Omega Diagnostics has now released its final results for the year ended 2016.

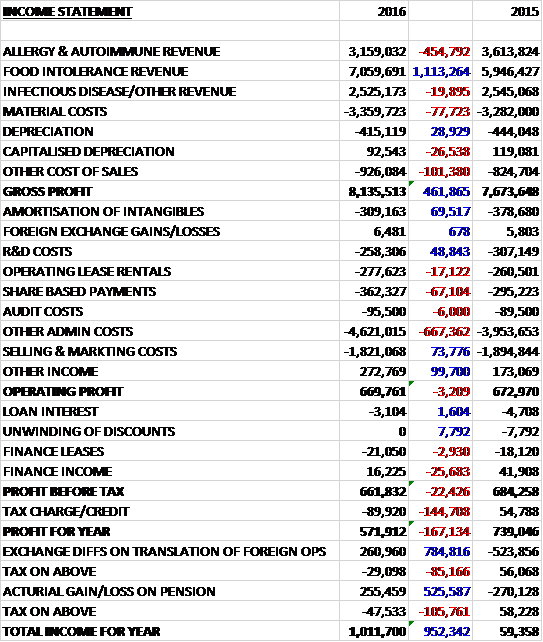

Revenues increased when compared to last year as a £455K fall in allergy & autoimmune revenue and a £20K decline in infectious disease & other revenue was more than offset by a £1.1M growth in food intolerance revenue. Material costs were up £78K and other cost of sales increased by £100K which meant that gross profit was £462K higher than last time. Amortisation fell by £70K and R&D costs decreased by £49K but share based payments were up £67K and other admin costs grew by £690K reflecting an expanded board, an increase in staff and rent costs in Pune and an increase in costs relating to auto enrolment in UK pensions. We then see selling & marketing costs down £74K and other income up £100K reflecting a further credit from the UNITAID grant, which gave an operating profit broadly flat on 2015, down by just £3K. Finance income was down £26K, however, and there was a £145K detrimental swing in tax charges relating to a prior year deferred tax adjustment as tax losses were surrendered and tax was underprovided for in previous years which meant that the profit for the year came in at £592K, a decline of £167K year on year.

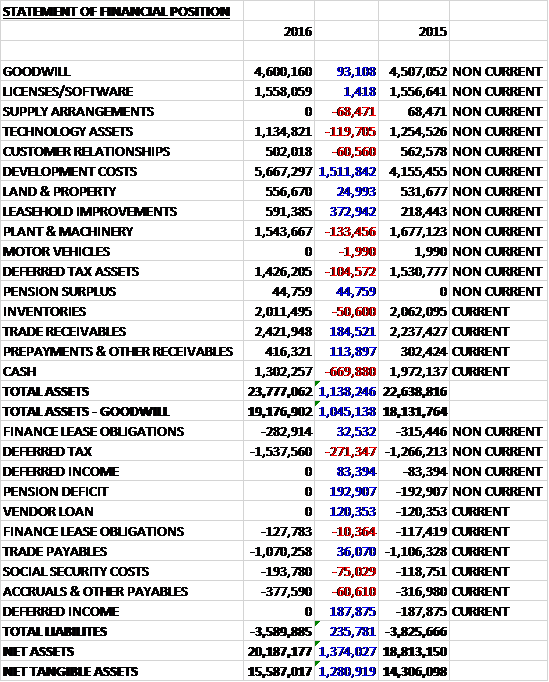

When compared to the end point of last year, total assets increased by £1.1M to £23.8M, driven by a £1.5M growth in development costs, a £373K increase in leasehold improvements and a £185K growth in trade receivables, partially offset by a £670K decline in cash and a £133K fall in the value of plant and machinery. Total liabilities decreased during the year as a £271K growth in deferred tax liabilities was more than offset by a £193K fall in the pension deficit and a £231K decline in deferred income. The end result was a net asset level (excluding goodwill) of £15.6M, a growth of £1.3M year on year.

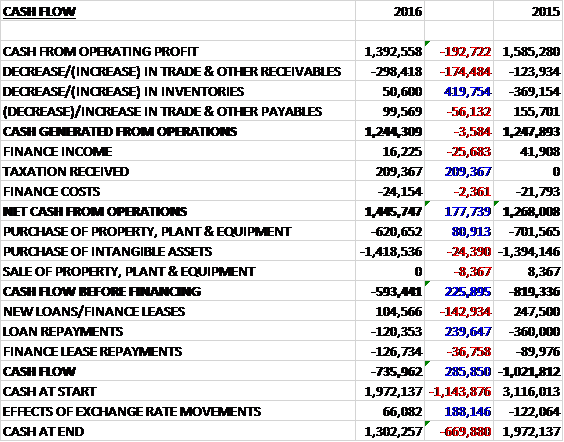

Before movements in working capital, cash profits declined by £193K to £1.4M. There was also a cash outflow from working capital due to a growth in receivables but the effect was less than last year as inventories fell. After finance income was down £26K and the group received a £209K tax payment, the net cash from operations came in at £1.4M, a growth of £178K. This was just about all spent on development costs, mainly reflecting the development of Allersys (£950K) and Visitect (£490K), and the £621K also spent on property, plant & equipment (about half relating to the fit-out of the Pune facility) meant that there was a cash outflow of £593K before financing. This outflow increased after the payment of finance leases and a small repayment of the loan to give a cash outflow of £736K for the year and a cash level of £1.3M at the year-end.

The operating loss in the Allergy & Autoimmune business was £320K, an increase of £82K year on year. Allergy sales fell by £510K to £2.6M, not helped by the weak Euro, and autoimmune sales increased by £60K to £590K. The allergy sales continue to be derived almost entirely from the German business which has experienced a reduction in sales due to continued reimbursement restrictions. The modest growth in autoimmune sales reversed a recent downtrend due to growth n India and China.

The operating profit in the Food Intolerance business was £2.5M, a growth of £415K when compared to last year. Sales of Food Detective grew by 10% to £2.3M with good growth from Europe, Latin America and China. Total volumes achieved were 181,000 units, a growth of 11%. Sales of Foodprint reagents grew by 38% to £3.5M with strong performances in Europe, North America and the Middle East. The group sold a further 18 instruments in the year, taking the number of installations up to 168 instruments.

The CNS lab service showed a decrease of 11% in sales to £580K. Sales were dominated by the markets in the UK and Ireland and they produced 7,008 patient reports in the year with an average price of £82.73 per report, compared to 8,241 reports at £79.33 per report last year. Food intolerance will continue to be a key growth driver for the group. This has been reflected in the increase in staff to provide technical support for the CNS product range. The growth trajectory is expected to continue with this core business supported by increasing the range of products and services in the health and wellbeing market which now extends to 75 countries.

The operating loss in the Infectious Disease business was £244K, an improvement of £24K when compared to 2015. Sales were broadly flat with increases in Bangladesh and Nigeria offsetting a downturn in Brazil due to the economic issues there. These products operate in a very competitive market but the board expect to see increases in sales from the introduction of new products such as CD4 and malaria rapid tests coming through the Global Health programme and the Pune operation.

Significant efforts continued to be made in the year on the allergy development with the optimisation of 41 allergens being achieved in April. All of the Allersys reagents have been validated on the IDS iSYS analyser, demonstrating performance that matches the market leader. Inventory build is underway for the launch, which is expected to be over the next few months. Work is already being carried out to increase the number of allergen tests, both in house and with an external development partner.

With external evaluations having now been completed in Spain, Italy and France, and a fourth evaluation currently being completed in Germany, they will have sufficient data to allow them to apply the CE Mark to all 41 allergens, a prerequisite for marketing any diagnostic test in Europe and beyond. They have identified a plan to increase the number of allergens from 41 to 120 over the next three years. Commercialisation discussions are at an advanced stage with IDS about how best to launch into the market.

In addition to the Allersys programme, the group have taken steps to reinvigorate an allergy dipstick product called Allergodip by expanding the panel of tests available to include country-specific panels. This, alongside the introduction of a mobile app that allows quantification of the test result, will provide them with a much broader product offering and one that will appeal to many of the resource poor countries they operate in. India, with a large number of small labs, is a particular target market for this product.

For the Visitect CD4 device, the group have concentrated their efforts to resolve the ambient temperature effect. The root cause of this was determined and it was anticipated that they would need to work with design companies to provide a one-step solution to the effect because a sample pre-treatment step was required. They continued to also investigate possible alternative designs, however, and subsequently demonstrated that they can manufacture devices which indicate operating performance at temperatures between 20 and 35 degrees (a key design goal parameter) during in-house testing, without the need for a sample pre-treatment step. This is currently undergoing exhaustive testing with patient samples at a local hospital site but the aim is to ensure that they can retain the performance so that the test can be run in the field by community healthcare workers without access to lab facilities.

The group still need to undertake clinical field trials and obtain regulatory approvals once they have a finished test. Other infections disease opportunities presenting themselves include the development of new tests for dengue fever.

During the year the group completed the fit-out of the manufacturing facility in Pune, funded in part with a grant contribution of £540K from UNITAID. In addition to providing capacity for Visitect, the first products to be made there will be a range of malaria rapid tests. The equipment needed to manufacture these tests has now been installed and has undergone operational qualification. Prototype devices have been manufactured on a small scale and, when tested on samples, indicate a level of performance equivalent to a market leading product.

When the manufacturing procedures have been finalised, the equipment will complete its production qualification and will enable larger batches of tests to be manufactured for verification and validation, and they have been able to source a number of malaria-positive and negative samples on a commercial scale which can be stored and used for this purpose when needed.

Colin King joined the board as COO in August and has introduced a number of initiatives to improve processes, communication and plan execution.

Going forward the board expect to see the good food intolerance performance continuing with the marketing initiatives being planned and reaching the launch stage of the Allersys allergy tests should provide good sales progress over the coming year. There is a robust order book which provides a solid foundation for achieving the first half sales targets.

At the current share price the shares are trading on a PE ratio of 34.2 which falls to 22.4 on next year’s consensus forecast. At the year-end the group had a net cash position of £890K compared to £1.4M at the end of the prior year.

Overall then this has been a mixed year for the group. Profit declined, mainly due to a deferred tax charge and lower finance income; net assets increased and operating cash flow increased, but again this was due to a tax receipt and tax profits declined with no free cash being generated. Incidentally I note that the group is capitalising some depreciation charges which seems a bit nonsensical! The infections disease and allergy divisions are still loss making, although the former did see losses narrow. The same cannot be said for the allergy division which saw losses increase due to continued German reimbursement restrictions.

The Food Intolerance division is the big profit generator which saw its performance improve this year due to increased sales of Food Detective and Foodprint reagents. There is much to be excited about going forward, with the Pune factory coming on stream, continued growth in the food intolerance division, the Allersys device nearly being ready and progress being made to rectify the issues with CD4. With a forward PE of 22.4, this is excitement is probably baked into the share price but I continue to hold what I think is an interesting company with great potential.

On the 2nd August the group announced that it had secured a Scottish Enterprise R&D grant of £1.8M. This grant represents a significant contribution towards the total R&D project costs to fund the planned expansion of the Allersys range or reagents from 41 allergens to 120 allergens over the next three years. A portion of the grant will also be used to establish a global health scientific team to screen future product opportunities for resource limited setting.