Murgitroyd has now released its final results for the year ended 2015.

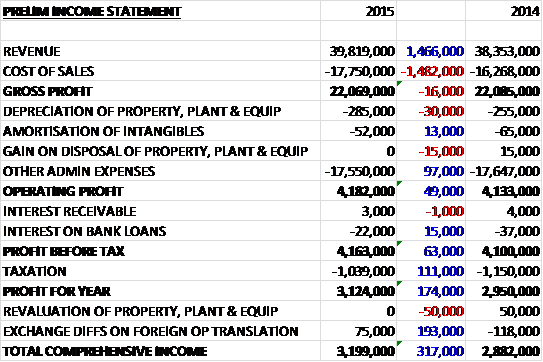

Revenues increased by £1.5M when compared to last year but a similar increase in cost of sales meant that gross profit was broadly flat, down by just £16K. Depreciation was slightly higher but other admin expenses fell to give an operating profit some £49K ahead of last year. This was further improved by a small reduction in interest and a £111K fall in tax which gave a profit for the year of £3.1M, an increase of £174K when compared to last year.

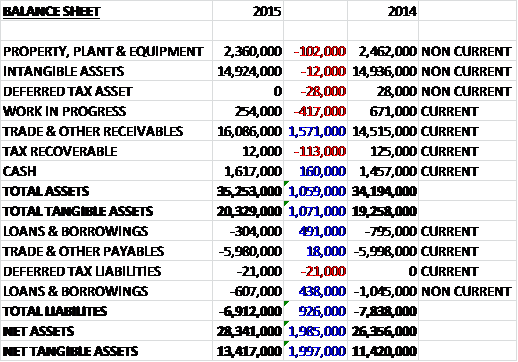

When compared to the end point of last year total assets increased by £1.1M driven by a £1.6M growth in receivables, partially offset by a £417K fall in work in progress. Liabilities fell during the year due to a £929K decline in loans and borrowings. The end result is a £2M increase in net tangible assets at £13.4M.

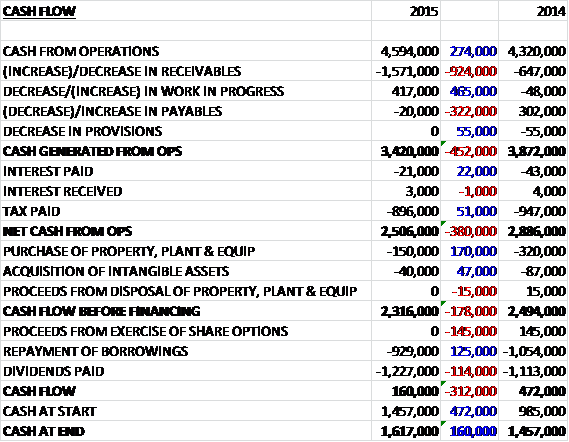

Before movements in working capital, cash profits increased by £274K to £4.6M before a larger increase in receivables, partially offset by a fall in work in progress and less interest and tax paid meant that the net cash inflow from operations was £2.5M, a decline of £380K when compared to 2014. The group then only spent £150K on fixed tangible assets and £40K on intangible assets to give a free cash flow of £2.3M, of which £1.2M was paid out in dividends and £929K was used to pay back loans. The group had a cash inflow for the year of £160K and a cash level at the year-end of £1.6M which is all very comfortable.

The markets in which the group operate showed steady growth in the year with an increase in Community Trade Mark applications, up 4.4% and a stable demand for Registered Community Design applications. The most recent stats report an annual increase of 3% in European Patent applications to 273,000, which is an all-time high. The composition of these filings shows applications from the US up 6.7%, Japanese applications falling by 3.8% and EU applications remaining unchanged. The group continues to monitor developments concerning the introduction of the new European Unitary Patent, which is still expected to be ratified by sufficient member states of the EU and enter force during 2017. Despite the buoyant markets, however, price pressures remain and cost control remains a priority for the group.

Revenue growth has been driven organically by the ongoing investment in business development, principally in the US where revenues increased by 20% to £15.7M and the country now accounts for about 40% of total sales. This growth was partially offset by a further contraction of £900K in revenues from the longstanding UK client base. The gross margin declined slightly from 57.6% last year to 55.4% in 2015 due to the ongoing changes in the client and sales mix as well as the continuing price pressure in the market for professional IP advisory services. Despite this, operating profits increased by 1.2% due to a strong focus on cost controls.

As well as a reduction in overall headcount, the number of qualified attorneys required and employed by the group continues to fall reflecting the transfer of a number of revenue generating areas from attorneys to paralegals, specialist formalities staff and patent and TM admins. The group will continue to recruit and train these non-attorney staff members whilst at the same time restructuring how it delivers services to clients to generate greater efficiencies. This restructuring is on course and remains a key component of the group’s strategy of growing earnings.

During the year, Edward Murgitroyd took over day to day leadership of the management teams and was appointed CEO of the operating subsidiaries in October. Dr. Chris Masters and John Reid have been appointed as non-executive directors and in August, the group appointed Gordon Stark as COO. Due to these new appointments, the executive chairman, Ian Murgitroyd intends to move from an executive position to a non-executive role going forward.

Over the next year the group are looking to drive growth in the US while also increasing their focus on Europe with the aim of reversing the recent contraction of revenues in this market as economic activity increases. Trading since the year-end has been in line with management expectations and the board apparently look forward to the future with confidence.

At the current share price the shares trade on a PE ratio of 15.4 reducing to 14.7 on N+1 Singer’s forecast for next year. After an 11% increase in the total dividend for the year, the shares yield 2.8% increasing to 3% on next year’s forecast. There is a net cash position of £710K at the end of the year compared to a net debt position of £380K at this point of last year.

Overall then, this was a solid set of results. Profits increases modestly year on year and net assets were also up. Operating cash flow did fall but this was entirely due to an increase in receivables and underlying cash profits grew to give a comfortable free cash flow. Although the market seems to be growing, the problem is the pressure on price and it looks like the group is looking to cut costs to drive growth rather than rely on an upturn any time soon. The US business seems to be performing well at the expense of the UK division so hopefully this is something that they can focus on for next year. The forward P/E of 14.7 and dividend yield of 3% seem about right for this safe stock with net cash. Safe but rather unexciting in my view and I am not rushing to own any shares for the time being.

The chart doesn’t look all that exciting at the moment either…