N. Brown is a clothing chain that focuses on plus sizes. As well as the sale of products, the group also makes money from the rendering of services which includes interest, admin charges and arrangement fees. Interest income is accrued on a time basis, by reference to the principle outstanding and the applicable effective interest rate which is the rate that exactly discounts estimated future cash receipts through the expected life of the financial assets to that asset’s net carrying amount. The average credit period given to customers for the sale of goods is 258 days. Interest is charged at 44.9% on the outstanding balance and generally receivables over 150 days past due are written off in full. JD Williams is an online department store for the 50+ female with other brands including Simply Be and Jacamo. N Brown has now released its final results for the year ended 2015.

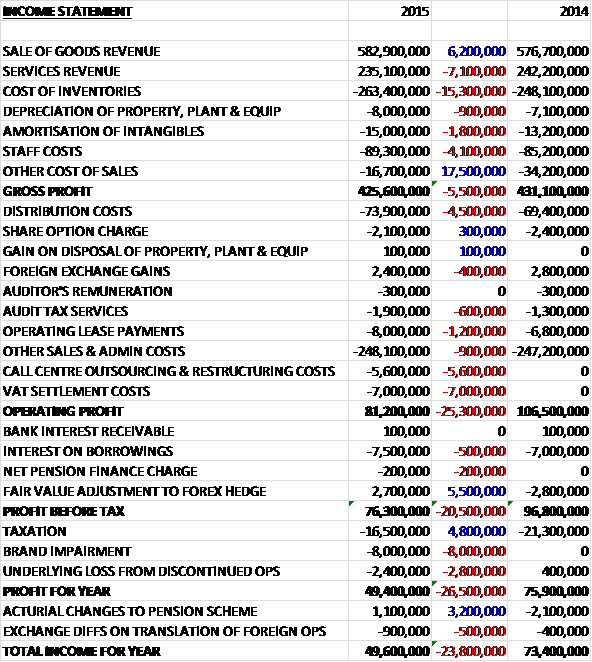

Overall revenues were down when compared to last year as a £6.2M increase in the sale of goods was more than offset by a £7.1M fall in services revenue. Cost of inventories increased by £15.3M which was offset by a decline in other cost of sales so that the gross profit was some £5.5M down. Distribution costs grew by £4.5M as did operating leases and sales and admin costs but we also see some one-off costs creeping here too with a £5.6M charge related to restructuring, including the outsourcing of the call centre to Serco, along with a £7M charge relating to the VAT settlement with HM Customs which drove the operating profit down by £25.3M at £81.2M. The group then benefited from a £5.5M positive swing in the fair value adjustment of the forex hedge and a lower tax payment but the brand impairment and the underlying loss from the discontinued operation meant that the profit for the year came in at £49.4M, a decline of £26.5M year on year.

When compared to the end point of last year, total assets increased by £42.7M driven by a £33M growth in the value of software, a £9.5M increase in trade receivables, a £6.1M growth in land and buildings and a £4.9M increase in inventories, partially offset by an £8M fall in the value of brands and a £4.9M decline in cash. Total liabilities also increased during the year as a £28M increase in bank loans, an £8.8M growth in trade payables and a £4.7M increase in accruals and deferred income was partially offset by a £4.9M fall in current tax liabilities and a £2.8M decline in social security and other taxes. The end result is a net tangible asset level of £398.3M, a decline of £13.7M year on year.

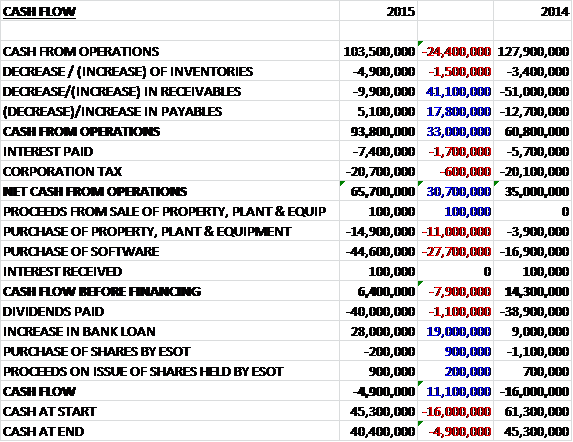

Before movements in working capital, cash profits fell by £24.4M to £103.5M. There was an outflow from working capital, but this was much less than the huge increase in receivables that occurred last year and after higher interest payments, the net cash from operations was £65.7M, an increase of £30.7M year on year. The group spent £44.6M on software and £14.9M on fixed tangible assets relating to stores and the warehouse in equal measure to give a free cash flow of £6.4M. This was nowhere near enough to pay the £40M in dividends so the group increased the bank loan by £28M to give a cash outflow of £4.9M for the year and a cash level of £40.4M at the year-end.

Step-changing the way the business operates and presents itself to market proved more disruptive than anticipated in some key areas and this, combined with a very challenging Autumn trading period across the sector, led to their performance falling below initial expectations. The largest brand, JD Williams, was entirely relaunched during the year which was well received by customers and the spring saw a step-up in the product offering and brand awareness.

Jacamo, having enjoyed revenue growth of 20% last year, saw sales rise by 11% during this year. The introduction of two new labels in the portfolio has helped attract more customers to the brand. Both Label J and Black Label have built on the success of the Flintoff range. The group are also driving brand awareness with TV advertising, used for the first time. The homewares category saw sales increase by 7% year on year; there has also been a decent international performance, albeit with deliberately constrained growth as they bedded in a third party credit offering. US demand was up 13% for the year.

Interestingly the CEO has identified a number of weaknesses at the group including merchandising, the value for money of some of their products, the digital marketing capability, low brand awareness and an underinvested systems infrastructure. Apparently they have made progress in all of these areas but will continue to focus on them going forward.

Over the past year the group have made improvements to their product quality. Also, from a price perspective they decided to make a number of investments to improve their competitive positioning. They have rebalanced their pricing architecture with clearer definition between the three price points of the products. They introduced a small number of key value lines and at the top end of the pricing structure they have improved the ranging of their premium product with occasionwear being a good example. For spring they moved JD Williams to “All sizes one price” in line with the other brands. This followed positive results from a number of trials but the changes led to a percentage margin reduction, although cash margin increased after three to six months.

In financial services, whilst revenue declined by 2.9% year on year, this was driven by a number of policy changes made and the gross profit contribution increased year on year with credit arrears at their lowest level on record. The focus in the division is on maintaining the credit customer base, growing the number of cash customers and modernising the offer. The latter target is enabled by the systems transformation project which will enable the group to charge variable APRs, offer promotional interest free periods and allow them to make credit decisions at a product level.

The group have recently started taking cash customers and their introduction has not resulted in a decline in the credit customers who roll over a balance but are incremental or at the expense of credit customers who immediately paid off their balance, not incurring interest charges. It has also been noted that cash customers have a 6% lower returns rate than either group of credit customers.

A comprehensive review of the systems transformation projects has been undertaken and as a result the number of systems releases has been streamlined and the project length reduced. The project is primarily focused on customer facing improvements and in association with the significant systems change, they are also running an organisational change programme. The benefits include cost reductions, increased demand and improved margin and some of these benefits will be reinvested back into the business. The global multi-channel transformation is expected to save £24M at a cost of £41M; the credit transformation project is expected to save £12M at a cost of £9M; and the planning transformation project is expected to save £9M at a cost of £15M so in total the savings are expected to be £45M at a total cost of £65M. These benefits are expected to start to ramp up from the second half of 2017 with the full impact from 2020.

In the US, sales grew by 13% and the operating loss reduced considerably from £4.7M to £2.5M. Revenue growth was somewhat constrained by the decision to dial-down the recruitment activity as they bedded in their third-party credit provider. This credit offer has performed strongly and has significantly improved customer loyalty, with credit customers seeing a 250% uplift in second order rates versus cash customers. The systems transformation programme includes the launch of a new international web platform and until this is live they will remain in cautious expansion mode in the US, with a focus on improving customer loyalty, building brand awareness and minimising operating losses, which sounds sensible to me.

Sales from the Simply Be and Jacamo stores were up 64% to £13M but the operating loss increased slightly, from £1.6M to £1.8M over a period of significant store openings. There are now fifteen stores, including five stores opened during the year with the new Exeter store being the best performing to date. The long term strategy is to open 25, covering 85% of the population. They have continued to see a positive “halo” effect from the store portfolio and they are also important in terms of building brand awareness. This coming year will see an efficiency review focusing on logistics as the board believe these operations can be improved.

The group are in discussions with HMRC in relation to the VAT consequences of the allocation of marketing costs between the retail and the credit businesses. At this stage it is not possible to determine when or how the matter will be resolved but in the VAT creditor there is an asset of £16.7M that has arisen as a result of cash payments made under protective assessments raised by HMRC which the board expect to recover in full.

Following a review of the business and its future profit potential, the board decided to close the Gray and Osbourn catalogue business. The process is ongoing and will continue into the next year but the business made an underlying loss of £2.4M during the period with an £8M amortisation of the brand, whose value was reduced to zero. Other exceptional costs included £5.6M spent on strategy costs, which include the outsourcing of the call centre to Serco, along with group re-organisation costs. The group also incurred £7M of exceptional costs for VAT. This relates to a potential settlement with HMRC in respect of VAT recovery on bad debts written off over a number of years. The board expect to settle this matter in the coming year.

There were a number of board changes during the year. Lesley Jones joined the board as non-executive director. She has over 35 years of marketing and risk management experience. In January they it was announced that Dean Moore would be stepping down to pursue other opportunities. He had been CFO for eleven years and was placed by Craig Lovelance who was previously CFO of BMI Healthcare. It is notable that the directors are very well paid here, perhaps excessively so, and it is also interesting to see that 18% of votes were voted against the remuneration report at the last AGM which is quite a lot.

The group has a bank loan of £250M secured over some receivables whilst there is also an unsecured bank loan of £37M drawn down under various medium term bank revolving credit facilities of which £120M is committed until March 2016. At the year-end they have available £83M undrawn committed borrowing facilities. If interest rated had increased by 0.5% the profit before tax would have decreased by £1.4M so this is a potential risk for the group. The group does operate a defined benefit pension scheme which was closed to new members back in 2002. Although the deficit is currently only £3.3Mm the present value of defined obligations is £120.8M.

The scale and pace of change required to modernise the business put a great deal of strain on the performance in a difficult year for the clothing sector. Some important foundations for profit recovery and long term growth were laid and the board is confident in the outlook for the business.

At the current share price the shares trade on a PE ratio of 17.6 falling to 15.1 on next year’s consensus forecast. The shares yield 3.8% which is expected to remain the same next year. At the year-end the group has a net debt position of £246.6M compared to £213.7M at the end of last year. In addition there are outstanding operating leases of £32.1M which are increasing, presumably as the number of stores increase.

Overall then this has been a rather difficult year for the group. Profits were down year on year not helped by the ongoing costs relating to the dispute with HMRC and the restructuring expenses. Net tangible assets also fell and although operating cash flow improved, this was only because there was a much smaller increase in receivables than last year and cash profits were down. There was some free cash but this was nowhere near enough to cover the dividends.

Operationally the group was affected by the restructuring and the poor autumn for the clothes market due to the warm weather. Despite this, sales at Jacamo and homewares improved and the US business reduced losses. The stores still made a loss, but this was apparently due to the new openings so this should bode well for the future. Despite the poor performance this year, I do think this is a decent business and the comparatives for next year seem good but I will hold of for now.