QinetiQ has now released their final results for the year ended 2018.

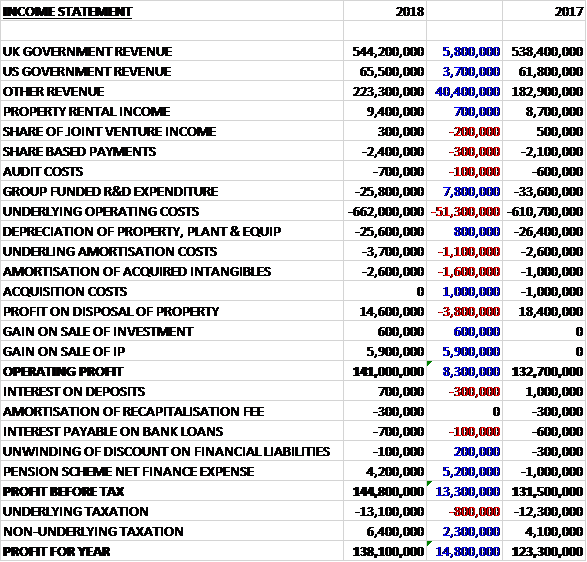

Revenues increased when compared to last year with a £5.8M growth in UK government revenue, a £3.7M increase in US government revenue, a £700K growth in property rental income and a £40.4M increase in other revenue. Group funded R&D expenditure increased by £7.8M but share based payments increased by £300K and other underlying operation costs were up £51.3M. Depreciation was down £800K but underlying amortisation costs were up £1.1M and the amortisation of acquired tangibles increased by £1.6M. There was a £3.8M fall in the profit from property sales but also a £1M fall in acquisition costs and £6.5M was made on the sale of IP and investments to give an operating profit £8.3M higher. There was a £5.2M positive swing to a net pension scheme income and tax charges declined by £1.5M to give a profit for the year of £138.1M, a growth of £14.8M year on year.

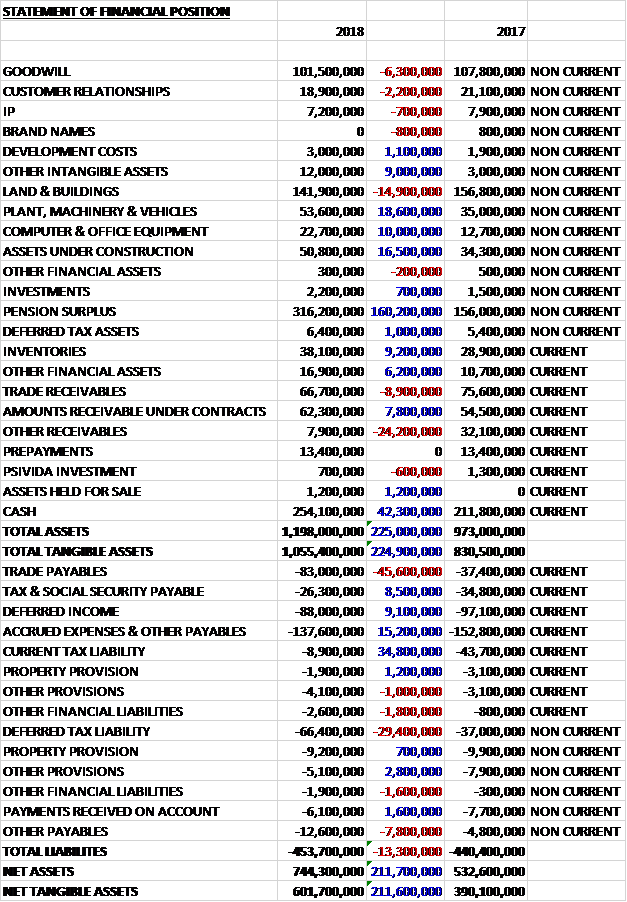

When compared to the end point of last year, total assets increased by £225M driven by a £160.2M increase in the pension surplus, a £42.3M growth in cash, an £18.6M increase in plant & machinery, a £16.5M growth in assets under construction and a £10M increase in office equipment, partially offset by a £24.2M decrease in other receivables relating to the insurance payout following the unfavourable court decision in the US, and a £14.9M decline in land and buildings. Total liabilities also increased during the year as a £34.8M decline in current tax liabilities relating to the settlement of a tax liability in the US related to an unfavourable court decision and a £15.2M fall in accrued expenses and other payables were more than offset by a £45.6M increase in trade payables and a £29.4M growth in deferred tax liabilities. The end result was a net tangible asset level of £601.7M, a growth of £211.6M year on year.

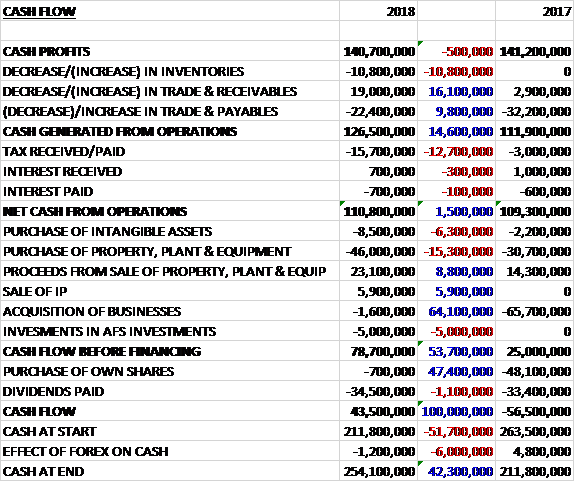

Before movements in working capital, cash profits declined by just £500K to £140.7M. There was a cash outflow from working capital but this was lower than last time so even after tax payments increased by £12.7M the net cash from operations was £110.8M, a growth of £1.5M year on year. The group spent £8.5M on intangible assets, £46M on fixed assets, £5M on available for sale investments and £1.6M on acquisitions. Offsetting this the group brought in £23.1M from the sale of fixed assets and £5.9M from the sale of IP to give a free cash flow of £78.7M. Of this, £34.5M went on dividends to give a cash flow of £43.5M and a cash level of £254.1M at the year-end.

Capital expenditure increased from £32.9M to £80.4M to support the development and modernisation of capabilities for long-term UK MOD contracts and expansion into high growth international markets. Capex is expected to be in the £80M to £100M range in 2019 with the capex associated with the LTPA recovered in full under existing LTPA contract terms.

The operating profit in the EMEA Services division was £94.3M, a growth of £1.6M year on year. Orders for the year were down £165M to £355.9M due in part to the award in the prior year of the £109M Naval Combat System Integration Support Services contract and £55M of Strategic Enterprise contracts. Excluding this there was slower H1 orders offset in part by stronger order performance in H2. Revenues increased by 4% on an organic basis driven by the International and Maritime, Land and Weapons businesses.

At the start of 2019, 75% of the division’s revenue was under contract compared to 79% at the start of last year which reflects the lower value, shorter dated orders in 2018 and an increasing international mix in the business. The increase in profit was due to a number of one-off items including a £5.3M credit relating to the release of engine servicing obligations, a £4.7M credit related to settlement of a contractual dispute, a £2.7M charge relating to property liabilities and a number of other contract related releases. Excluding these, profits fell by £3.4M due to the lower baseline profit rate single source contracts, in line with expectations.

The baseline profit rate which applies to pricing discussions is a three year rolling average so whilst the input rate for 2019 increased from 6.44% to 7.94% the rolling average fell from 7.46% to 6.81%. The impact of changes to the single sourcing pricing regulations is expected to intensify this year with the anticipated repricing on the remainder of the LTPA representing a headwind of around £6M to operating profits in the division.

In the Air and Space business the group is building on the investment made as part of the 2017 amendment to the LTPA in test aircrew training and have begun marketing the new enhanced offer which uses their new aircraft and syllabus. In November they signed the first multi-year contract with the Royal Netherlands Air Force for £6M and have subsequently signed a contract with Armasuisse which is responsible for defence procurement in Switzerland, and are in close dialogue with a number of other potential customers.

The business completed the implementation of Strategic Enterprise, securing customer endorsement and achieving dull operating capability, a major milestone under the contract. Strategic Enterprise has been a significant achievement for the group with over £250M of orders placed under the framework. The group have been invited by the MOD to negotiate the Engineering Delivery Partner programme on a sole source basis through which the MOD will procure its engineering services which the group will deliver with Atkins and BMT.

The business continues to deploy significant resources to develop the gridded ion energy electric propulsion system to be used on ESA’s BepiColombo mission to Mercury which is scheduled to launch in October 2018, and the module has now been shipped to the launch site. Technical qualification for the propulsion system needs to be completed and accepted by the customer before approval can be given to launch.

In the Maritime, Land and Weapons business the investment in the air ranges they are making as part of the 2017 amendment will allow the group to deliver more complex trials. Using their facilities at MOD Aberporth, they worked in partnership with the MOD and MBDA, the manufacturer of the Brimstone 2 missile, to provide the capability assurance required to ensure the missile can be integrated onto Typhoon.

In January they won an order from a key international customer to perform submarine research, modelling and testing and as part of an ongoing programme of work they provided test and evaluation services on the escape systems of the new class of submarines being built for the Italian Navy. In addition they are leading a new framework programme providing the UK MOD with access to key industry, academia and SME expertise.

The business is working with MBDA and the MOD to develop a new joint UK energetics strategy. As part of this, they have secured a significant contract for weapon test and evaluation and completed the refurbishment of an Environmental Test Centre. Following the delivery of the Dragon Fire design review, the MOD has agreed to place the second year of funding with the Dragon Fire consortium which the group provides with high energy laser source expertise.

In the Cyber, Information and Training business, orders were lower than last year due to fewer research related orders from the UK MOD. The business is focused on bidding and winning more transformational deals with new customers. Major deals being bid for include work for client side support for BATCIS with an estimated contract value of between £50M and £95M, the new Defence Operational Training, synthetic training environment and continuation of the Rockwell Collins partnership for the next generation of position, navigation and timing receivers.

The business is bidding for Serapis, the replacement for the MOD’s current communications and information systems R&D framework run by the group. During the period they were awarded a £4M consultancy contract to the UK Space Agency utilising their experience in satellite communications. They have developed a cyber test and evaluation service to enable organisations to test and rehearse cyber defence scenarios to better understand vulnerabilities and responses to them. Finally, they are responding to customer needs and building a new capability hub in Lincoln to address new requirements for the Electronic Warfare community based around RAF Waddington.

In the international business, the year marked a significant one in Australia. Overall record orders were complemented with significant contract wins and an increase in revenue of around 30%. They were awarded their second test and evaluation facilities operations contract in Australia to run the mine warfare maintenance facilities in Sydney. They achieved an A$16M increase in their contract under AIR7000 to provide support relating to the procurement of maritime patrol aircraft in Australia. The group, as part of a consortium led by Nova Systems, has been selected by the Australian DoD as one of four Major Services Providers enabling it to bid for larger strategic contracts.

The Advisory Services business increased its international consulting contract wins and entered a number of new Middle Eastern and European countries. As a result the business doubled the size of its order intake in the year. In Sweden, they secured three new international customers at their Flight Physiological Centre that they operate on behalf of the Swedish FMV. The centre also conducted its first space mission training.

The operating profit in the Global Products division was £28.2M, an increase of £4.6M when compared to last year. Orders increased from £154.4M to £231.3M, including more than $50M of orders for maritime systems in the US and a $25M spacecraft docking mechanism order from the ESA. The division had 51% of its revenue for 2019 under contract at the beginning of the year compared to 55% at the same point of last year reflecting the shorter contact cycle of the division and an overall increase in expected revenues.

Revenue was up 7% driven by the impact of Target Systems. Like for like revenues declined by 4% due to lower robot sales. Despite this, like for like profits were up £2.7M due to improved profitability at Opta Sense and high margins in the QTS business in Q4.

In the North American business the group were unsuccessful on the US DOD’s Man-Transportable Robotic System program of record. Despite this they are well placed for the remaining programmes and were selected as one of two suppliers for the EMD phase of the Common Robotic System programme of record. The EMD will last round ten months during which time the DOD will test and evaluate robots from the two suppliers. The total budget for the programme is approximately $400M over seven years.

They secured over $20M of orders for Talon robots and more than $20M of orders for their Q-Nets and Armor products. They won a total of more than $50M of orders for maritime systems in the US including for aircraft launch and recovery equipment for the new class of aircraft carriers.

The performance of the OptaSense business improved as they saw the impact of returning confidence in the oil field market and its diversification into adjacent markets started to reap rewards. The business has made multiple significant deliveries to infrastructure customers during the year. The largest single system awarded has been delivered to Turkey, they have had significant deliveries into the Middle East and the first significant award and first phase delivery into the US. Oil field activity in North America continues to increase while the adoption in the Middle East and Asian markets becomes more embedded.

In the Space Products business, during the year they were awarded a €25M contract from the ESA for their International Berthing and Docking Mechanism. They are engaged in discussions with other potential users of the system both in the commercial and government sectors for the supply of docking modules, potentially creating a new revenue stream for the business. They secured a €3M contract with the ESA for the prelim design activities on the Altius earth observation satellite which will study the distribution of ozone in the stratosphere. The business also secured a number of new contracts, the most significant of which was COLIS, a €6M project to build a Colloid Light Scattering instrument for investigating the effect of density and temperature on colloidal structures.

In the EMEA Products business, the performance of Targets Systems, which was acquired in December 2016, continued to exceed expectations. During the year it won work from two new customers, the Korean Air Force and the Japanese Self Defence Force. It was also awarded a five year framework for the Dutch Navy for the majority of its maritime targets in addition to as long term framework with the US Targets Management Office. The business reached its production milestones with its Hammerhead and Banshee targets.

The business is supporting the Canadian government with trials of their counter-UAV system Obsidian which tracks drones. The group are collaborating with Isotropics in the development of electromagnetic lenses for use in electronically steered flat panel satellite antennas. This technology enables high throughput satellite comms in the growing areas of communications on the move and consumer broadband. They are also launching their new iridium based phone for military, emergency services and users working in challenging environments such as oil and gas or mining.

Headwinds in the UK come from the lower baseline profit rate set by the Single Source Regulations Office which made for a tougher trading environment in the year. This headwind is expected to intensify in 2019 with the anticipated remainder of the LTPA which was not part of the December 2016 amendment but it should moderate in 2020 enabling growing revenue to deliver increased profitability.

After the year-end the group entered into an agreement to acquire EIS Aircraft Operations for €70M. The business is a provider of airborne training services based in Germany, delivering threat representation and operational readiness for military customers. It generated €5.4M EBITDA last year and the legal approvals are expected to close towards the end of H2 2019.

Priorities for 2019 include the repricing of the LTPA with UK MOD, accelerate international growth and continue investment driving sustainable growth. Going forward with more than two thirds of 2019 revenue under contract they enter the year in a position of strength and are maintaining expectations for group performance. The board expect the global products division to make continued progress with further organic growth partially offset by a translational impact from forex.

At the current share price the shares are trading on a PE ratio of 14.3 which increases to 16.1 on next year’s consensus forecast. At the year-end the group had a net cash position of £266.8M compared to £221.9M at the end of last year. After a 5% increase in the total dividend the shares are yielding 2.3% which remains the same on next year’s forecast.

On the 25th July the group released a trading update covering Q1 2019 which was as expected with no change to expectations for group performance for the year. The EMEA services division continued to deliver against their growth strategy, increasing both revenue and orders organically. Revenue under contract is in line with expectations for this point in the year.

The division on the competition for the Battlefield and Tactical Communications and Information Systems contract worth up to £95M over five years. This is the largest competitive win since the implementation of their new growth strategy. They won a five year contract to build and maintain a synthetic environment to provide test and reference services for a new ground based air defence system; and with their partners Atkins and BMT they have been confirmed preferred bidder by the MOD for the Engineering Delivery Partner programme.

The global products division has continued to grow orders and revenues organically. The North American business delivered a good performance driven by demand for their robots and survivability products. Following its integration the Target Systems business has continued to grow and is leveraging wider group capability to enhance its portfolio. It reached a significant milestone in the development of a new supersonic aerial target and won its first orders for an enhanced Banshee aerial target from a Scandinavian customer.

On the 18th October the group confirmed the completion of the EIS Aircraft Operations business.

On the 22nd October the group announced the acquisition of 85% of Inzpire Group with an agreement to acquire the remaining 15% after two years for a total consideration of £23.5M. The business has a five year track record of consistent revenue growth and is expected to deliver £2M of EBITDA this year.

The business is a provider of operational training and mission systems for military customers. Around 75% of its revenue comes from airborne training and evaluation services, primarily for the RAF. The balance of revenue is from the sale of aviation mission system products ranging from standalone tablets to full mission support systems integrated with aircraft avionics.

Overall then this has been a bit of a mixed year for the group. Profits were up but this was mainly due to the sale of IP, financial gains from the pension scheme and one-off tax income. Excluding this, there was a modest rise. Net assets grew strongly and the operating cash flow improved, although this was entirely due to working capital movements and cash profits fell ever so slightly. Still, a decent amount of free cash was generated.

The EMEA Services division saw profits increase due to one-off items. Excluding this, there was a decline due to the lower baseline profit rates on single source contracts, which will only intensify in the coming year. Global products seems to be doing fine, boosted by increased profitability at OptaSense and QTS. The coming year will probably be quite difficult but once the baseline profits are sorted for the single source contracts, the rest of the business seems to be doing well. At some point these shares could be a decent buy but with a forward PE of 16.1 and yield of 2.3% they look a little expensive at the moment.