International Greetings have now released their final results for the year ended 2018.

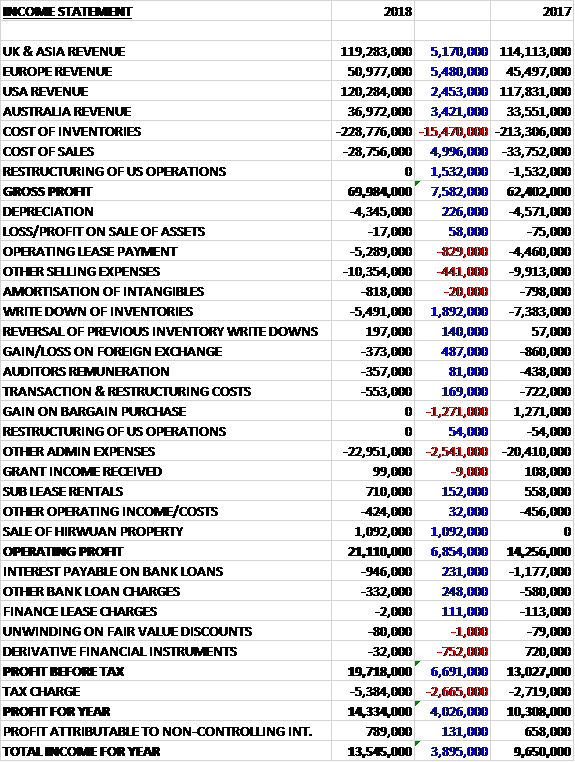

Revenues increased when compared to last year due to a £5.2M growth in UK and Asian revenue, a £5.5M increase in European revenue, a £3.4M growth in Australian revenue and a £2.5M increase in US revenue. Cost of inventories also increased but there were no US restructuring costs which were £1.5M last time so the gross profit was £7.6M higher. Operating lease payments increased by £829K and other selling expenses were up £441K. There was also no gains on bargain purchase, which brought in £1.3M last time. Offsetting this was a £1.9M reduction in inventory write-downs and a £487K improvement in the forex loss. Other admin expenses increased by £2.5M and after the group made £1.1M on the sale of the Hirwuan property, the operating profit was £6.9M higher. There was a £752K detrimental swing on derivative financial instruments and tax charges increased by £2.7M to give a profit for the year of £13.5M, a growth of £3.9M year on year.

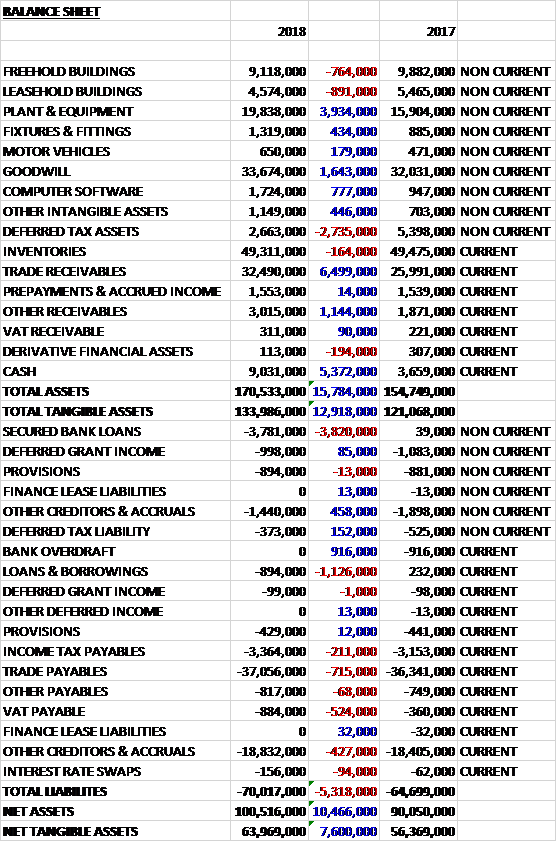

When compared to the end point of last year, total assets increased by £15.8M driven by a £6.5M increase in trade receivables, a £5.4M growth in cash, a £3.9M increase in plant and equipment, a £1.6M growth in goodwill and a £1.1M increase in other receivables, partially offset by a £2.7M decline in deferred tax assets as historical tax losses are used up. Total liabilities also increased during the year due to a £4.9M increase in borrowings. The end result was a net tangible asset level of £64M, a growth of £7.6M year on year.

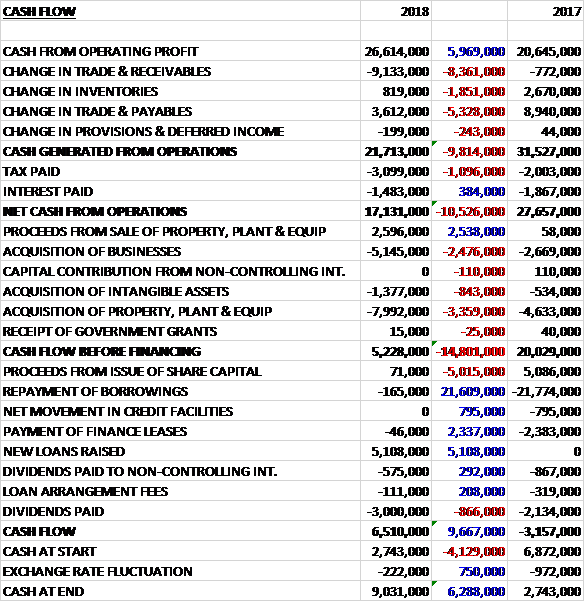

Before movements in working capital, cash profits increased by £6M to £26.6M. There was a cash outflow from working capital, however, and after tax payments increased by £1.1M the net cash from operations was £17.1M, a decline of £10.5M year on year. The group spent £8M on fixed assets, £1.4M on intangible assets and £5.1M on acquisitions but took £2.6M from the sale of assets to give a free cash flow of £5.2M. Of this, £3M went on normal dividends and £575K on dividends to non-controlling interests. After they took out £5.1M of new loans the cash flow was £6.5M and the cash level at the year-end was £9M.

The underlying result for the UK and Asia was £7.9M, a growth of £420K year on year. Last year the group decided to reorganise their three UK business under one overall leadership team. This year they began to see the tangible benefits of increased cohesiveness with a return to profit growth in the region and encouraging momentum across many areas of the UK business. They saw an excellent performance in their gift wrap and paper bag manufacturing operation in Wales and card, bag and cracker production facility in China.

An initiative to develop new income streams in adjacent categories and resulted in the UK manufacturing paper bags for the not for resale market, with a focus on the supply of higher end fashion and beauty brands. With production starting in September 2017 they are already providing retail brands with a significant volume of bags with orders in place which will grow the business further still in 2019.

The underlying result for Europe was £6.7M, an increase of £1.6M when compared to last year. This growth was supported by sales of bespoke gift products which have been especially strong with photo frames and photo based gift accessories achieving record volumes. Their efficiency has been further enhanced through their latest investment in a new printing press which started production in the Netherlands in March.

The underlying result for the US was £9.3M, a growth of £2.1M when compared to 2017. The year featured strong growth in their Creative Play product sales under the recently launched Anker Play Products brand which includes play themed educational, art and crafty and construction ranges for mass and value retailers. They plan to further develop sales of the brand within the Americas and throughout the global customer base.

Sales of dated products such as calendars grew and alongside the challenges of integrating a new business, the synergy opportunities that were identified during the acquisition of Lang have continued to be delivered with further areas of improvement. New initiatives include the investment in a new IT platform to enable their future growth trajectory to be efficiently delivered and supported by user friendly systems and enhanced commercial and operational capability.

The underlying result for Australia was £2.9M, an increase of £1.2M year on year. Having won a three year contract for the supply of greetings cards to Australia’s largest discount retailer in 2017 they saw the benefits of this flow through during the year combined with economies of scale. This has been further enhanced by the acquisition of Biscay in January with operational and commercial integration on track to complete during 2019.

The group remains focused on further improving margins in future years by driving operational efficiencies through sourcing and manufacturing as well as balancing the mix of products toward higher margin categories and channels such as increased sales of design group branded products. They anticipate the trend of overheads rising at a slower rate than sales growth to continue.

Over the year the group spent £9.4M on capex. Some £3-4M represented maintenance spend with the balance being spent on increasing capacity, improving efficiencies and developing new product offerings. Significant capital projects completed included the acquisition of a second printing press in the Netherlands which came on line at the year-end meaning the production efficiencies they will gain over the older press it replaces will benefit the coming year; the introduction of a new bag machine in the UK factory to provide not for resale branded bags for retails, which is now full operational and delivering profit in this new revenue stream; and an ERP system programme in the US which will support the delivery of operational efficiencies and future growth there.

During the year there were transaction costs of £553K relating to the acquisition of Biscay and some remaining costs from the Lang acquisition. There was also a benefit of £1.1M relating to the exceptional gain on the sale of the Hirwaun property in Wales and was inclusive of any restructuring costs related to the sale.

In January the group acquired Biscay Greetings, a greetings card and paper products business based in Australia. The acquisition was satisfied by a cash consideration of £5.1M and generated goodwill of 1.7M. In the quarter the business contributed £1.3M of revenue.

Going forward, with a strong order book in place and a positive start to the year the board are expecting further growth in 2019.

At the year-end there was a net cash position of £4.4M compared to £3M at the end of last year. At the current share price the shares are trading on a PE ratio of 26 which falls to 20 on next year’s consensus forecast. After a 33% increase in the dividends the shares are yielding 1.2% which increases to 1.5% on next year’s forecast.

On the 28th August the group announced the acquisition of Impact Innovations, a supplier of gift packaging and seasonal décor products in the US, for a total consideration of £56.5M. This is going to be paid for with a placing of up to £50M with institutional investors of 9,804,000 new shares. Last year, Impact recorded an underlying EBITDA of $15M and the directors believe the acquisition will create the world’s largest consumer gift packaging business, deliver significant earnings accretion over the next three years, deliver annual synergies in excess of $5M by year three; and enable expansion into the adjacent seasonal décor product category.

On the 16th October the group released a trading update covering the first half of the year. They have a positive performance in the period with reported overall revenue and margin, including the recent acquisition of Impact, significantly up on last year with growth across all regions. The integration of Impact is already underway with synergies on track to be delivered on time or earlier.

The new printing press in the gift wrap manufacturing operation in the Netherlands is now fully operational and supporting record production levels and improved efficiencies; the Biscay acquisition is now fully integrated with targeted synergies already beginning to deliver enhanced performance; the new IT system in the US has gone live on time and is now being run in parallel with the existing IT platform to ensure the processes are running smoothly; and the new revenue initiative in the factory in Wales to manufacture premium paper bags continues to deliver increased volumes with a strong pipeline of new customers to come.

The group is on track to achieve year on year profit growth in the full year and the EPS performance is in line with management expectations, delivering strong growth.

Overall then this seems to have been a decent year for the group with profits up and net assets increasing. The operating cash flow did decline but this was due to working capital movements and the free cash covered the dividends. All regions have performed well, particularly outside the UK, and this seems to have continued into this year. The acquisition is interesting but it is disappointing to see an equity raise, particularly one where the general punter can’t participate. The good performance comes at a price though and the shares are definitely not cheap with a forward PE of 20 and yield of 1.5%. Not sure whether to keep hold of these or not.