N Brown has now released its interim results for the year ending 2016.

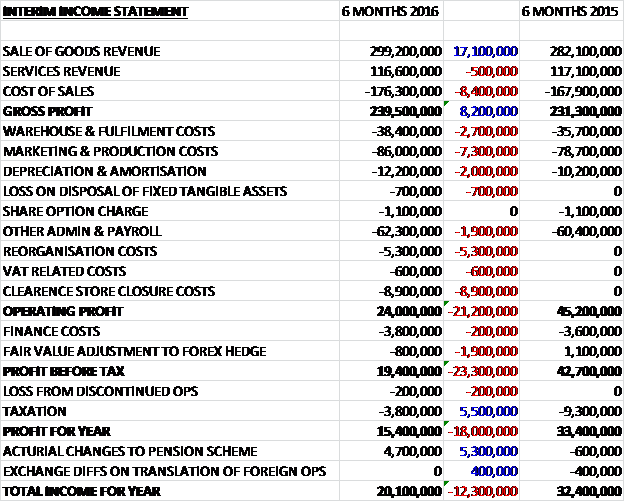

The revenue attributable to the sale of goods increased by £17.1M and the services revenue remained broadly flat year on year. Cost of sales also increased to give a gross profit £8.2M above that of the first half of last year. Warehouse and fulfilment costs increased by £2.7M, admin costs grew by £1.9M and depreciation & amortisation increased by £2M but the big increase was the £7.3M hike in marketing and production costs due to a step up in recruitment for Simply Be and Jacamo together with the timing of some TV campaign spend, which meant that underlying operating profit fell year on year. In addition to this there were some one-off costs including a £5.3M reorganisation charge and an £8.9M cost relating to the closure of the clearance store which meant that operating profits nearly halved to £24M. There was also an adverse movement in the forex hedging instrument but tax was a lower which meant that the profit for the half year was £15.4M, a decline of £18M year on year.

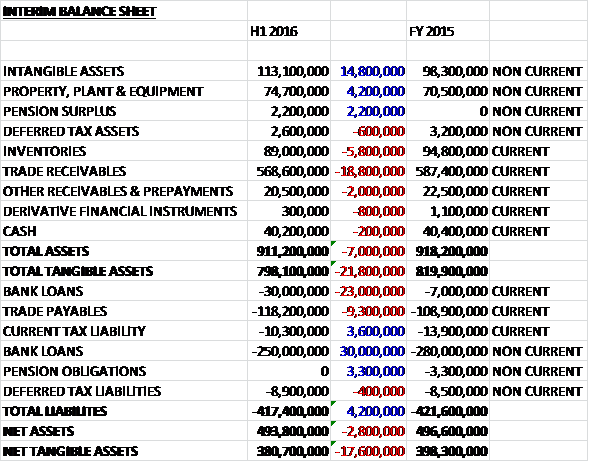

When compared to the end point of last year, total assets fell by £7M to £911.2M driven by an £18.8M decline in trade receivables, a £5.8M decrease in inventories and a £2M fall in other receivables and prepayments, partially offset by a £14.8M increase in intangible assets, a £4.2M growth in property, plant and equipment and a £2.2M pension surplus. Total liabilities also declined during the period as a £7M fall in the bank loan, a £3.6M decline in the current tax liability and a the eradication of the £3.3M pension deficit was partially offset by a £9.3M increase in trade payables. The end result is a net tangible asset level of £380.7M, a decline of £17.6M over the past six months.

Before movements in working capital, cash profits fell by £18.6M to £38M. As with the first half of last year, there was a big cash inflow from working capital with a particularly large fall in receivables and after a £5.5M reduction in the corporation tax payment, the net cash from operations was £62.4M, a decline of just £400K year on year. The group spent £8.5M of this on fixed tangible assets mainly relating to warehousing and £23.1M on intangible assets, mostly relating to software developments to give a free cash flow of £30.8M. Some £24.2M was spent on dividends and the rest was used to make a dent in that huge bank loan so that there was a £200K cash outflow for the period and a £40.2M cash level at the end of the half.

The group is adjusting their retail business model and the way they operate, transforming from direct mail-led to digital first.

The gross profit in the product division was £172.9M, an increase of £5.8M year on year. JD Williams continued to improve but the turnaround of the largest brand will take time and during the period JW Williams product revenue was £103.1M, flat year on year. The brand represents a group of seven historic titles that have been migrated into JD Williams over the past year but Fifty Plus and Ambrose Wilson still need to be migrated which should take place in 2016. The core brand actually increased sales with the overall flat performance due to a decline in Ambrose Wilson sales. In addition, new customers were up 21%, the online order penetration of first orders increased by 21% to 74%, overall online penetration of JD Williams was over 50% for the first time, and the market share of retail online traffic, although still low at 0.4%, was up 22%.

Simply Be product revenue was up 21% to £50.2M with an improving trend in Q2 compared to Q1. The online penetration of the brand is now 89%. During the period, the group further strengthened their digital marketing capabilities and stepped up their social engagement, with campaigns such as #catwalkcontender, a search, working with Cosmo magazine and Milk money agency, for a real customer to front their Christmas campaign. They have also launched new ranges for Autumn Winter 2015, including Simply Be Unique, targeted at the most fashion conscious consumers, a capsule Coast range exclusively in sizes 20-26, a range with their new brand ambassador Jameela Jamil, and a range with plus-size blogger Sprinkle of Glitter.

Jacamo product revenue was also up 21% to £30.4M, again with an improving trend in Q2. Online penetration stands at 98%. The strong performance was driven by improved product ranges. Going forward, they continue to focus on the brand positioning and style credentials. Again, they significantly increased their social media engagement, the highlight being the #Hakarena campaign, which has been viewed by over 2.4M people online and trended number one on twitter. The specialist brands performed strongly, with revenues up nearly 16% to £38.4M driven by a continued good performance from House of Bath but support brands saw revenue fall by 2.8% to £77.1M.

Overall ladieswear saw growth of 2.4% to £134.6M against a challenging market backdrop. Within this, the Q2 growth rate was several percentage points higher than in Q1. Menswear revenue declined by 2.9% to £40.6M although younger menswear outperformed, driven by Jacamo. There was a good performance in Footwear, with revenues up 11.9% to £33.2M driven by continued product improvements. Home and Gift revenue was up 14.8% to £90.8M. This was driven by improvements made to the product offering, helped by a favourable market backdrop and by encouraging customers to increase their spend with the group by also purchasing homewares in addition to the core fashion offering.

The gross profit in the financial services division was £66.6M, a growth of £2.4M when compared to the first half of last year with revenues that fell 0.4% with a 1.9% decline in Q1 and a 1% improvement in Q2. The modernisation of the business is enabled by the credit release of their new systems transformation project which gives the group the tools to continue to refine their credit decision making, charge variable APRs, offer promotional interest free periods and new credit products in 2016. Credit arrears over 28 days stood at 10% compared to 11.7% in the first half of lf last year which was due to policy changes in prior periods and improved fraud detection. As they go into H2, the board expect the rate to increase slightly due to seasonal timing factors (rates are high in the busier Christmas period) and the continued step-up in new customers.

For the first time in three years there was an increase in new credit customer recruits, up 15%. It is believed that this was driven by the improved product proposition. Going forward it is expected that the recently introduced 0% interest offer over the Christmas trading period and, longer term, the ability to offer customers a far more personal credit proposition, to both generate further new credit customers. It is still relatively early days since the introduction of cash customers and they seem to be either incremental or at an expense of credit customers who immediately paid off their balance, not incurring interest charges. Currently about half of new customers open a credit account.

Sales from the Simply Be and Jacamo stores were up 91% to £9.4M and 6% on a like for like basis. The operating loss was £900K against £600K last year due to the headwind of seven new stores opening during the period with the profitability of like for like stores increasing by 12%. They now have 15 stores with the long term strategy to ultimately have 25.

Before exceptional items, there was a 14% decline in operating profit due to the timing of some marketing spent for the Autumn Winter campaigns which occurred in H1 instead of H2, the increased operating costs from seven new Simply Be and Jacamo stores year on year, and increased depreciation and amortisation spend due to the investments in their systems.

Revenue derived from international markers amounted to £15M, an increase of £1M with an operating loss of £400K compared to £1.2M in the first half of last year. The performance in the US is improving with revenues up 35% to £6.2M and an operating loss that fell from £1.7M to £900K. During the period the group carried out their first PR activity in the country and as part of this focus, they sponsored a special plus-size episode of America’s Next Top Model which was watched by over 1.4M people and drove a 100% increase in traffic to the US website.

The group are pleased with the performance of their third-party credit provider. This is marketed to customers as a credit facility together with a points-based loyalty programme. Over two thirds of new customers now elect to join this scheme which is important for customer loyalty, with credit customers having a second order rate three times that of a cash customer. The systems transformation programme includes the launch of a new international web platform. Until this goes live in mid-2016, they will remain in cautious expansion mode in the US with a focus on further improving customer loyalty, building brand awareness and minimising operating losses which all sounds sensible to me.

The board are also pleased with the performance of the Irish business which saw positive revenue growth in constant currency terms for the first time in several years, driven by the product improvements they have made. Irish revenues were £6.4M, down 3.9% in sterling terms but up 5.9% on a constant currency basis.

During the year the board carried out an efficiency review of their store estate which resulted in two sets of outcomes. The group are improving staff structures and store rotas to better match demand patterns and increase efficiency, changing store delivery frequencies, tailoring this to individual store requirements; and moving to “just in time” logistics processing of inventory for stores. The other outcome was the closure of the 18 clearance stores which took place in August after the review concluded that disposing of unwanted stock through outlet stores was inefficient and outdated. The excess inventory is now sold through online channels at a cost saving of £3M per annum against the clearance store route.

There were a number of non-underlying items during the period. VAT costs relate to a potential settlement with HMRC in respect of VAT recovery on bad debts written off over a number of years. It is anticipated that this matter will be settled in the second half of the year. The £600K charge is legal costs associated with disputes with HMRC on this and other issues. During the period they closed their retail clearance stores, in line with the strategy to become digital first with the exceptional costs of £8.9M relating to stock write-downs, onerous lease provisions and other related closure costs. The exceptional costs in the second half are expected to be considerably lower in H2, with guidance of between £2M and £3M.

The overhaul of the merchandising function is now largely complete, they have made strong progress with the relative pricing position of their products and they have significantly invested in and improved their digital marketing capabilities, the brand awareness continued to increase and they are half way through their systems infrastructure project.

The global multi-channel transformation involves a new core website transaction engine, fixing legacy issues which significantly slowed the speed to market. This new system will allow them to trade with far more agility going forwards. They will also move to a full cloud-hosted technology, have more global marketplace functionality and much improved personalisation capabilities. Credit transformation modernises the credit proposition and allows the group to operate in a far more flexible, customer relevant way. They will be able to charge variable APRs and will have the ability to make lending decisions tailored to individual customers and based on individual products.

Planning transformation significantly improves the systems used by the product teams, providing more enhanced data for merchandising decisions which will, in time, improve the supply chain efficiency.

In the first half the group implemented a new finance system which was delivered on time and to budget. The second half of the year will see the first go-live releases of Fit 4 the Future. The credit transformation went live as the report went to press and the Simply Be euro website goes live later in the second half of the year.

The group currently have a market share of 4.3% in the plus-size ladieswear market and 1.3% in the larger size menswear market. They have ranked third in the UK retail sector for customer service in the recent Institute of Customer Services survey, behind only Amazon and John Lewis. The group have invested in an in-house design function for the first time which is significantly improving their fashion credential, ensuring they present their customers with on-trend collections in a brand appropriate way. To date, this design function has only had input into the womenswear ranges with Autumn Winter 2015 being the first season to benefit. This will be expanded into menswear and home in the coming year and a half. In addition, this season the group will also launch a range with Coast in larger sizes.

The group returns rate significantly improved to 27.8% which was driven by product mix, with homeware outperforming; an increase in cash customers who have significantly lower returns rate; and the benefits from the improvements that have been made in the products such as size consistency.

The group continue to see strong online metrics, with demand up 17% and active customer numbers up 15%. Online penetration stood at 63% during the period, a significant increase to the 58% in the first half of last year. Mobile services now account for 64% of online traffic, an increase of 12% driven by improvements in the mobile offering. The company has a loyal group of customers who are unlikely to transition online to the same extent as the overall population, so it is important that they continue to be considered in the transition to a digital led offering. The conversion rate of 5.7% was slightly lower due to the continued shift to mobile devices which people tend to use for browsing primarily. In fact, the conversion rate increased for each device individually.

During the period the group completed their refinancing process at improved rates. The borrowing facilities, expiring in March 2016, were previously financed through a £250M securitisation facility and two £50M bilateral revolving credit facilities. As a result of the refinancing process, they increased the securitisation facility to £280M and extended it for a further five years. They also replaced the two revolving credit facilities with a £125M facility plus a £50M accordion feature.

The year is expected to be significantly H2 weighted and the second half has started well, with a decent performance in September in line with expectations which underpins board confidence for the year as a whole with the new Autumn Winter campaigns being well received. For the full year the group is guiding for a full year product gross margin from 25bps down to 50 bps up; full year financial services gross margin between 300bps to 200bps down; full year operating costs up 3% to 5%; net interest between £8M to £10M; capex of between £58M to £60M and H2 exceptional costs of £2M to £3M.

After the interim dividend remains the same, the shares yield 3.8% which expected to remain the same for the year as a whole. The net debt position at the period-end was £239.8M compared to £205.2M at the same point of last year.

Overall then this seems to have been another difficult period for the group. Profits declined year on year due to increased recruitment for the stores and the timing of some marketing spend, net assets fell and operating cash flow decreased, although there was still a decent amount of free cash. In the product division, the growth in sales seems to be driven by Simply Be and Jacamo with some of the other brands doing less well. Financial services profits were up in the period as fewer customers were in arrears and the group developed a more flexible product offering.

The physical stores are still loss making due to the new openings but stores that have been open for the year seem to be profitable. The international business was also loss making but these losses are declining, mainly as a result of lower losses in the US. One-off costs are expected to be much lower in the second half and trading is expected to be second-half weighted with a decent September, although I am not sure what effect the mild October will have had on trading. With a dividend yield of 3.8% and a forward PE ratio of 15.1 these shares are not bad value but there is also a hefty net debt position here to consider so I will probably leave this for a while.

On the 22nd December the group announced that director Angela Spindler purchased 23,782 shares at a cost of £69K. This was her first share purchase.

On the 14th January the group announced that non-executive director Simon Patterson is resigning in order to take up another role outside the company.

On the 21st January the group released a Q3 trading update where they state they are on track to meet full year expectations. Group turnover increased by 4.1% in the quarter with product turnover up 4.3% and financial services turnover increasing by 3.7%, compared to 5.8%, 7.9% and 1% respectively in Q2.

After the well-documented difficult start to the season for the sector, the group delivered good results over the cyber weekend and the weeks that followed, driven by an improved product offering which continues to gain traction with customers, together with new digital marketing initiatives. Simply Be and Jacamo showed strong growth and there was also double digit growth in the JD Williams brand.

The JD Williams group of titles saw marginally positive product revenue growth but there remains a divergence in performance between the core JD Williams brand, which has undergone modernisation, and the traditional brands Ambrose Wilson and Fifty Plus. The double digit growth seen in the core JD Williams brand, driven by improved product offerings, strong PR activity and the Autumn Winter digital marketing campaigns, was offset by single digit declines in the other two brands. The group are focusing on stabilising the performance of these brands, including a refinement of their marketing programme and clearer articulation of the product offering for these customers.

Simply Be achieved low double digit revenue growth and the new Autumn ranges were well received by customers. Jacamo also saw double digit growth, driven by the continued success of own-label, together with digital content that is resonating well with target customers. At the category level, ladieswear saw modest growth, a solid result against the challenging market backdrop; menswear recorded mid-single digit revenue growth, driven by Jacamo; but homeware was the best performing category, up high single digit figures driven by furniture, home textiles and beauty.

Online sales were up 13% and both order frequency and units per basket both recorded positive growth whilst the average selling price was flat. Conversion and abandonment rates improved further, both overall and across each device type. Simply Be USA performed well with a 28% growth in turnover, aided by the strong dollar with constant currency revenue up 20%. The group are in cautious expansion mode in the US, ahead of the new international web platform going live in mid-2016.

Whilst stores remain a small part of the group overall, their performance was disappointing with sales flat on a like for like basis. In line with the wider retail sector, footfall was weaker, and this was the primary cause of the muted sales performance, with conversion in store up year on year.

There was revenue growth of 3.7% in financial services and gross margin benefited from the continued improvement in the quality of the credit book. The trend of an increase in new credit recruits who are rolling a balance has continued.

The Fit for the Future project saw to important milestones during the period: the launches of the Simply Be Euro website and Powercurve, the foundation of the credit release and early results on both launches are encouraging. Having reviewed the launch of the first stage of the new web platform, management have identified additional opportunities to improve the customer experience through implementation, and have therefore refined the phasing of the credit and global multi-channel releases. Additionally, to avoid any disruption to 2016 peak trading, they plan to defer the roll-out of the main brands until early 2017 so there will be a modest delay to the projected flow of benefits announced previously, although the overall costs and benefits of the project remain unchanged.

The group has made a couple of changes to their guidance for 2016. Product gross margin has fallen from -25bps to +50bps to -75bps to flat; but financial services gross margin range has improved from -300bps to -200bps to -100bps to flat. All other guidance remains unchanged and the current consensus trading pre-tax profit is around £84.3M.

Overall then, this is actually quite a decent update. Sales were up overall and the core brands of JD Williams, Jacamo and Simply Be all performed well and the US stores seem to be making progress. The group seem to have shrugged off difficulties relating to the warm autumn period and, although margins seem to be falling this year, the shares are looking like a decent investment at the moment in my opinion.

Overall then, much like most of the other housebuilders, this has been a good year for the group. Profits were up, net assets increased and the operating cash flow improved to give the group some free cash to play with. Completions were up, sales prices increased, the margin improved and the land bank grew. The cost of land did increase slightly compared to the sales price and skilled labour shortages did increase build costs too but materials prices have stabilised.

Going forward, there are some sizeable developments that the group is embarking on and the order book is up from last year. It is worth noting that further growth is likely to come from an increase in sales outlets rather than increased prices and this is a very cyclical business which will be very dependent on prevailing interest rates. There is more debt here (including the deferred terms on land purchases) than some other builders such as BKG which makes this a bit of a riskier investment, and the forward dividend yield of 2.2% is not much to write home about. The forward PE of 8.2 does look cheap but overall I think I am happier being invested in Berkeley than here and I am reluctant to increase my weighting towards such a cyclical sector.

On the 29th February the group announced that following a review of their accounting policies in relation to provisioning for bad and doubtful receivables, they have restated their debtor impairment provisions. This seems to have been prompted by a change of auditor as the previous once, Deloitte confirmed the group’s financial statements were appropriately prepared under IAS 39 but the new one, KPMG seem to disagree.

An adjustment to reduce net assets for 2014 by between £45M and £55M is being made reflecting the impact on net assets from an increase in the provision and a similar, albeit lower adjustment will be required for 2015. These adjustment reflect an increase in the debtor impairment provision level from 8% of gross debtor value to a range of between 17.5% and 19% in 2014; and from 6.5% to a range of between 15.5% and 16.5% in 2015. An estimated increase in the debtor impairment provision to a range of between 14.5% and 15.5% is estimated for 2016.

There are also small changes as a result of these restatements to revenue, cost of sales and gross margin of financial services. The net result of these adjustments is to increase expected pre-tax profit in 2016 by £4M to £7M and between £3M and £4M in the previous year. The quality of the group’s credit book has been improving over recent years which is the primary reason for the upward adjustment to profit for 2015 and 2016 following the higher provision to be made in 2014. I’m afraid I still don’t understand why profit has been increased for 2016, my best hypothesis is that the group was accounting for defaults that were higher than the provision and now the provision has increased, the extra defaults in the next year have fallen?

Separately the board have stated that they remain comfortable with market expectations for the current year before accounting for the increase in profit expected as a consequence of the adjustments. This is all very confusing but it seems like that the underlying trading hasn’t changed.