Newmark Security has now released its interim results for the year ending 2018.

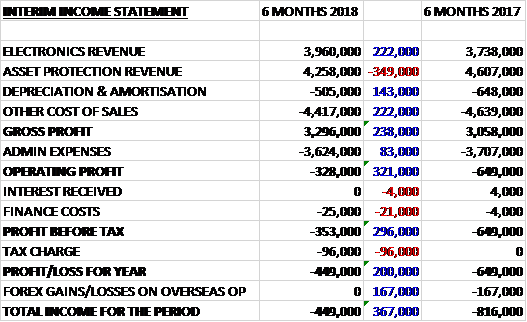

Revenues declined when compared to the first half of last year as a £222K growth in electronics revenue was more than offset by a £349K decrease in asset protection revenue. Depreciation fell by £143K and other cost of sales were down £222K to give a gross profit £238K higher. Admin expenses reduced by £83K which meant that the operating loss improved by £321K. Finance costs increased by £21K and tax charges were up £96K which meant that the loss for the period was £449K, a £200K improvement year on year.

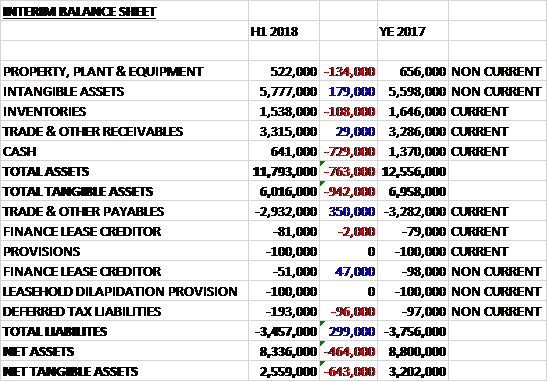

When compared to the end point of last year, total assets declined by £763K driven by a £729K fall in cash, a £134K decline in property, plant and equipment and a £108K decrease in inventories, partially offset by a £179K growth in intangible assets. Total liabilities also declined during the period, mostly due to a £350K decrease in payables. The end result was a net tangible asset level of £2.6M, a growth of £643K over the past six months.

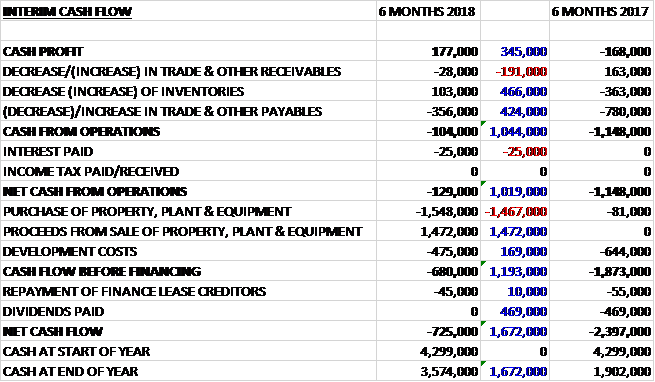

Before movements in working capital, cash profits improved by £345K to £177K. There was a cash outflow from working capital and after interest payments increased by £25K the net cash outflow from working capital was £129K, an improvement of £1M year on year. The group spent £475K on development costs and £1.5M on property, plant and equipment, although they also brought in £1.5M on asset sales which meant that there was a cash outflow of £680K before financing. The group spent £45K on finance lease repayments to give a cash outflow for the period of £725K and a cash level of £3.6M at the period-end.

Revenues in the Asset Protection division declined by £349K. Safetell revenue was 7.6% lower, mainly as a result of reduced contribution from sales of time delay cash handling equipment to the Post Office as it enters the last year of its Network Transformation Programme, which resulted in overall sales of cash handling equipment by 67%. Trading conditions remained challenging whilst the continuing economic uncertainty has resulted in budget cuts and cancellation of planned work by several customers, including government departments. The cost saving initiatives implemented in January 2017 are reflected in the results but further cuts have taken place in H2 2018.

Products revenue was 15% lower but revenue of non-cash handling equipment increased by 57% as a result of renewed marketing and sales efforts. Revenue from Eclipse rising screens was 28% higher as a result of two programmes of work by long standing financial institution customers. Revenue from fixed glazing products continued to decline as they see clients moving away from ballistic protection counters to less secure open counter trading to improve customer relations. After a few years of decline they have seen a 44% increase in revenue for Secure Panel Systems after they obtained additional certification and made significant improvements to the product line. They continue to explore and develop other product offerings which will reduce their reliance on rising screen revenue streams in future.

Service revenue was 14% higher. Margins were maintained due to cost cutting efforts and improved mix of work, but revenue will remain challenging for the division as a result of the continued impact of branch closures that is occurring in the banking sector. As a result, there has been a migration away from traditional work and they are seeing improved opportunities in other markets. They are apparently in the process of renegotiating the renewal of some larger service contracts so hopefully that will go OK.

Revenue in the Electronics division increased by £222K. Within Access Control, the fall in revenue from the legacy Janus range was more than offset by the growth in revenue from the Sateon range. Due to Microsoft’s discontinued support for the 32-bit Windows operating systems on which Janus runs, no new Janus systems were installed and sales declined by 35% to £665K. A significant proportion of the remaining revenue is from recurring software service agreements for existing sites so is expected to decline at a much less pronounced rate in future periods.

The demise of previous generation products has continued to help drive sales of the Sateon line with the Janus-Sateon upgrade programme being extended for another year. Sateon access control revenue saw an increase of 23% to £1.3M. Sateon Advance has continued to be well received by the market since its launch in November 2016. In the period the quantity of new systems installed increased by 86% over the corresponding period last year with the average revenue per system also increasing by 21%.

Development work started to create non-proprietary variants of the Sateon Advance range to allow the hardware to be integrated with third party vendors’ software. By adopting an open protocol approach, incremental revenue is being generated as new channels are developed. Within the period a contracts was won with a major European Workforce Management software provider to supply this hardware as an OEM product to integrate with their proprietary access control systems. Other negotiations are underway with major US and UK based third party access control providers with a view to supplying this line as OEM products.

Across the UK and US, sales of Workforce Management grew by 21% to nearly £2M. In the UK the range of RS series products showed growth of 32% largely driven by requirement for access control products in the HCM sector. The Linux based IT series showed growth of 33%, aided by a contract for one of the world’s largest steel producers, which was completed in the period. They also agreed in November new ongoing supply agreements for the IT51 Linux based workforce management terminal with Workforce Software, an HCM solution provider based in the UK and US. In addition to the hardware a range of remote support tools on a SaaS basis are also being provided, furthering the group’s ambition to generate additional recurring revenues from SaaS.

Also in November it was announced that Grosvenor Technology had won a contract with a leading European Workforce management provider for whom the OEM variant of Sateon is being supplied. The client preferred the industrial design of the GT-10 Android based terminal but wanted to take advantage of the hosted support services that Grosvenor provides within the Linux based terminals. As a consequence, a hybrid solution was developed and this unit will replace a competitor’s product as their flagship hardware offering. The business will also provide a Linux based OEM variant of its GT-10 terminal in addition to a range of cloud based support services on a SaaS basis. The customer is funding development work value of €190K and revenues are expected to come on stream in Q2 2018 with the contract value expected to be €3M over a five year period.

The US operation saw sales increase by 17% to $726K. Negotiations continued with a tier one HCM solutions provider with a view to Grosvenor providing an OEM variant of the GT-10 terminal. These discussions have been underway since the second half of last year but it is felt that they will conclude in H2 of this year. Negotiations are also underway with a second tier one potential customer, again for an OEM variant of the GT-10. Early stage indications are that the proposition is well placed and thus the pipeline to enable future growth continues to be encouraging.

Going forward the group has continued to be affected by challenging market conditions during this period of economic uncertainty together with the anticipated decline in sales to the Post Office. The board anticipates making further contract announcements in the near future and these together with the two contracts mentioned above are expected to improve results in future years.

As the group is loss making, PE ratios make no sense and I can’t find a forecast for this year. There are no dividends being proposed.

Overall then, the group is still struggling but results have improved slightly from last year. Losses improved and the operating cash outflow also got a little better. The net asset level continued to deteriorate, however. The Asset Protection division is struggling due to the continued reduction in the Post Office contract and other customers cutting budgets. The Electronics division looks healthier, however, with growing SATEON revenues and some interesting new contracts where the group is supplying some OEM solutions.

It is hard to say whether these are worth buying yet. I do see some improvements but they seem a little too risky, being loss making. Perhaps one to keep a relatively close eye on.

On the 18th April the group announced that it has received a formal contract extension for the supply of physical security equipment and preventative maintenance to the UK branch network of a leading worldwide supplier of retail banking services.

The contract consists of secured orders for the supply of service and maintenance support for fast rising screens totalling £1.2M, along with the supply of new fast rising screens and auxiliary physical security products which is expected to total around £300K. This is a one year extension to an original contract agreed in 2012 and covers the period ending November 2018.

On the 30th April the group announced that it had secured a new supply agreement for physical security equipment including time-delayed cash handling equipment and secure cash storage units for a major high street financial institution. The agreement will run for five years with options to extend for up to eleven years in total. The first year projections are estimated to generate between £1M and £1.5M of product and installation revenue. This is a current customer for the group and they have supplied them for over 14 years.