrex sales increased 42% to £33M following the regaining of exclusivity in Canada until October 2015.

The operating profit in the ViiV healthcare division was £466K, an increase of £220M when compared to Q3 last year. HIV sales increased 65% to £622M with the US up 94%, Europe up 54% and ROW up 19% with the growth in all three regions being driven by Triumeq and Tivicay. The ongoing roll-out of both products resulted in sales of £211M for Triumeq and £157M for Tivicay. Epzicom/Kivexa sales declined 9% to £175M but Selzentry sales grew 10% to £33M. There were continued declines in the mature portfolio, mainly driven by generic competition to both Combivir, down 42% to just £7M, and Lexiva, down 19% to £18M.

The operating profit in the vaccines business was £464M, a growth of £136M when compared to Q3 2014. Vaccine sales grew 32% to £1.181BN with the US up 42%, Europe up 31% and ROW up 22%. The business benefited from sales of the newly acquired products, primarily Bexsero and Menveo in Europe and the US. The 13% pro-forma growth was primarily driven by strong Fluarix sales in the US due to improved supply and the accelerated switch to the Quadrivalent formulation, and higher CDC orders primarily for Rotarix, and Synflorix in ROW regions. The growth was partly offset by supply constraints in Hepatitis vaccines and a decline in Infanrix in the US reflecting a return of a competitor to the market.

In the US sales grew 42% and 22% on a pro-forma basis. This was largely attributable to the improved supply and accelerated delivery schedule of Fluarix Quadrivalent, up 59% compared with Q3 last year. A government contract delivered incremental Ixiaro sales while the timing of CDC orders drove Rotarix up 57%, and the Hepatitis vaccines portfolio, up 9%. These factors were partially offset by the comparison to Q3 last year which benefited from an Infanrix CDC replenishment. The newly acquired portfolio added a combined £60M to US sales, driven by the Bexsero launch and the timing of CDC orders for Menveo.

In Europe sales grew 31% and 14% on a pro-forma basis to £308M. This growth primarily reflected increased sales in the Meningitis portfolio. Bexsero growth came from gains in private market channels in several countries including Italy and Portugal, and the UK following its inclusion in the NHS immunisation programme. A strong Menveo performance reflected a tender win in the UK. Growth in Germany was strong with Boostrix, the MMRV portfolio and Infanrix all benefiting from better supply and a competitor supply shortage. Growth in Europe was partly offset by a 9% decline in sales of Hepatitis A vaccines reflecting supply constraints.

In the ROW market, sales grew 22% and 3% on a pro-forma basis to £347M. The pro-forma performance reflected Synflorix growth, up 19%, driven by orders from Africa and Brazil. International pro-forma growth was partly offset by Boostrix, down 48%, due to greater competitive pressures, particularly in Latin America, and lower sales of Hepatitis A vaccines, reflecting supply constraints.

The operating profit in the consumer healthcare division was £210M, an increase of £75M year on year. The business represents the joint venture with Novartis together with the GSK business in India and Nigeria, which are excluded from the joint venture. Turnover grew 55% to £1.576BN, benefiting significantly from sales of the newly-acquired products. On a pro-forma basis, growth was 7% reflecting 5% in volume and 2% in price, reflecting strong growth in the US following the launch of Flonase as well as globally strong growth in Sensodyne and Panadol. Momentum from first half launches continued to drive innovation contribution with sales from product introductions in the last three years representing about 13% of sales in the period.

US sales grew 61% on a reported basis to £360M and 18% on a pro-forma basis, with Flonase contributing just over half of the growth for the quarter. Theraflu recorded strong growth following the launch of a warming syrups range. The quarter also benefited from the improved supply of denture care products and the re-launch of Nicorette lozenge together with the ongoing re-launches of Nicorette Minis and alli, which continued their recovery from supply shortages last year.

Sales in Europe grew 87% to £481M, but just 1% on a pro-forma basis. Sensodyne continued to report strong growth due to new advertising in key markets and the roll-out of Sensodyne True White in the UK, Sensodyne Repair and Protect in Germany and Sensodyne Mouthwash across a number of markets. In Wellness, Voltaren continued to perform strongly, recording the highest ever market shares in Germany, Sweden, Poland and Italy, driven by a new advertising campaign. This was substantially offset by unusually warm weather in Europe which delayed the start of seasonal cold and flu activities.

ROW sales of £735M grew 37% on a reported basis and 6% on a pro-forma basis. India continued to perform well with Horlicks reporting growth of 8% and Sensodyne delivering growth of 41% due to strong marketing campaigns. Oral health sales in Japan grew 15% compared with a comparative period impacted by an increase in sales tax last year, with Sensodyne sustaining its position as the country’s number one toothpaste brand. Wellness sales began to recover as some markets stated to return to growth following the negative impact of reducing channel inventories in the acquired consumer businesses.

Core EPS for the year is expected to decline at a percentage rate in the high teens, primarily due to continued pricing pressure on Seretide in the US and Europe, the dilutive effect of the Novartis transaction and the inherited cost base of the Novartis business. The guidance excludes potential income from the proposed divestment of ofatumumab. In 2016, the group expects to see a significant recovery in core EPS with percentage growth expected to reach double digits on a constant currency basis as the adverse impacts seen this year diminish and the sales and synergy benefits from the Novartis transaction contribute more meaningfully. The board are apparently confident in their outlook for the rest of the year and a return to growth in 2016.

Some of the new pharmaceutical and vaccine products seem to be gaining some traction. Of course the HIV products of Triumeq and Tivicay are leading the way with sales in the quarter of £211M and £157M representing increases of more than 100% and 96% respectively. The next most important is vaccine Menveo was sales of £81M, but this only represented an increase of 26%. The £41M of Bexsero sales, however, represented an increase of more than 100%. The respiratory products of Relvar/Breo Ellipta and Anoro Ellipta both increased sales by more than 100% to £64M and £22M respectively. For some context seretide sales fell 19% to £794M and Avodart sales were down 5% to £176M so Triumeq is already as important as Avodart and is increasing importance at a considerable rate.

During the quarter there were a few advances made in the pipeline, most notable of which was the Japanese approval of Zagallo for alopecia and the data from the phase III study of Shingrix demonstrating 90% efficacy against shingles in people 70 years of age and over.

The group are expecting to complete the divestment of ofatumumab in Q4 2015 or Q1 2016. During the period they completed the disposal of various consumer healthcare products in a number of markets for £145M. They also completed the disposal of two meningitis vaccines in a number of markets for £55M. Both of these disposals were required to meet anti-trust approvals for the Novartis transaction.

The net debt at the end of the period stood at £10.551BN compared to £14.788BN at the same point of last year. There was no change in dividend expectations for the year and the shares are currently still yielding 5.8% and is planned to remain the same up to the end of 2017 which is probably providing a bit of a floor on the share price at present. There is also a special dividend of 20p that is going to be paid early next year which will give a dividend yield of 7.2% for this year only.

On the 4th November it was announced that the group had received approval from the US FDA for its biologics licence application for Nucala (mepolizumab) as an add-on maintenance treatment of patients with severe asthma aged twelve years and older and with an eosinophilic phenotype. It is administered as a 100mg fixed dose injection every four weeks and patients will receive Nucala in addition to their normal medications for severe asthma. This is the first marketing authorisation for the drug anywhere in the world and took about a year to achieve from submission. Applications have been submitted in a number of other countries including the EU and Japan with further submissions expected during 2016.

Overall then this was a bit of a mixed quarter for the group. Profits did increase but this was due to lower legal costs and less acquisition expenses and underlying profits fell due to the lower margin on the acquired Novartis products. Net assets did improve over the past nine months but operating cash flow was down with no free cash being generated. The problem remains the respiratory portfolio and Seretide in particular. Seretide remains by far the most important drug but sales are down due to pricing pressures in the US and generic competition in Europe and the new respiratory drugs are still some way off making a contribution close to Seretide.

Elsewhere, generic competition for Avodart is expected to start in the US in Q4 which will put this stalwart under pressure but the real saviour at the moment is ViiV healthcare and the new drugs of Triumeq and Tivicay which are growing fast and starting to make a real meaningful contribution. It is just a shame that the group doesn’t own 100% of these products! The vaccines business is also doing well with the contribution from the former Novartis products along with some organic growth. Additionally, consumer healthcare is also making an improved contribution to profits due to the launch of Flonase in the US and a strong performance from Sensodyne. With a dividend yield of 5.8% and the strengthening contribution from the ViiV healthcare drugs, I think GSK is starting to look rather interesting again.

On the 2nd December it was announced that the European Commission had granted authorisation for Nucala as an add-on treatment for severe refractory eosinophilic asthma in adult patients. As a result it is now approved for use in the 31 countries covered by the EMA. This follows the US approval in November and regulatory applications are ongoing in a number of other countries including Japan.

On the 16th December the group announced that it had received positive top line results from the phase III programme investigating sirukumab, a human anti-interleukin monoclonal antibody for the treatment of patients with moderately to severely active rheumatoid arthritis in development as part of a collaboration with Janssen Biologics. There were no unexpected safety findings and long term safety and efficacy data are currently being collected in ongoing extensions of the trials. Regulatory applications for the drug are anticipated in 2016.

On the 18th December the group announced that ViiV Healthcare had reached two separate agreements with Bristol Myers Squibb to acquire its late stage HIV R&D assets and to acquire their portfolio of preclinical and discovery stage HIV research assets. Under the terms, ViiV will acquire fostemsavir, an attachment inhibitor currently in phase III development for heavily treatment experienced patients which is expected to be filed for regulatory approval with the FDA in 2018. The second late stage asset is a maturation inhibitor currently in phase II development for both treatment naïve and experienced patients and a back-up inhibitor candidate is also included in the purchase.

Assets in preclinical and discovery phases of development include a novel biologic with a triple mechanism of action, a further maturation inhibitor, an allosteric integrase inhibitor and a capsid inhibitor. A number of Bristol Myers Squibb drug discovery employees will also be offered the opportunity to transfer to ViiV Healthcare. These potential therapies have novel modes of action and would offer significant new treatment options to patients with HIV.

The late stage asset purchase comprises an upfront payment of $317M followed by development and first commercial sales milestones of up to $518M and tiered royalties on sales. The purchase of the preclinical and discovery stage research assets comprises an upfront payment of $33M followed by development and first commercial sales milestones of up to $587M with further consideration contingent on future sales performance. These transactions are expected to be completed in H1 2016.

On the 21st December the group announced the completion of its transaction to divest rights to ofatumumab for auto-immune indications to Novartis following regulatory approval. The consideration payable by Novartis may reach up to $1.034BN and comprises $300M paid at closing; $200M payable subject to the start of a phase III study in relapsing remitting MS; and further contingent payments of up to $534M payable on the achievement of certain other development milestones. Novartis will also pay royalties of up to 12% on any future sales of the drug in auto-immune indications.

It looks as though this sale is paying for most of the purchase of the HIV assets but only time will tell as to whether this is a good deal I guess.

On the 23rd December the group announced the appointment of Dr. Jesse Goodman as a non-executive director. Dr. Goodman is currently professor of medicine at Georgetown University and previously served in senior leadership positions in the US FDA, including most recently as the FDA’s chief scientist. This to me looks like a very useful addition to the board.