Qinetiq has now released its final results for the year ended 2016.

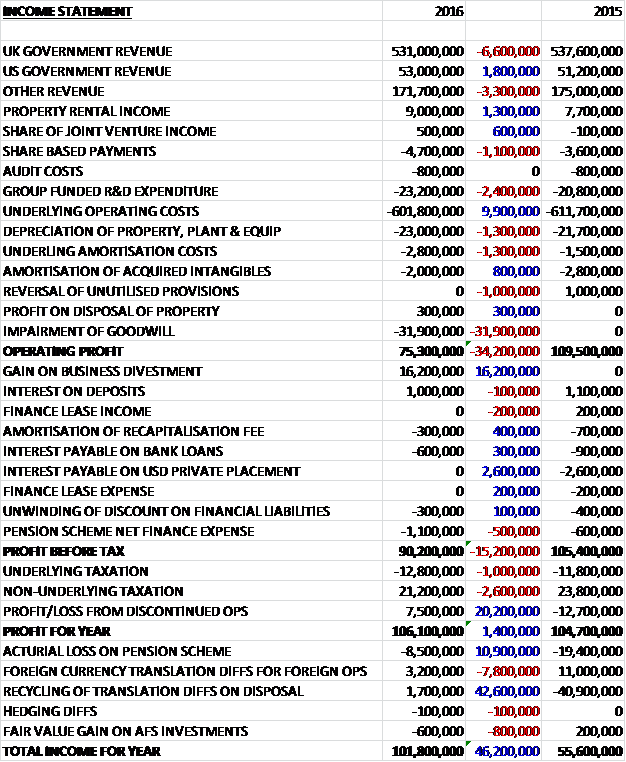

Revenues declined when compared to last year as a £1.8M increase in US Government revenue and a £1.3M growth in property rental income was more than offset by a £6.6M fall in UK Government revenue and a £3.3M decrease in other revenue. Share based payments increased by £1.1M, R&D expenditure was up £2.4M, depreciation increased by £1.3M and underlying amortisation was up £1.3M, although other underlying operating costs fell by £9.9M. We then see a £31.9M impairment of goodwill which meant that the operating profit declined by £34.2M when compared to 2015. Counteracting this we see a £16.2M gain on the sale of a subsidiary, relating to the sale of the Cyveillance business for $34.1M, and interest payments came down considerably to give a pre-tax profit down £15.2M. Tax costs were up £3.6M due to a large one-off tax rebate following the change in rules surrounding R&D tax credit reporting, but a £7.5M profit from discontinued operations relating to the release of provisions gave a profit of £106.1M, a growth of £1.4M year on year.

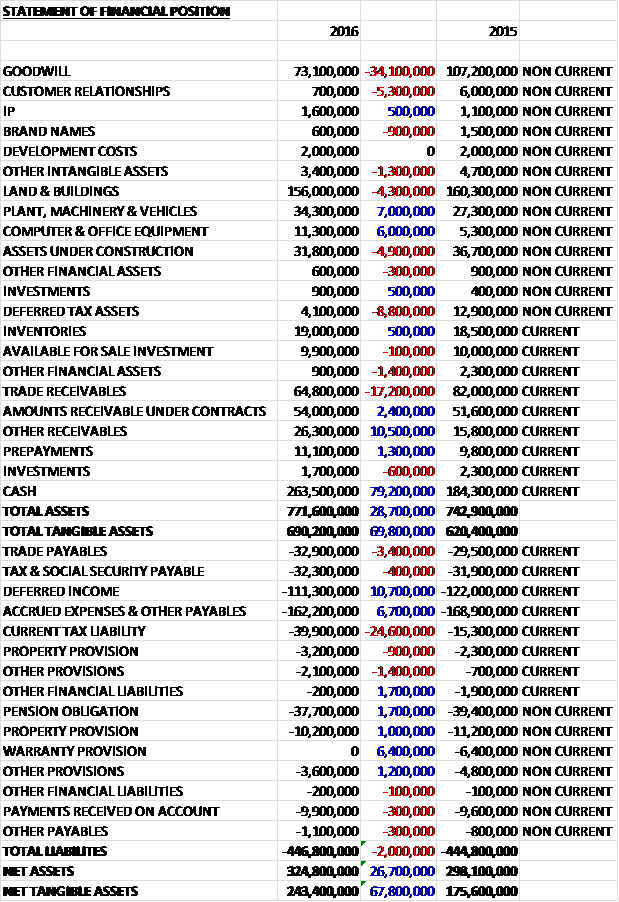

When compared to the end point of last year, total assets increased by £28.7M, driven by a £79.2M growth in cash, a £10.5M increase in “other” receivables relating to the potential insurance payment due to the potential US tax liability, a £7M growth in property, plant and equipment, a £6M increase in computer and office equipment and a £2.4M growth in amounts receivables under contracts, partially offset by a £34.1M fall in goodwill due to impairments and disposals, a £17.2M decline in trade receivables, an £8.8M decrease in deferred tax assets as tax losses were utilised, a £5.3M fall in customer relationships due to divestments and a £4.9M decline in assets under construction. Total liabilities were broadly flat as a £24.6M increase in current tax liabilities due to the court decision in the US was offset by a £10.7M fall in deferred income, a £6.7M decrease in accrued expenses and a £6.4M decline in warranty provisions. The end result was a net tangible asset level of £243.4M, a growth of £67.8M year on year.

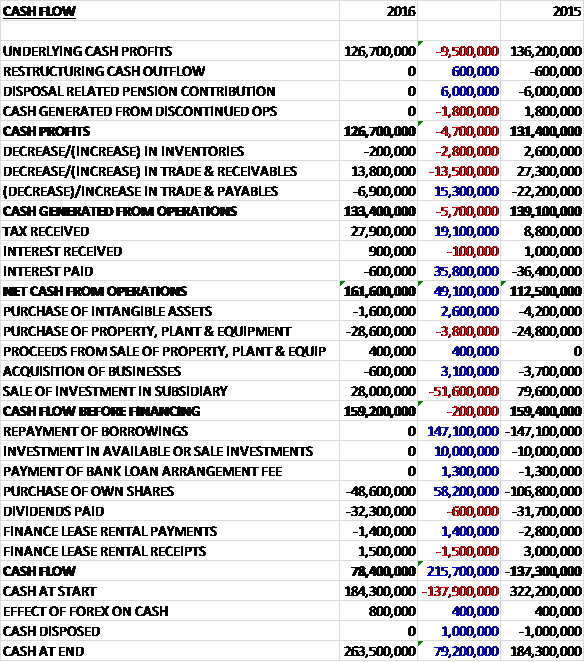

Before movements in working capital, cash profits declined by £4.7M to £126.7M. There was a cash inflow from working capital due to a fall in receivables, but this was less pronounced than last year to give an operating cash flow down some £4.7M. There was a one-off tax rebate of £27.9M and interest costs fell by £35.8M to give a net cash from operations of £161.6M, a growth of £49.1M year on year. The group spent £28.6M on property, plant and equipment along with £1.6M on intangible assets but a receipt of £28M from the sale of a subsidiary meant that there was a hefty free cash flow of £159.2M although the group have pointed out that capex will increase next year due to investments in the LTPA and other long term contracts. Of this, £48.6M was spent on share buy-backs and £32.3M was spent on dividends to give a cash flow of £78.4M for the year and a cash level of £263.5M at the year-end.

In the UK the MOD has declared plans to address important capability gaps such as maritime surveillance and combat air numbers. These plans will require immediate savings to be made elsewhere to fund them, with the government looking to achieve a 30% reduction in MOD civilian staff and in built estate, and to deliver £11BN of savings from defence and security budgets over the next four years. The savings programme could provide further opportunities for outsourcing, along with the increased MOD presence on the group’s sites. There is likely to be increasing competition but the group is well positioned due to its strong record in delivering improved services combined with significant savings for customers.

The SSRO has confirmed the baseline profit rate for new single source defence contracts is 8.95% compared to the 10.6% over the past year. About 70% of the EMEA Services revenue is derived from single source contracts, including the non-tasking element of the LTPA. It is thought that the majority of single source revenue will fall under the regulations within three years.

In the US the defence downturn is reaching the bottom of the cycle with the president requesting continued increases to the defence budget and the budget for overseas contingency operations. A renewed commitment by US military customers to unmanned systems products is reflected in plans to award new competitive programmes of record over the next two years to enhance and sustain the US unmanned systems capability in the DoD budget. The president has also requested an increased R&D budget for defence.

The Australian government is responding to the need to modernise its defence equipment and now plans to replace the majority of their platforms over the next 15 years, supported by an increase in defence expenditure to 2% of GDP. The Canadian government pursues similar defence transformation programmes to the UK and they value the advice, test and evaluation that the group can provide in support of better procurement.

In Sweden the defence budget is similar, with budget pressures evident against a backdrop of heightened security threats. In Turkey and the Middle East, budgets remain more robust, offering increased export opportunities for defence products and services, albeit these and other nations are determined to develop indigenous capacity for both economic and sovereignty motives.

The operating profit in the EMEA Services division was £93.8M, a growth of £800K year on year, assisted by a credit of £3M due to the resolution of a historical overseas exposure. Each of the core Air and Space, Maritime, Land and Weapons and Cyber, information and training businesses delivered a solid performance despite the uncertainty resulting from the UK Strategic Defence and Security Review published in November, along with budgetary pressures. Orders grew 7% to £495.4M driven by the timing of multi-year contract awards, including the £153M five year UK MOD renewal for aircraft engineering services, with some continued de-scoping and delay in other orders in a challenging market environment.

The Air and Space businesses were combined in April 2016 to increase collaboration in the engineering capabilities to de-risk complex aerospace programmes. The business is working in partnership with the MOD and the supply chain to implement a new model to transform the provision of aircraft test and evolution. During the year, it was awarded two single source contract renewals under this new model, worth a combined £153M over five years, to deliver technical services to fast jets and heavy lift aircraft.

This represents a new way of working under which they are measured and paid on results and outputs, not inputs, improving long-term planning, providing better visibility and delivering considerable savings to the MOD. The award complements a £13M contract to assist the MOD in bringing the Delta Test variant of the A400M Atlas into UK service, and a £5M contract to evaluate flight control system upgrades to Boeing’s Chinook helicopter.

In international markets, the business was awarded a five year extension to the contract under which it manages and assists in the delivery of training at the Swedish Flight Physiological Centre. It is also developing the gridded ion engine electric propulsion systems for the flight module to be used on the ESA’s BepiColombo mission to Mercury. Significant resources are being deployed by all parties to ensure the mission meets the planned launch date in 2018. The business delivers turnkey services for customers using Remotely Piloted Air Systems to meet growing demand, particularly from international organisations such as the UN. Following the opening of the Snowdonia Aerospace Centre in Wales, it demonstrated the use of RPAS in tackling environmental issues in a project for the Welsh Government.

The Maritime, Land and Weapons business was created in April 2016. During the year, in the weapons domain, the business was awarded a new research framework contract for trials, testing and analysis in cyber and electronics warfare, a five year contract to provide advice to the MOD on military batteries and a four year contract to provide advice to NATO.

In October the business led a team from across the group to deliver an international at sea demonstration at the Hebrides range, the largest in Europe. The exercise attracted nine ships from eight nations, culminating in the first ever launch of a ballistic rocket into space from the UK and its subsequent engagement by an SM3 missile launched by a US guided missile destroyer. As a result, the business is now pursuing opportunities for further combat scenario training and inter-operability testing involving customers from many nations. It also undertook testing of the latest helicopter-borne IR threat warning system in live rocket and gunfire scenarios.

The Maritime Land & Weapons business was awarded a new contract to deliver acceptance trials for the new MARS class tankers. The business also resolved urgent operational issues to enable ships to deploy and be effective in theatre including improving the hydrodynamic efficiency of Type 23 frigates by optimising the design of the propeller and hull, enabling the Royal Navy to realise potential fuel savings across its fleet. It also delivered a container-based system for close-in defence against Fast Inshore Attack Craft, offering a new solution for the self-protection of support ships.

The business is pursuing selected growth campaigns with a focus on emerging technologies such as autonomous systems. During the year it won a number of autonomy-related contracts, including support to the Royal Navy to deliver the unmanned warrior exercise in October which will demonstrate the use of autonomous systems in a wide range of scenarios. The group’s role also includes the delivery of a containerised command system to control multiple unmanned systems.

In Cyber, Information and Training, although competition is fierce, the SDSR and the focus on counter-terrorism are likely to drive increased in budgets for C4ISR and cyber security. The CIT business is the MOD’s leading supplier of C4ISR research, maintaining its research revenues during the year and winning new work to improve information systems for deployed headquarters. During the year the business was awarded a position with Northrop Grumman on a seven year framework contract to deliver cyber security support to the UK Government. It also won a contract with Motorola Solutions to provide monitoring, assessment and assurance services in support of the delivery of the UK Emergency Services Network.

Outside its traditional markets, CIT is providing advice to regional and local government customers on innovation initiatives to support local business growth, and is delivering training and simulation services to customers in North America, Europe and the Middle East. Finally the business is providing secure receiver processing for the encrypted Public Regulated Service on the Galileo constellation of satellites, the EU version of GPS, which goes live in 2017. During the year it launched a new receiver that will utilise the PRS service for use by governments, the military and emergency services across Europe.

The International business was established in April 2016 and includes QinetiQ Australia as well as Advisory Services. The Australian business agreed with the Australian DoD the renewal for up to 15 years of the Aircraft Structural Integrity services contract for a minimum contract value of A$21M, which supports the airworthiness of military aircraft. Building on its strong record in the UK, the Advisory Services business won a major contract to provide early stage advice and business case support to a Middle Eastern client for a complex engineering project.

The operating profit in the Global Products division was £15.1M, a decline of £3.2M when compared to last year, impacted by a reduction in income from the oil and gas sector along with the completion of certain programmes in the prior year. Orders grew 8% to £164.4M as a result of a new pipeline contract for OptaSense and due to improved order flow in North America. As a result, the division had 64% of its 2017 revenue already under contract at the beginning of the new financial year compared to 61% at the same time last year.

The performance of QinetiQ North America improved during the year as it adapted to a defence funding environment that has shifted markedly from the overseas contingency operations associated with Iraq and Afghanistan. The business is the world’s leading provider of military robots and activity during the year focused on the reset and recapitalisation of robots previously used on operations and the upgrade of systems with new capabilities such as the detection of chemical and biological weapons etc. At the same time the business is preparing for multi-year programmes of record which will be funded out of the Department of Defence’s base budget.

During the year the business announced a contract win valued at $16M from General Atomics in San Diego to deliver control hardware and software for the Electromagnetic Aircraft Launch System and the Advanced Arrested Gear to be installed on the Navy’s next aircraft carrier, the John F. Kennedy. It was also awarded orders for survivability products for both US and international customers, with demand for air and ground armour increasing in the year.

During the year Jamie Pollard was appointed to be OptaSense’s CEO after more than twenty years running large global businesses within Schlumberger. Although growth in the upstream oil and gas market has been constrained by the low oil price, the product development agreement with Shell continues to deliver significant technical progress and a fourth generation OptaSense system was launched in the year. The business also signed a strategic market agreement with Weatherford, and oil and gas service company with a presence in every major oil and gas region of the world. The partnership will deliver enhanced data acquisition and monitoring of seismic activity, well construction, completion and fracture operations, and production flow.

The business continues to make progress in infrastructure security, winning a contract with a partner to deliver the world’s largest distributed fibre sensing project for the Trans-Anatolian Natural Gas Pipeline. The total contract value is more than $30M, of which about half has been contracted with the group and will cover the protection of over 1,850km of pipeline. The business also won a contract to monitor a further 500km of gas pipeline in India. At the end of September, the business completed an 18 month development project with Deutsche Bahn, which concluded that DAS technology has the potential to significantly reduce the cost of sensing in the rail industry. It also won a contract with a Class 1 US railroad operator to deliver a software platform in preparation for a wider rollout of DAS technology.

The Space Products business delivered several projects in the year. In March, the ESA’s ExoMars mission was launched, containing the group’s UHF transceiver which will transmit data from the lander on the planet’s surface back to Earth via a satellite orbiting Mars. The project will pave the way for a second mission, recently rescheduled to 2020, in which a rover will spend six months analysing Mars’ environment for signs of life. The business is currently developing the computer and avionics for ESA’s Proba 3 satellites, to be launched in 2019 to study the Sun.

EMEA Products renewed a five year £10M contract to provide materials research and advice to the UK MOD. They also continued their relationship with EDF Energy for the development of stealth wind turbines. The group became the first company accredited and authorised by the French government to assess proposed wind farm impact on meteorological radars in order to speed up planning applications. Other orders received in the year included a contract with the US DARPA to develop an electric hub-drive that will improve survivability and mobility of future military ground vehicles. The contract, worth $2M with an option for a further $3M, is part of DARPA’s Ground X-Vehicle Technologies programme.

Bolden James, which provides data classification solutions to large military and commercial organisations, had a strong year and should see further opportunities following changes to EU regulations that introduce significant penalties for data classification leaks. Commerce Decisions renewed its agreement with the MOD for the provision of tender assessment and procurement support software. It also won the first contract through its Australian arm and was selected to deliver bid evaluation criteria for the Canadian Surface Combatant programme which will be used to assess warship designers and combat systems integrators.

The increase in the current tax liability is primarily due to a potential tax liability crystallising in the US following a court decision in respect of taxes payable from the group’s acquisition of Dominion Technology Resources in 2008. An insurance policy was taken out by the group at the point of acquisition and if the court’s decision is final then the funds required to settle this dispute will be provided by the insurers. Hence, an offsetting receivable is reported on the balance sheet.

There has been quite a sizeable impairment of goodwill this year. Goodwill previously allocated to the Cyveillance business of £5.2M was written off on disposal of the business. There was also an impairment of £31.9M in the US Global products division due to reducing growth rates.

Steve Wadey joined the group as CEO in April 2015 having previously been MD of MBDA UK and Technical Director for the MBDA Group.

Going forward, the UK government’s strategic defence and security review has brought clarity to key defence programmes but will require further savings to be delivered from ongoing defence transformation. For EMEA Services, in the short term there will continue to be uncertainty with the potential for interruptions to order flow. Although revenue under contract for 2017 is slightly below that of a year ago, the division’s performance as a whole is expected to remain steady this year. The Global Products division has shorter order cycles than EMEA services. At the beginning of the year, 2017 revenue under contract was slightly above that of a year ago, but the division’s performance remains dependent on the timing and shipment key orders. Overall, the board’s expectations for group performance this year remains unchanged.

At the year-end the group had a net cash position of £274.5M compared to £195.5M at the end point of last year. At the current share price the shares are trading on a PE ratio of 14.4 which increases to 14.5 on next year’s consensus forecast. After a 6% increase in the full year dividend, the shares are yielding 2.5% which increases to 2.6% on next year’s consensus forecast.

Overall then, this has been a mixed but robust year for the group. Profits increased but underlying profit was broadly flat. Net assets grew and although operating cash flow increased with plenty of free cash being generated, this was due to bigger tax rebates and lower finance costs. The MOD budget is rather constrained but the group feel this may lead to more outsourcing and opportunities. The baseline profit for single source contracts has fallen, however, which may lead to some lower profits.

In EMEA Services, profits did increase but this was entirely due to a credit received from the resolution of a historic overseas exposure with underlying profits down due to MOD budget constraints and uncertainty surrounding the single source contract changes. In Global Products, profits were down due to the subdued oil and gas market along with programme completions.

Orders did grow in this division, however. Going forward, performance is likely to remain solid but unchanged. With a forward PE of 14.5 and dividend yield of 2.6% the shares are not cheap but despite the lack of growth, this is a cash generative quality company and I hold the shares.

On the 28th June the group announced that over the past few days they had purchased for cancellation 1,144,000 shares at a cost of £2.7M. It was also revealed that CFO David Mellors is leaving to take up the same role at Cobham after spending the last eight years at the group. This is a blow as David really has created a very strong balance sheet and financial position at this company.

On the 20th July the group released a trading update covering Q1 which was in line with expectations.

Revenue under contract in the EMEA services division is similar to the position a year ago and is anticipated at this stage in the financial year, despite some continued de-scoping and delay to orders. During the quarter, the division won three orders for engineering support to the Wildcat, Apache and Tornado aircraft. These projects are to be delivered under the Strategic Enterprise Agreement with the MOD.

The UK’s defence and security review will require further savings to be delivered from ongoing defence transformation and in the short term there will continue to be uncertainty and the potential for interruptions to order flow. Despite this, the division’s performance as a whole is expected to remain steady this year.

In Global Products, 2017 revenue under contract continues to be slightly better than last year but the performance of the division remains dependent on the timing and shipment of key orders.

The next scheduled triennial valuation of the defined benefit pension scheme is due at the end of June 2017 and the recent fall in gilt yields, if sustained, would impact the measurement of scheme liabilities. Of the £50M share repurchase announced in November, £37M is still to be completed with the buyback due to be complete by the end of 2016.

Overall, expectations remain the same but there do seem to be some near-term issues to contend with. Despite this, I continue to hold.

On the 1st August the group announced that non-executive director Lynn Brubaker purchased 12,000 shares at a value of £27K.

On the 27th September the group announced that David Smith has been appointed as CFO. He is currently CFO of Rolls Royce and has previously been CEO of JLR so he seems like a decent appointment.

On the 29th September the group released a trading update where the board maintained its expectations for group performance this year. EMEA Services has continued to perform as set out in the last update. Revenue under contract in the division is similar to the position a year ago and as anticipated at this stage of the year. The global products division has shorter order cycles and more lumpy revenue profile than EMEA services but 2017 revenue under contract remains slightly better than last year, although its performance remains dependent on the timing and shipment of key orders.

The recent fall in gilt yields, if sustained, would impact the measurement of group defined benefit pension scheme liabilities, which is something that should be taken into account. A £50M share repurchase was announced last year and £21M remains to be completed, expected to be done by the end of 2016.

On the 30th September the group announced that it has signed an 11-year £109M contract extension with the MOD to continue to develop and de-risk Royal Navy mission systems and infrastructure through integration and testing at Portsdown Technology Park, Portsmouth. The renewal of the Naval Combat Systems Integration Support Services contract, fist signed in 2012, secures the site’s future. Operating in collaboration with the Royal Navy, DE&S and BAE Systems, the contract will be accompanied by QinetiQ investment to modernise the facilities, equipment and ways of working at the site to improve services to the MOD and attract new customers.

All this sounds fairly OK, although the reliance on key contract timings sounds a bit iffy to me.