James Latham has now released its final results for the year ended 2016.

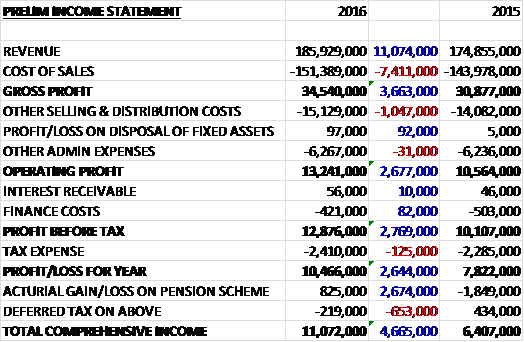

Revenues increased by £11.1M when compared to last year and cost of sales increased by £7.4M to give a gross profit £3.7M above that of 2015. Other selling and distribution costs were up £1M which meant that the operating profit grew by £2.7M. A modest decline in finance costs, mainly relating to interest on the pension scheme deficit, was offset by a growth in tax expenses to give a profit for the year of £10.5M, a growth of £2.6M year on year.

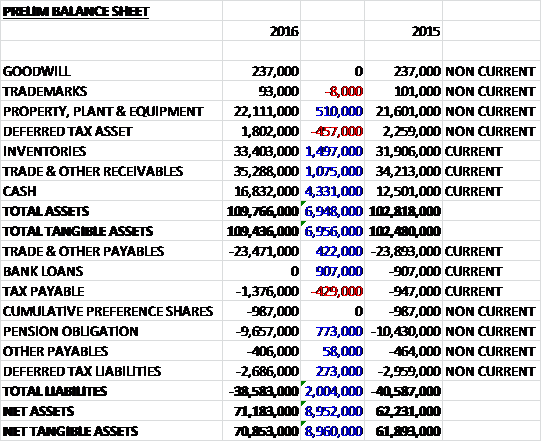

When compared to the end point of last year, total assets increased by £6.9M driven by a £4.3M growth in cash, a £1.5M increase in inventories and a £1.1M growth in receivables. Total liabilities declined during the year as a £907K fall in bank loans and a £773K decrease in pension obligations due to increased corporate bond yields used to calculate the liabilities was partially offset by a £429K growth in current tax payables. The end result is a net tangible asset level of £70.9M, a growth of £9M year on year.

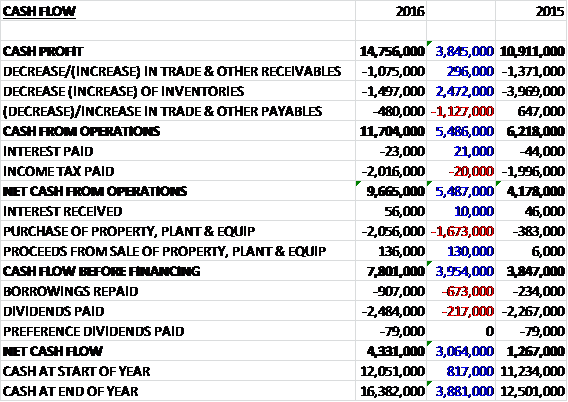

Before movements in working capital, cash profits increased by £3.8M to £14.8M. There was a cash outflow from working capital, although this was less than last year and after tax and interest was broadly consistent, the net cash from operations was £9.7M, a growth of £5.5M year on year. The group spent £2.1M on capex to give a free cash flow of £7.8M. Of this, £2.5M was paid on dividends and £907K was used to pay back borrowings which gave a cash flow of £4.3M and a cash level at the year-end of £16.4M.

Revenue continued to grow this year due to increased volumes both in ex-warehouse and direct business but year on year growth slowed in H2. Both panels and timber grew revenues throughout the year. The gross margin, before warehouse costs, increased by 1.4% due to the higher share taken by the specialist products and margins remained tight on commodity products.

Timber and panel prices fell slightly during the year despite weakness of sterling in the second half of the year. Focus panel products including melamine panels and door blanks continues to show good growth. The certified sustainable hardwood and WoodEx, the brand of engineered timber for the joinery sector, showed good growth. Overheads were higher than last year due to the extra volumes and longer warehouse hours introduced to meet customer demands.

The plans to upgrade the two older sites at Yate and Wigston have progressed with site purchase and build contracts approved, subject to planning, for a new site in Yate which should be completed by the end of the year, and negotiations proceeding for the relocation of the Wigston site.

So far this year, like for like revenues are 4% higher for April and May, both in panels and timber, and the gross margin is also higher. Whilst this is a steady start to the year there are some signs that this growth is slowing and the fluctuating value of sterling and the uncertain outlook for business activity caused by the Brexit vote make the immediate future difficult to predict. The board continue to see encouraging growth in the newer decorative products they introduced, however.

At the current share price the shares trade on a PE ratio of 11.5 but this increases to 13 on next year’s consensus forecast. After an increase in the dividend, the shares are yielding 2.3% which increases to 2.6% on next year’s prediction.

There is not much detail given in this update but overall then this has been a very strong year for the group. Profits are up, net assets increased and the operating cash flow grew with plenty of free cash being generated. All this with a forward PE of 13 and dividend yield of 2.6% suggests something might be wrong and growth has been slowing with the Brexit vote increasing uncertainty and the weakening sterling must not be good for the group. For now I feel it wise to wait for more certainty regarding what effect Brexit will have on Latham.

Panel Product sales were 5.8% higher than last year at £132.1M with volumes up 2.3%. The group’s strategy continues to be to target specific markets where decorative surfaces are required. Their extensive range of real wood veneered and melamine products, laminates, Hi-Macs natural acrylic stone and flexible panels have all shown sales growth. During the year they added Xylocleaf, a high quality embossed melamine panel, and Kydex, a thermoformable plastic to their range. These products have enabled them to develop sales into new customers and markets and they will continue to invest in a wider range of melamines and laminates.

Sales of hardwood and softwood plywood have come under pressure during the year, but the strategy continues to be to supply certified products. A campaign to raise the awareness of the group’s plywood range began in January. Birch plywood sales have remained strong despite the weak currency in Russia.

In Spite of aggressive pricing by competitors, the group have seen marginal growth in sales of MDF with more positive increases in Tricoya Extreme Durable Fibreboard. The next generation of added value and higher performance Smartply OSB entered the market during the year and early indications show a real interest from the customer base. An exclusive agreement to distribute a range of fire retardant materials from the group’s Iberian supplier has helped to increase sales and margins in this area.

During the year extensive testing has been carried out on the high quality Moralt fire, thermal and acoustic door blanks, leading to specifications being won and higher sales volumes. In March the group signed a three year agreement with the Business Design Centre in London for a suite where they will have a dedicated team and showroom aimed at the group’s larger audience of architects, designers and specifiers.

The Advanced Technical Panels team produced a good increase in turnover and margin this year. Buffalo Board continues to be specified and the addition of Kydex on an exclusive distributor basis proved to be very beneficial with strong sales into new and existing customers.

Timber sales were 7.7% higher at £53.9M with volumes up 6.7%. The timber strategy remains to target the joinery, kitchen and shopfitting sectors, all of which have provided sales and volume growth. The group re-focused their sales efforts on the traditional business namely American (mostly walnut and oak), African and European hardwoods. They have been developing their relationships with key suppliers in these areas, and concentrating their sales efforts on premium grades. Volume growth in North American and European timbers has been encouraging, but achieving sales and margin growth in African timbers remains challenging.

The group has secured some high end specification contracts for both Lifecycle and Profi, the premium range of wood plastic composite decking. They believe the market for composite decking is one that could bring further growth. Their success has been more with contractors than builders merchants so far but they expect sales from both sectors to grow in the future.

Accoya Modified Wood sales have been steady this year, but there have been some high profile specifications for their Latham Accoya Clad. They are also introducing other species into the cladding range, in a market where the group haven’t previously been strong in.

The largest growth area has been WoodEx, the FSC certified brand of engineered hardwood and softwood, where they have continued to expand the range and sizes that are available to meet their customer needs. Their decision to focus on working with a small number of suppliers and promote premium products is proving successful. The Engineered Grandis 690+ has been tested and approved for use in FD60 door frames which will provide the group opportunities in the door market.

LDT have made a very useful contribution to group profits despite the extreme competition. The group have made good progress in developing overseas markets in Europe and Asia and expect to see continued sales growth there. As part of their ongoing development, LDT will look to increase their product offering to the importer and merchant sectors, whilst maintaining their strict environmental policy.

The group will continue to look to develop new markets, including Ireland and other export markets. They will continue to invest in their depots, with the relocation of the Yate and Wigston depots expected to be substantially complete during the course of the next year. Further investment in racking systems will be undertaken at Hemel Hampstead and Purfleet depots. They will also consider acquisitions where opportunities arise, to enhance their product range or geographical coverage.

The cash level is being held to finance the relocations of Yate and Wigston. There have been more planning delays for Yate than originally anticipated but this relocation should be completed by March 2017. The board do not foresee and planning issues with the Wigston relocation and this may be substantially completed by June 2017. It is anticipated that each site will cost over £7M with sales proceeds for the existing two sites being received the year after.

As expected the levels of capital expenditure returned to normal levels during the year. The £2M invested in fixed assets included £825K in new and replacement lorries where they have increased their fleet by seven to 69 vehicles. £695K was invested in warehousing lifting equipment and £200K in warehouse racking. They also undertook a major project to replace their complete IT infrastructure to move to state of the art servers, hosted away from the depots, and improving back-up and disaster recovery systems which took place with no disruption to business activities.

The group are somewhat susceptible to exchange rate changes but apparently they are hedged against any volatility that has arisen around the Brexit vote.

Overall than, this doesn’t change my view but adds a bit more detail to the story. All parts of the business seem to be performing well, in particular the more value added products. This also shows that the relocations are going to be a short-term burden on cash flow and this potential disruption does add some risk. This is a high quality company, performing well but I remain somewhat concerned about any Brexit-related issues (although the group claims to be well insulated against currency changes).

On the 24th August the group released an update covering the first four months of the year. Revenue in the period is 3% higher year on year, largely the result of product mix but also higher volumes traded, with more orders delivered from the warehouses. Margins are higher than for the same period last year, although slightly down on Q4 2016. Overall they are trading in line with full year market expectations.

The trading environment remains competitive, and activity shows signs of slowing for both timber and panels, although the group continues to see growth in the newer product lines that they have taken on and bad debts continue at a low level.

Since the year-end, they have completed the purchase of a new site in Yate at a cost of £5.2M. Fitting out is expected to cost an additional £1.2M and they expect to relocate into this site by June 2017. They are also in negotiations for a site for the relocation of the Wigston warehouse. They have increased their capacity to meet growing demand for their specialist panels with further investment in racking at Hemel Hempstead.

The outlook remains uncertain but the wide spread of customers and strong balance sheet means that they are well placed to take advantage of opportunities. Overall, this is a decent enough update but the slowdown in timber and panels is a bit of a concern.

On the 6th March the group released a trading update covering the full year results. Revenue for the year is expected to be broadly in line with market expectations and pre-tax profit is likely to be higher than expected. Building work is continuing as planned and to budget at the new depot in Yate and the move to the site is expected during August. In addition, detailed plans have been agreed for the relocation of the Wigston business to a new site and the company is currently awaiting planning approval. The board also announced that Peter Latham has decided to retire as Chairman and that Nick Latham will take over. This all seems good.