Orosur Mining has now released its interim results for the year ending 2016.

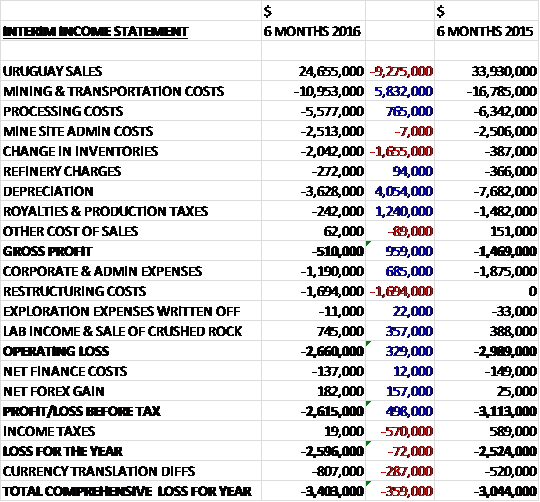

Revenues fell by $9.3M when compared to the first half of last year due to both a reduction in the price of gold and a fall in the amount produced. Cost of sales fell even more though as a $1.7M increase in cost of inventories was more than offset by a $5.8M fall in mining & transportation costs, a $4.1M decline in depreciation following the impairment last year and a $1.2M reduction in royalties after the Uruguay government gave the company a reprieve for a year. The mine site admin costs were broadly flat despite an $881K in additional contingency recognised following a final verdict from the judge relating to a labour claim from 2006. After this, the gross loss improved by $959K when compared to the first half of 2015.

We then see a $685K fall in corporate expenses and a $357K growth in income from the sale of crushed rock and lab services, along with the income from the lease of the exploration camp in Colombia, offset by $1.7M of restructuring costs to give an operating loss some $329K better than last time. There was a decent forex gain but the tax rebate was much lower, presumably due to the effects of the Uruguay peso’s depreciation on deferred tax, which meant the loss of the half year was $2.6M, an increase of just $72K year on year.

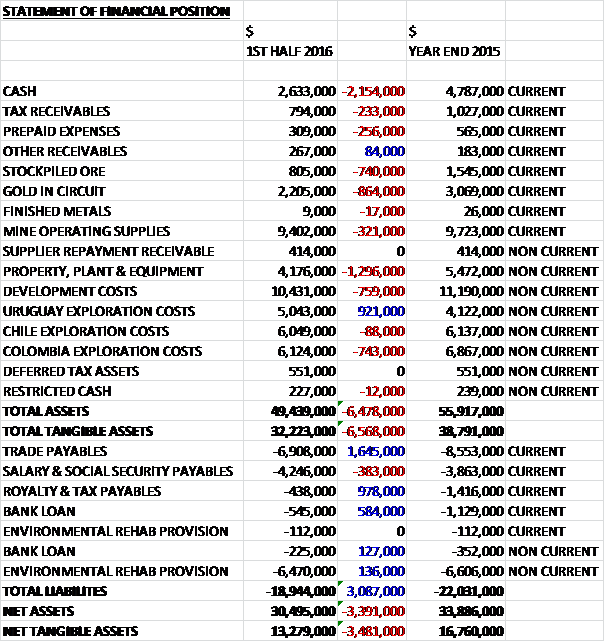

Total assets declined by $6.5M when compared to the end point of last year driven by a $2.2M fall in cash, a $1.3M decline in property, plant and equipment as depreciation outpaced capex, a $743K fall in Colombian exploration costs due to foreign exchange movements and a $1.9M decrease in inventories partially offset by a $921K increase in Uruguay exploration costs. Total liabilities also declined over the past six months due to a $1.6M fall in trade payables, a $978K decline in royalty payables and a $710K decrease in bank loans. The end result is a net tangible asset level of $13.3M, a decline of $3.5M over the last half year.

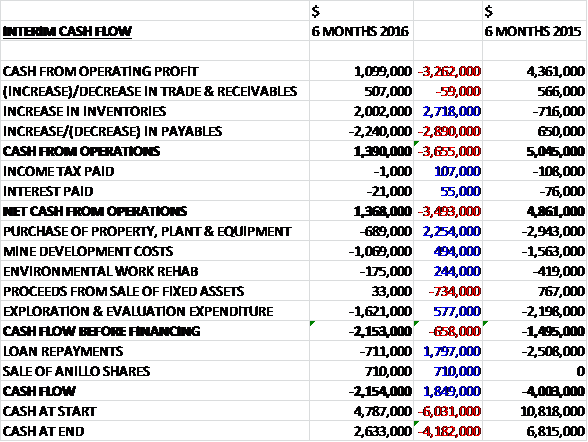

Before movements in working capital, cash profits fell by $3.3M to $1.1M. There was a slight cash inflow from working capital, but much less than last time, so the cash from operations came in at $1.4M, a fall of $3.5M year on year. This did not cover the $1.8M of tangible assets (mainly development costs) or the $1.6M in exploration costs so before financing there was a cash outflow of $2.2M. The sale of Anillo shares paid for the loan repayment so the cash flow for the period was $2.2M and the cash level at the end of the half year was $2.6M.

Despite Q2 being a transition quarter, all in sustaining costs show a significant improvement from last year, falling to $1,166 in Q1 and $1,095 in Q2 but the company expects that the benefits of the programme are yet to be fully realised and will be more pronounced next quarter. Although an improvement, this does not compare that well with the average gold price received of $1,100, down from $1,212 at the same point of last year.

In December the president of Uruguay granted the company an exemption on the royalty payment to the government which covers the period from April 2015 to March 2016. The group have also been able to reduce staff levels by more than 40% and have enacted a reduction in the cash remuneration of the board. (Don’t worry, they are not taking a pay cut as they will be paid partly in shares instead.)

The company produced 8,172 ounces of gold in Q2 compared to 12,854 at the same point of last year with a total of 20,643 ounces produced in the first half. In the quarter, 199,352 tonnes of ore was processed at a grade of 1.34g/t with 319,244 processed at a grade of 1.34g/t in Q2 2014, and 409,268 tonnes was mined which included 192,164 tonnes of ore and 217,104 tonnes of waste at an average grade of 1.39g/t. compared to 318,840 tonnes of ore and 955,806 tonnes of waste at a grade of 1.38g/t during Q2 last year.

In Uruguay the San Gregorio Deeps underground mine project continued to advance through permitting. A prelim permit was issued by the environmental authority in Q1 2016 and the mining permit is currently in process with the mining authority. The main pit of San Gregorio has been de-watered during the last three months and is now ready for about 1,500 ounces to be mined from it. Some initial development work is expected to commence shortly to connect the main ramp of open pit mine with the designed portal for San Gregorio Deeps. Based on limited sampling, a portion of the material in this sections carries grades between 2 and 5g/t, mixed with waste material.

A short infill RC drilling campaign of 500m is underway from the main ramp of the open pit mine with the intention of further defining resources at level 17 of the San Gregorio Deeps project. This work also gives the company the opportunity to potentially advance mining of a chamber as well as gaining geological and geotechnical information to optimise the mining design. At Arenal Deeps, the company is testing a down-plunge extension of the Arenal mineralised structure. A 90m tunnel has been completed to access and make room for more cost efficient drilling with the aim of testing for a net structure within a distance of 300m from the current underground workings. During December, a 1,100m drilling campaign commenced and is expected to continue through to April.

As far as brownfield exploration in Uruguay is concerned, possible extensions of known mineralisation have been identified in a number of locations including adjacent to the open pits at Veta Rey, Laureles and Zapucay mines as well as at Rieles which represents the eastern extension of the San Gregorio main pit extending to the East extension pit. The company is currently focusing its brownfield exploration effort for the remainder of the year in Vesta Rey and in the Sobresaliente area. Here, the main focus will be on advancing known target zones using NSAMT geophysics methods and developing a programme of approximately 5,000m of Pantera drilling.

At Anillo in Chile, a campaign of 13 RC holes totalling 3,600m of drilling was completed on time in December. Drilling tested geologic, geophysical and geochemical indicators of Au-Ag epithermal mineralisation at the central-north, NE, S and W sectors of the project. Testing of all drilling interceptions is currently underway to validate assay results and obtain further information on pathfinder geochemical behaviour. The results to date demonstrate a non-obvious mixture of low and high sulphidation epithermal, thought to be a result of at least four different magmatic events recognised by geoscientists in the region. Additional geochemistry is expected to aid in the preparation of a geological model that interprets the levels of exposure of the dominant mineralisation systems in place. A meeting of the technical committee of Anillo is planned for February to review the results and determine the next phase of the exploration campaign.

Following the negative NPV and write-off of assets at the Pantanillo project the group decided not to fulfil the payment of advanced royalties totalling $1.6M due to Anglo American in December, which triggers the process for the properties to be returned to them which will take place over the coming months and will not have any additional adverse effect on the balance sheet of the company.

As part of the company’s cost reduction plan, a portion of the Anza exploration camp in Colombia has been rented until August to a major mining company exploring a neighbouring district which seems a sensible use of space.

In June the company signed an option agreement for the funding of the next exploration phase at Anillo in Chile with AC. The agreement defines a non-dilutive financing of up to $3.5M in advance of the exploration and states that AC may earn up to a 40% interest in the project. The group incorporated Anillo SPA, an 84% owned associate and transferred the property of the project to the business. AC has subscribed for an initial amount of Anillo shares equal to 16% of the capital for $850K. AC has a further option to elect to earn up 32.5% and then 40% by funding an additional $1.25M and $1.375M. Should AC not fund the purchase of shares in phase 2, they will lose their participation interest.

Phase 1 exploration will include a geophysics campaign and a minimum of 3,600m of RC drilling and have an estimated duration of up to ten months. Phase 2 would include an additional geophysics campaign and a minimum of 5,500 metres of RC drilling and have an estimated duration of 18 months and phase 3 would include further geophysical work and additional RC drilling and also have an approximate duration of 18 months.

In November, in Uruguay, Minerales Cala gave notice to the company of the completion of its expenditures and reported obligation with respect to phase 2 of the option agreement, thereby earning an additional 29% in the project for a total of 80% with Orosur retaining 20%. Phase 3 of the option agreement has commenced and Minerales Cala is obligated to submit a detailed work programme and budget to the company.

In September, also in Uruguay, due to a number of objections concerning the submitted phase 2 expenditures and an ongoing dispute between the parties, the company exercised its right to request an audit of the itemised statement of accounts delivered by Gladiator. Later in the month, Gladiator notified the company that phase 3 of the option agreement will not be completed by the end of December and that it should be considered finalised which terminated their option to acquire a further 29% interest in the project. Once the audit of the phase 2 expenditures has been finalised and the earning of the phase 2 interest is either confirmed or rejected, the parties will be required to renegotiate a new joint venture agreement in order to continue with the development of the project.

The cash balance at the end of the half was $2.6M and the debt balance was $800K with $3M of undrawn lines of credit available.

Overall then this has been another difficult period for the group. Losses were flat year on year but the pre-tax loss improved despite some $1.7M of restructuring costs as the group benefited from reduced staff costs and from renting out their exploration camp in Colombia. Net assets declined, however, as did operating cash flows with no free cash being generated. The group produced less gold when compared to the first half of last year but the real issue is the fact that AISC was $1,095 whereas the sales price for the gold was $1,100 which is hardly conducive to making lots of profit. The company expect the AISC to come down in H2 but where will the gold price be?

This is of course, the crux of the investment case here and until the gold price shows a sustained improvement, I am not investing in this company.

On the 21st January the group announced that it had granted 2,920,000 stock options to its employees. The options are exercisable at a price of C$0.105 per share by the start of 2021 and will vest in three parts with the first vesting immediately and the others in Jan 2017 and 2018. The company also issued 2,103,894 shares to satisfy the termination consideration with Pablo Marcet. Lots of confetti being distributed here, I guess cash is very tight.

On the 3rd March the group stated that it had granted an aggregate of 193,880 stock options and 126,226 shares to directors and officers in lieu of 20% of their standard cash compensation for the last three months which is equivalent to a cash amount of $29,513. This is not a material amount but it does hint at the fact that cash is getting very tight here in my view.