President Energy have now released their interim results for the year ending 2018.

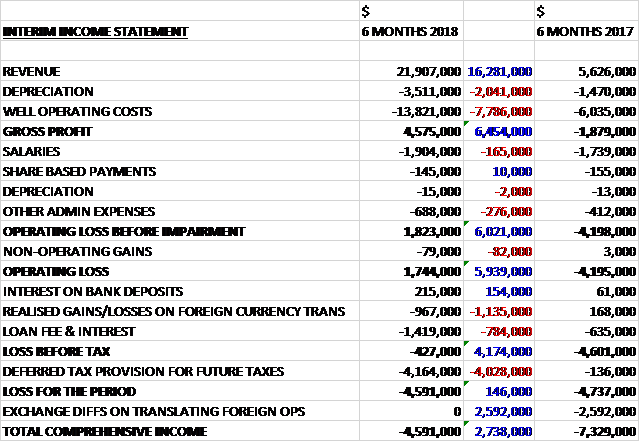

Revenues increased by $16.3M when compared to the first half of last year. Depreciation was up $2M and well operating costs increased by $7.8M to give a gross profit $6.5M higher. Wages increased by $165K and other admin expenses increased by $276K which meant that there was a $5.9M swing to an operating profit. There was a $1.1M negative swing to forex losses and loan fees increased substantially, up $784K which meant that there was still a pre-tax loss, although this showed an improvement of $4.2M. There was a considerable deferred tax charge, however, which meant that the loss for the period was $4.6M, an improvement of just $146K year on year.

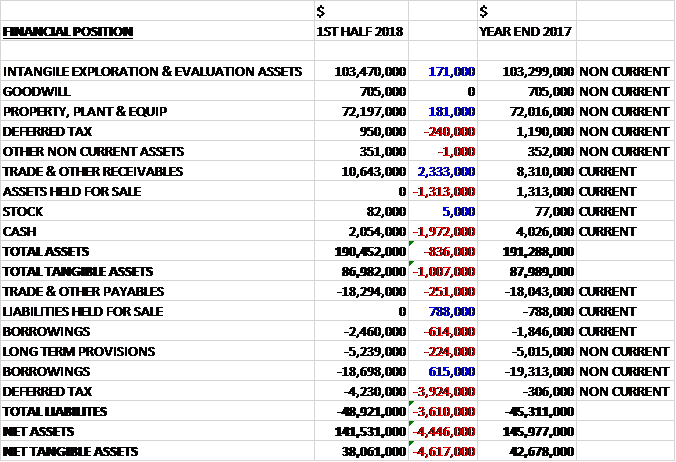

When compared to the end point of last year, total assets declined by $836K driven by a $2M decrease in cash and a $1.3M elimination of the assets held for sale, partially offset by a $2.3M increase in receivables. Total liabilities increased during the period as a $788K elimination of the liabilities held for sale was more than offset by a $3.9M increase in the deferred tax liability. The end result was a net tangible asset level of $38.1M, a decline of $4.6M over the past six months.

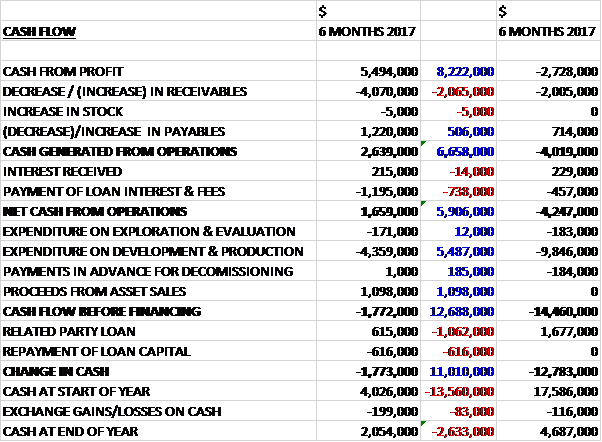

Before movements in working capital, cash profits increased by $8.2M. There was a cash outflow from working capital and a $738K jump in loan fees so the net cash from operations was $1.7M, an improvement of $5.9M year on year. The group spent $171K on exploration and $4.4M on development and production but recouped $1.1M from the sale of some assets to give a cash outflow of $1.8M before financing. This was also the cash outflow for the period as a whole to give a cash level of $2.1M at the period-end.

The average group production in the period increased by nearly 200% to 2,064 boepd notwithstanding some disruption to production caused by the extensive workover programme in Argentina and prolonged flooding in Louisiana at the start of the year.

The twelve well workover programme boosted production in June to over 2,000 boepd gross in Rio Negro while production at Puesto Guardian was stable at around 500 bopd, contributing to the group with margin improvements. Louisiana continues to contribute solid and stable profits, returning between $200 and $250K cash per month to the group.

The US average realised oil prices increased by 38% to $65 per barrel and now stand at $71 per barrel. The Argentina average realised price increased to $65 per barrel at Puesto Flores and up by $6 per barrel to $56 per barrel at Puesto Guardian and these are the same as the current prices.

Group well operating costs reduced by 14% to $33.50 per boe and continued to reduce in H2 with the group average to date being $24.66 and expected to fall further as production from new wells and the synergy benefits from the forthcoming acquisitions come on line through 2019.

The farm out process in Paraguay continues. The group is in any event starting the preparatory work to be able to drill a well in 2019 to explore the potentially oil-bearing targets in the Pirity blocks. At this stage is it expected that the well will address a prospect in the Imperial Complex of prospect and leads, some 30km across the border from the prolific Palmar Largo oilfield in Argentina, as further studies of the 3D seismic have demonstrated clear and directly defined analogues to the anomalies shown in Palmar Largo. The complex is estimated by management to contain nearly 200 MMBO of prospective resources. If no farm out on terms satisfactory to the group is achieved, they intend to drill the well in H2 2019, the cost of which is currently anticipated will be met out of their own financial resources and facilities. Costs of the well are estimated to be substantially lower than the previously drilled wells in Paraguay. The Pirity block has been continued for another two years and is now expiring September 2020.

In Louisiana the Pacific Enterprise non-core well, previously a producer that had watered out and been shut-in, was reopened and worked over as a future water disposal well to support the group’s producing wells. The costs of the work were paid in full by a company owned by the CEO and Chairman of President who in consideration acquired a 75% stake in the well. Always slightly dubious of these kinds of deals. Prior to conversion, a zone higher up in the well was perforated as a last opportunity to identify any movable hydrocarbons. A short test gave a positive result which may lead to gas production. It is too early to identify what sustained production may be generated.

Going forward the first three months of H2 already demonstrate a substantial improvement on H1 with EBITDA showing material increases from the first half as they benefit from higher production levels, improving operational efficiencies and economies of scale. The acquisition of Puesto Prado and Las Bases concessions in Argentina are projected to take place before the year-end which would provide the group with additional production from the start of 2019 together with over 60km of gas pipeline infrastructure to deliver gas direct to market.

Whilst there has been recent turbulence in the macro-economic environment in Argentina, the group is not experiencing any material adverse cash impact as a dollar denominated business.

After the period-end, the current group production stands at 2,700 boepd. A fully funded three well drilling programme is underway at the Puesto Flores field aimed at increasing field production by a further 600 bopd. An extensive 2019 drilling programme is now in the planning stages, comprising new production and exploration wells, workovers, re-activations, facilities and infrastructure work in each of the present and soon to be acquired Argentine fields, in addition to an exploration well in Paraguay expected to be financed out of cash flows.

The work to power the group’s Puesto Flores and Estancia Vieja fields using Estancia Vieja gas is in hand and is due to be completed by the end of January producing significant savings with Puesto Prado likewise to be powered later in 2019. The first half of 2019 will see a reduction in major capex in order to build up cash strength in anticipation of a concentrated wide scale drilling and infrastructure development programme in the second half of the year. Very sensible and great to hear.

The shares are still loss-making so a current PE ratio would be impractical but the consensus forecast for this year as a whole is a PE of 34.6 which falls to 8.6 on next year’s forecast. There are no dividends on offer here.

On the 15th October the group released a Louisiana update. They have acquired and signed a lease with the Louisiana authorities for a 693 acre production block known as Jefferson Island. The bonus paid to the State of Louisiana for the lease was $175k. Meridian will be the operator of the block in which it will be a 20% participant.

Jefferson Island currently has plugged and abandoned wells but has in the past been a prolific oil producer. It is conveniently located within a manageable distance from the group’s other assets in the area. The group takes the view that there remains significant undrained low risk potential in the area with the first stage to reprocess with the latest technology 3D seismic previously acquired.

With several leads already identified it is expected that a four well drilling programme will start towards the end of Q2 2019 with each well having an estimated cost of $2M, $400K net to President. It is expected that these costs will be met out of the group’s existing resources. Previous well drilled in the island have generated initial production of up to 400 bopd.

Overall then this has been a period of considerable progress for the group. Losses improved, but the group is still loss-making before tax. Net assets declined but the operating cash flow improved but it should be noted that the group is still some way off generating any free cash. Things continue to improve in the second half of the year with production now up to 2,700boepd, the oil price received improving and costs going down. Indeed the PE ratio for 2019 comes down to 8.6 which seems about right. I continue to hold, although I am keeping an eye on that increasing debt.

On the 22nd October the group announced a drilling update covering Puesto Flores. The PFOI development well, being the first in the sequence of three, has now been drilled, cased, cemented and logged on time and in budget. The results obtained to date are at the upper end of expectations. The well was drilled to a total depth of 2,359m with oil shows in at least three different formations.

According to the logs net pay is above 23m with good to excellent porosity ranging from 18% to 25%, the latter being in the primary target zone. A completion rig will be mobilised for early November to test and complete the well where upon it will be tied in as a producer. The drilling rig is now moving on to the next well, PFE 1001, which is expected to spud shortly. The acid test will be the flow rates which are expected to be in November, however.

On the 29th October the group released a statement covering Q3. Turnover increased by 21% over Q2 to $13.1M; adjusted EBITDA doubled to $5.7M and is running at around $2M per month; free cash generation increased by 59% to $6.8M; and group well operating costs per barrel reduced by 20% to $27.18.

The group has now been materially adversely affected by the recent macro economic turbulence in Argentina which has shown some signs of stabilising. Q4 should benefit from the current three well drilling campaign in Puesto Flores which is targeted to add an initial 600bopd to field production and the group is expecting to complete the acquisition of two fields in Rio Negro by the beginning of December which should give incremental production of the group from January as well as providing a strategic pipeline for offtake of the company’s gas.

On the 13th November the group released an update. The PFO1001 well has been tested from only the second deepest target interval and during the test production was over 200bopd with only 2% water, which is in excess of expectations from the well as a whole. It has now been placed on production with an electrical submersible pump.

The main target, the shallower Punta Rosado formation 200m higher up the well was observed to have a net pay of 15m and porosity of 25%. It has been decided, however, that at this time it would not be prudent to test and co-mingle that zone as the group would first like to observe how the deeper intervals perform to gain a greater understanding of reservoir capability prior to bringing the main target on production. In due course this well is likely to result in an increase in the group’s proven oil reserves.

The PFE1001 well has now been drilled on time and budget to the target depth of 2,550m. Live oil has been seen on the surface with good oil shows and gas readings in the mud logs from both the primary Punta Rosado and the secondary Pre Cuyo targets as well as a shallower interval. The mud logs from the Pre Cuyo formation are particularly encouraging as this is the first time that such an interval has been penetrated in the Eastern part of the Puesto Flores Concession.

The rig will now be transported to the next well, PFO1005, which is expected to spud around the end of November. The workover rig will then be brought on to complete this well and subject to successful testing the well should be brought on stream in early December.

It is expected that the acquisition of the Puesto Prado and Las Bases concessions will be completed by early December. The group is making preparations to promptly start production from these concessions through opening up certain currently shut in wells.

Whilst the group has noted the recent decline in international oil prices, the price obtained in Argentina has so far been stable. The oil price expected to be received in November is around $66 per barrel, net backs there are now in excess of $40 after all operating costs but before general and admin costs. The group do not expect to pay any corporate taxes in Argentina before 2020. The Peso/dollar exchange rate has stabilised in the recent past as a result of government action and a perceived growing confidence in the markets.

The declining oil price is a concern if it sustained, but otherwise this seems a very positive update.

On the 22nd November the group released an update. New well PFO1001 is now tied in and producing to the battery at a rate of 600bopd from the primary target, the Punta Rosada formation with zero water cut. The oil quality is similar to that of oil produced in the Puesto Flores field. The secondary target Pre Cuyo interval 200 metres deeper has been temporarily isolated and is being kept in reserve to be brought on production at a later date.

The PFE1001 well has been drilled to budget and has now been logged and cased. The logs show 17 metres of net pay in the Punta Rosada primary target and 26 metres in the Pre Cuyo formation with good porosities between 15% and 25%. At the present time the group maintains its guidance of 200 bopd targeted production from the second and third wells in the programme.

On the 27th November the group announced that the PFO1005 development well at Puesto Flores had been spudded and the recently drilled PFE1001 well is expected to be completed with a workover rig and to be on stream by the end of next week.

On the 28th November the group announced the acquisition of the new concessions from Rio Negro province. They have granted the group 90% operating interests which have a ten year term with the provincial energy company holding the 10% remainder interest. The purchase price was $9.9M with $8.7M having been paid today. This amount was financed through an additional $4M secured term loan with their bank and an additional $4M unsecured loan from the Chairman/CEO.

The loan from the chairman bears interest at the same rate as the bank loan – a rather hefty 12.5% above the LIBOR rate per annum. Las Bases and Puesto Prado have historically audited proven reserves estimated at around 1M barrels which management believe could be expanded to 4M barrels by the end of 2019.

The new concessions have extensive infrastructure facilities as well as a strategic pipeline of some 60km. The group is immediately benefiting from the pipeline income currently being generated from the transport of gas produced by CGC form its neighbouring concession. They will seek to capitalise on their infrastructure by offering capacity to its other neighbours.

The group are now working to bring into production certain wells that are currently shut in on the new concessions and it is expected that both oil production from Puesto Prada and some gas production from Las Bases will contribute to year-end production figures. The process of bringing wells on will continue into Q1 2019.

Testing of the pipeline between Estancia Vieja and Puesto Prado is taking place shortly with a view to initially using the Estancia Vieja’s gas to generate electricity to power the Puesto Prado facilities and wells by the end of the year. It is expected that they will start commercial sales of Estancia Vieja gas to the local market during Q1 2019. The group are provisionally targeting to drill at least one has well at Las Bases in H1 2019 with work there and in Puesto Prado continuing into H2.

On the 7th December the group announced that the PFE1001 well had been completed and tested. The Punta Rosada, having been tested at the rate of around 400bopd with nearly no water and good pressure, will be online by the 10th December with a similar level of initial production expected. This rate of flow is nearly double the expectations and would provide payback within a year on the bases of current oil prices. The drilling of the PFO1005 development well at Puesto Flores is proceeding as planned and the group retains its guidance of 200bopd.

The final part of the deferred consideration payable to the Rio Negro province of $1.8M has now been paid.

On the 18th December the group announced that well PFO1005 had been drilled on budget. Both the primary and secondary targets resulted in good oil shows with results in line with expectations. The well is currently expected to be placed on production around New Year with expectations of 200bopd initial production.

On the 20th December the group announced that the first two Puesto Prada oil wells have been reactivated and are producing in line with expectations. It is anticipated that a further three to four wells will be reactivated and brought into production. The oil is currently being shipped for treatment and sale by road transport but over the course of 2019, after necessary infrastructure works, Puesto Prado’s own battery will be reactivated which will allow the oil to be sold directly to nearby refineries.

After testing of the 15km of newly acquired pipeline between Estancia Vieja and Puesto Prado, gas has flowed from between the two. They are currently proceeding with the testing and commissioning of the next section of pipeline between Puesto Prado and Las Bases.

On the 9th January the group released an update where they stated that they had beaten their 3,000boepd target for net group production at the end of 2018. They are producing at a met group level of around 3,300boepd which represents a 50% increase year on year and is being achieved without the benefit of any contribution from the Las Bases concession and with only a limited contribution from the Puesto Prado and Estancia Veja fields. Commercial gas sales from the Las Bases and Estancia Vieja concessions are expected to start by the end of Q1 2019.

Well PF0 1005 has now been tested and placed on production with initial levels of around 250bopd, being in excess of expectations. Management expects that the next reserves audit published in March will show a significant increase in P1 proven reserves at Rio Negro due to the drilling and workover campaigns delivered in 2018.

Operational work in Q1 2019 will include preparation and planning of the next drilling campaign in Argentina due to start in Q2 as well as long lead planning for 2019 exploration in Paraguay; workover campaigns in Rio Negro to bring on new production from currently shut in wells in the Puesto Prada and Estancia Vieja fields; starting of added value commercial gas production and pipeline sales from existing shut in wells at the Las Bases and Estancia Vieja fields; electrification of the Rio Negro fields using the group’s own gas making operational savings and avoiding power outages; installation of a dual fuel power system in the Dos Puntitas field; preparation and planning of a four well drilling campaign starting in Q2 in Louisiana; and continued focus on margins.

On the 25th February the group announced that it had raised £6.5M from the issue of 81.25M new shares. Following on from the latest acquisitions in December together with the purchase of a gas pipeline network, the group had identified opportunities to accelerate their expansion programme in Rio Negro through the fast track development of their gas assets. This is rather disappointing, I thought we might have been at a point where the group could be self-sustaining but I suppose that is a bit of a pipedream.

On the 25th March the group gave some details of how the money will be spent. The estimated cost of the work programme between now and the end of 2020 is around $50M and is anticipated to be funded from existing resources (I should hope so!)

From now, until mid-2019 an aggregate of at least ten workovers in Puesto Flores, Estancia Vieja, Puesto Prado and Las Bases will be carried out with the rig currently being mobilised to the first well location. By the end of May, the renovation and commissioning of the oil treatment plant in Puesto Prado will be undertaken. The start of deliveries of oil from the field direct to local refineries will give enhanced margins. From the end of May to November the first phase repair, upgrading and commissioning of the gas plant in Las Bases will take place in order for it to have the capacity to handle initially up to 250Km2 of gas of the group’s own gas per day by the end of October.

From July to the end of the year there is a target of seven new production and appraisal wells. By the end of September, the erection and completion of 14km of new overhead electric lines between Estrancia Vieja and Puesto Flores and the commissioning of an electricity generation plant to power the latter field from the former’s gas and to sell surplus electricity generated to the grid.

By the end of October the restart of increased volumes of gas flowing through the building, completion and commissioning of a new 16km section of steel pipeline to be laid between Puesto Prado and Las Bases, replacing the limited capacity pipeline between those points. There will also be the start of a further workover programme from October and the continuation of infrastructure works throughout 2019.

In 2020 is it planned that there will be a drilling programme of an aggregate of eight new wells in Las Bases, Puesto Prado, Estancia Vieja and Puesto Flores; phase two of the upgrading of the Las Bases gas plant will be completed to increase its capacity to 1M M3 of gas; and an aggregate of at least eight workovers in wells in various fields in Rio Negro will be carried out.

By the end of 2020 the group’s borrowings will have reduced by over $6M as they are repaid. In addition to the above programme, planning work will continue for the drilling of up to two development wells in Puesto Guardian, one exploration well in Pirity in Paraguay, and up to four exploration wells at Jefferson Island in Louisiana. The group is targeting 50% exit production growth in 2019 and 2020.