N Brown has now released its final results for the year ended 2016.

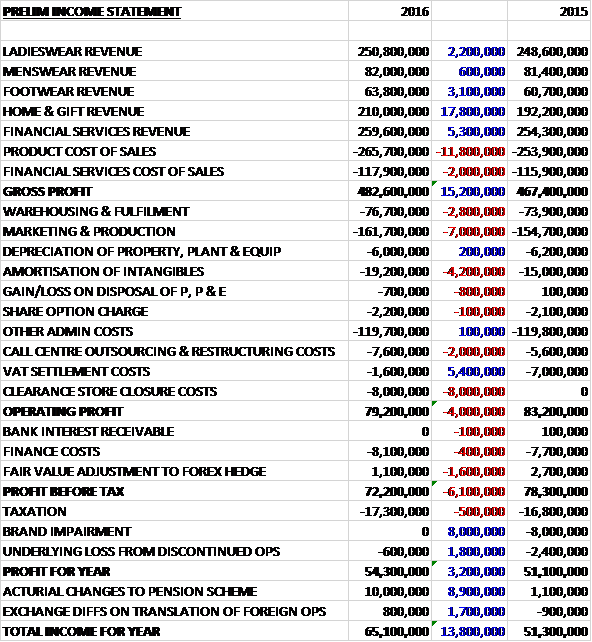

Revenues increased when compared to last year due to a £17.8M growth in home and gift revenue, a £5.3M increase in financial services revenue, a £3.1M growth in footwear revenue and a £2.2M increase in ladieswear revenue. Cost of sales also increased but the gross profit was some £15.2M above that of 2015. Warehousing and fulfilment costs were up £2.8M due to higher volumes, marketing and production costs increased by £7M as the creative production function was outsourced, resulting in some costs shifting from payroll to marketing, and amortisation was some £4.2M higher due to more investment in intangibles. We also see a £2M increase in restructuring costs and an £8M charge relating to clearance store closures, but this was somewhat offset by a £5.4M fall in VAT settlement costs which meant that the operating profit fell by £4M. We then see a £1.6M reduction in the changes in the forex hedge value but there was no brand impairment which accounted for £8M last time and there was a £1.8M reduction in the underlying loss from discontinued operations which all meant that the profit for the year came in at £54.3M, a growth of £3.2M year on year.

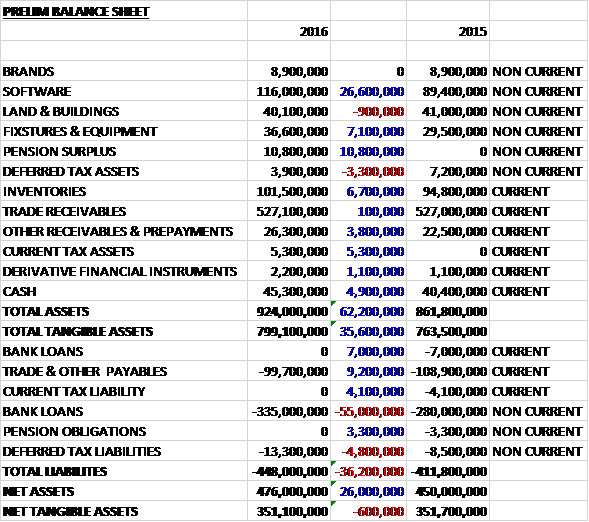

When compared to the end point of last year, total assets increased by £62.2M driven by a £26.6M growth in software, a £10.8M increase in pension assets, a £7.1M growth in fixtures and equipment, a £6.7M increase in inventories, a £5.3M hike in current tax assets and a £4.9M growth in cash, partially offset by a £3.3M fall in deferred tax assets. Total liabilities also increased during the year as a £48M increase in the bank loan and a £4.8M growth in deferred tax liabilities were partially offset by a £9.2M fall in payables and a £4.1M decrease in current tax liabilities. The end result was a net tangible asset level of £351.1M, broadly flat year on year with a decline of just £600K.

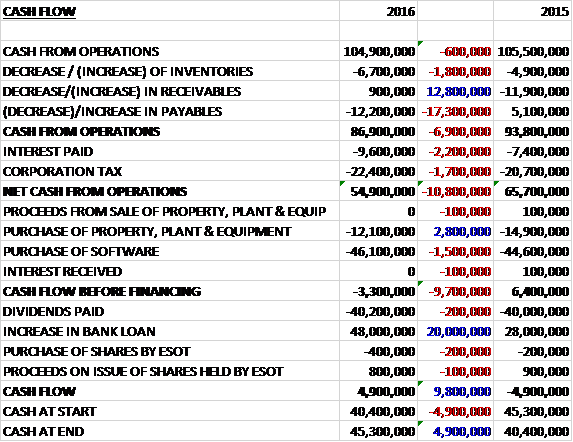

Before movements in working capital, cash profits fell by £600K to £104.9M. There was a large cash outflow from working capital as inventories grew driven by the timing of the new season intake, and payables fell which meant that after the interest costs increased by £2.2M and tax payments were up £1.7M, the net cash from operations came in at £54.9M, a decline of £10.8M year on year. The group spent £46.1M on software relating to the Fir for the Future programme and £12.1M on tangible fixed assets related to the warehouse extension, which gave a cash outflow of £3.3M before financing. They then increased the loan so they could pay out £40.2M in dividends which doesn’t seem that sensible to me. In all, there was a cash flow of £4.9M for the year to give a cash level of £45.3M at the year-end.

Overall the performance in 2016 was in line with expectations with a strong 11% profit growth in H2 with a good Christmas trading period. They saw a flat market share in ladieswear but within this they gained market share in younger fashion, driven by Simple Be and saw a small decline in the older age groups as a result of the underperformance of their traditional segment. There was a 20 basis point increase in menswear market share which was driven by Jacamo. In Q4, product revenue declined by 3.5% but financial services revenue was up 8.1% which meant that overall continuing revenue increased by just 0.2%, the weakest quarter during the year when compared to 2015, although it remained relatively unchanged when compared to Q3.

One area of focus has been expanding the offering of third-party brands and the ranges with Sprinkle of Glitter and Coast performed particularly strongly. In the last six months they have also launched collections from Scarlet & Jo, Studio 8 by Phase 8, Eden Row and Luke. In March they launched their first homewares range with Lorraine Kelly, building on the success of her womenswear and footwear ranges. The range consists of interior accessories across two trend collections and includes bed linens, lighting, soft furnishings and home accessories.

The group saw a reduction in returns with the returns rate improving by 120 basis points to 27.4% which was driven by the relative outperformance of homewares and menswear, improvements to the product quality and fit, and the increase in cash customers. Inventory clearance across the industry is moving online and as a result of this dynamic, the group closed their clearance stores in the first half. They are developing new online clearance tools and will be taking the opportunity to leverage these capabilities and reduce the aged inventory position over the course of 2017.

Online revenue was up 15% and online active customer numbers increased by 13%. Online penetration stood at 65%, a 6 percentage point increase but the online conversion rate was flat at 5.8%, although this was significantly above the industry average.

Financial services performed well during the year and continues to be an important enabler of the business. Revenue was up 2.1% to £259.6M but credit arrears over 28 days stood at 10.9%, an increase from the 10.3% recorded last year, driven by new customer recruitment. The provision rate improved from 16.1% to 15.6% with the improving trend a direct result of the work done over the past two years to tighten up the credit policies and help customers in financial difficulties. In 2017 the board expect both the provision rate and the arrears rate to reflect increased levels of customer recruitment and increase slightly.

Currently half of new customers opt to open a credit account, with about half being cash customers. Whilst less profitable, cash customers generate attractive returns, and are important in terms of driving growth and enabling the group to gain economies of scale. Once their new financial services offering is live they will aim to convert some of the cash customers to account customers. Over Christmas the group ran a small trial on a few of their brands offering 0% interest to new customers. The initial results of this trial are positive, but they need to assess the behaviour of customers who took up the offer over the course of the current season before they will be able to fully judge the result.

The Credit release of Fit for the Future goes live from autumn 2016 with the main brands moving onto the new credit platform in early calendar 2017. The new platform will allow the group to charge variable APRs for the first time as well as offer promotional interest free periods and other new credit products. In common with the wider industry, they are now regulated by the FCA having historically been regulated by the OFT and the FCA application is progressing in line with expectations.

The JD Williams brand continues to perform well, as the improvements the group are making to their products, their PR activity and their digital marketing campaigns continue to yield results. This season they significantly extended the menswear range within the brand and the performance exceeded expectations. The loyalty scheme launched in May 2015 continues to drive encouraging results in both frequency of spend and customer retention. Revenue from the brand was £151.2M, up 4.7% year on year with online penetration up 6ppts to 51% and online penetration of new customers up 13ppts to 65%.

Simply Be revenue was up 15.6% year on year to £103.9M The online penetration of the brand is 89% and 97% of new customer orders. The group improved their digital marketing expertise and social engagement, championing size inclusivity and body confidence. The new SS16 campaign has been well received and the board believe the brand offers a good global growth opportunity.

Jacamo revenue was up 14.6% to £62.8M. Online penetrations stands at 90% and 97% of new customer orders. They group have made significant product improvements, focused on broadening the brand appeal, the styling of the product range and the fit out of smaller sizes which resulted in strong sales and a reduction in the returns rate for these sizes.

The traditional titles such as Ambrose Wilson, House of Bath and Premier Man, have been disappointing with revenue down 5.5%. The board have taken a number of actions to improve performance including establishing a dedicated marketing team, changing their approach to promotions and giving a renewed focus on ensuring the product offering is what the customers actually want. The low online penetration of this segment means that it is likely to take until the autumn before performance is improved but they are confident that these actions will yield results.

The systems transformation project is progressing well. During the half the group launched the Simply Be Euro website and Powercurve, the foundation of the credit released and both launches were made on time. The benefits of the project are expected to ramp up from 2018 onwards and some of these benefits will be invested back into the business. The timetable for the project remains unchanged. This August they plan to start the roll out of the new web platform and new financial services platform, initially to the US, and then to a number of the smaller UK brands in September. The main brands will move onto the new systems in early 2017, after peak Christmas trading.

In May the roll out of the first phase of the planning transformation will be completed, giving the group improved tools for assortment and range planning. This will allow them greater visibility, control and consistency. The second phase of the planning release, which will give them item-level forecasting tools, improving markdown efficiency will go live in early 2017.

The warehouse extension at the main warehouse facility in Shaw is now complete and in the process of coming on stream. The project was completed on time and budget and the new facility has doubled throughput and importantly materially improving the next day availability of products.

US revenue was up 29%, aided by favourable forex movements and the business made a dollar profit in H2 with the operating loss for the year falling form £2.5M last year to £1M. The significant improvement year on year was driven by continued marketing efficiency, a small amount of financial income as a result of the relationship with Alliance Data, an improvement in promotional efficiency and a small charge for delivery.

In March the JD Williams brand was launched in the US and whilst early days, the initial performance has been encouraging. The new international web platform goes live in the US in August. This will give the group much improved personalisation tools and a more agile site from an operations perspective. Until this platform is live, they will remain in cautious expansion mode in the country with a focus on further improving customer loyalty, building brand awareness and increasing profitability.

The Ireland business delivered a decent performance this year with revenue growth of 4% on constant currency terms. The revenue growth was driven by new customers who are responding to their improved product offering. The business suffered due to the decline in the euro, however, and in sterling terms revenues were down 7% to £13.4M.

The stores remain a small part of the group overall but sales from the store estate were up 18% to £27M. The operating loss was £1M versus £800K last year and there remains more to do in terms of improving the efficiency of the estate. They group have 14 dual fascia Simply Be and Jacamo stores and the long term strategy is to have 25 in total, covering 85% of the UK population.

As with most years, the group have recorded a number of “exceptional costs”. Strategy costs of £7.6M relate to reorganisation costs and the outsourcing of IT maintenance whilst last year the £5.6M charge related to the outsourcing of the call centre. The VAT costs of £1.6M are legal and professional fees related to ongoing disputes with HMRC. Last year these charges of £7M related to a potential settlement with HMRC in respect of VAT recovery on bad debts written off over a number of years. Within the year-end VAT debtor is an asset of £21.7M which has arisen as a result of cash payments made under protective assessments raised by HMRC and based on legal opinion, the group believe that they will recover this amount in full and are engaged in a legal process to do so. In the first half of the year the group closed their retail clearance stores and the exceptional costs of £8M relate to stock write downs, onerous lease provisions and other closure costs. In all, these “exceptional” costs were £17.2M this year compared to £12.6M last year.

There are a number of risks facing the group. A key risk the delivery of their transformation project, Fit for the Future. This is due to be delivered in 2017 and the scale of the changes means that the success of the business in meeting its expectations for profitability is linked to the success of the project. Business continuity plans are in place and the group has further migrated IT systems and data security risk within the business through outsourcing IT services to a specialist IT provider. The Chairman has suggested that a programme on this scale will likely bring some “unexpected bumps in the road” which sounds ominous.

Also, they continue to review their compliance with the CCA and submitted an application to the FCA for full authorisation in September. Whilst the board consider that they are compliant, there is a risk that the eventual outcome may differ.

Following the appointment of KPMG as auditor, the group determined that it was necessary to make a change in the technical interpretation of IAS39. The revised interpretation relates to the judgement over whether a credit loss has been incurred when interest or other charges are temporarily waived, even for customers who ultimately repay their full capital balance. For customers who find themselves in financial difficulties, the group may offer revised payment terms but for these customers the group’s financial statements now reflect an impairment provision for the foregone interest income upfront and they recognise interest or other income over time on the impaired balances. Previously the group was focused on the capital element of receivables and did not consider loss of interest as an impairment loss. Last year this had the effect of increasing profits by £1.7M but reducing net assets by £46.6M due to the fall in receivables.

Going forward in 2017 the board are expecting product margin to fall by 50bps to 150bps due to forex headwinds, the clearance of aged inventory and tactical price activity to drive market share growth in a challenging market. Group operating costs are expected to grow by between 2% and 4%, capex is expected to be around £40M and exceptional costs of £2M are expected due to the ongoing tax disputes with HMRC.

Trading since the year-end has been subdued with sales lower year on year. The industry backdrop has been more challenging since January and the group have also adjusted their marketing approach this year, shifting from large TV campaigns to a more phased approach with increased investment in digital channels. This new approach delivers a better return on investment when viewed across the season as a whole so the board are expecting to see performance strengthen over the half. Forex rates also represent a significant challenge year on year with the strengthening US dollar against the pound giving a £3M profit headwind in 2017 with every 0.05 rate move in the exchange rate representing a £1M impact on profits, but overall the board remain confident of making further progress this year.

At the year-end the net debt position was £289.7M compared to £246.6M at the end of last year. At the current share price the shares are trading on a PE ratio of 13.9 which reduces to 11.2 on next year’s consensus forecast which doesn’t seem too taxing. After the final dividend was kept the same, the shares are yielding 5.3% which is also expected to be the yield next year too.

Overall then this has been a bit of a sluggish year for the group. Profits were up but this was only due to losses and impairment last year from discontinued operations and continuing profits fell modestly. Net tangible assets were broadly flat and operating cash flow declined with no free cash being generated after the investments in IT and the warehouse. Operationally, Jacamo and Simply Be are performing very well but this is offset by slower growth elsewhere and a decline in sales from the traditional brands. The US business is nearly at the breakeven point, though, and I must say I like the cautious approach to this market.

There are a number of issues facing the group, however. The fact that many of the products are purchased in US dollars mean that recent forex movements are unhelpful and the very expensive Fit for the Future programme could cause some teething issues this year. Indeed there are several warnings in this update stating that projects this size often have issues so I am fully expecting something to come out of the woodwork. When this is combined with subdued trading so far this year which is behind last year, despite the forward PE of 11.2 and yield of 5.3% looking good value, I am steering clear for now having sold out at a small loss.

On the 22nd April it was announced that CEO Angela Spindler acquired 18,000 shares at a cost of £49K which gives her a total of 93,295 shares.

On the 16th June the group released a trading update covering Q1. Group revenues were down 0.2% year on year with a 3.4% growth in financial services more than offset by a 1.6% fall in product revenues. Overall trading was in line with board expectations and the guidance for the year remains unchanged. The growth in financial services was driven by the increase in new credit customers. JD Williams, Simply Be and Jacamo continue to outperform the wider group and revenue from the traditional segment has continued to decline.

Simply Be and Jacamo revenues were both up year on year, driven by ongoing product improvements and the new season campaigns which are resonating well with the target customer bases with both brands seeing a significant increase in their active customer files. The JD Williams brand saw double digit growth but revenues for JD Williams as a whole were slightly down due to a weak performance from the Fifty Plus title.

Product revenues in Fashion World Figleaves, High and Mighty and Marisota were marginally lower year on year with Fashion World being the strongest performer. The traditional segment saw a mid-single digit decline in product revenues, in line with the performance reported at the final results stage. Actions have been taken to rectify this but although early signs are encouraging, it will take until H2 for them to positively impact performance.

During the period the group ran targeted promotions in order to drive revenue which resulted in a low single digit decline in average selling price, which was more than offset by an increase in average units per basket. The USA business saw Q1 revenue up 25% year on year with an increase of 17% at constant currency. The group remain in cautious expansion mode in the country, ahead of the new international web platform going live in August.

They had a good performance in the financial services division with the increase in revenues being driven by interest payments from new credit customers. The board continue to expect both their arrears rate and provision rate to increase slightly during the year, however. The full FCA authorisation application is progressing in line with expectations.

The Fit 4 the Future transformation project remains on track and to budget. They have now completed the roll out of the first stage of their new merchandising system as planned and are now in testing phase for the new web platform and credit systems with the next significant milestone being the launch of the new US website in August.

So, it doesn’t appear that much has changed for the group and I am staying away for now.

On the 21st September the group announced that JD Williams had been granted full FCA authorisation. The group’s new US web platform is scheduled to go live within the next few days, slightly later than planned. Learnings from this launch will be incorporated into the plan for the roll out of the new UK web platform and financial services system. This will result in a change to the previously communicated timetable with further details being released at the interim results.

The group has identified an error in relation to its previous calculation of financial services customer complaint redress. A detailed review is being undertaken but they currently anticipate that this will result in an exceptional cash cost of between £5M and £8M.