QinetiQ has now released its interim results for the year ending 2017.

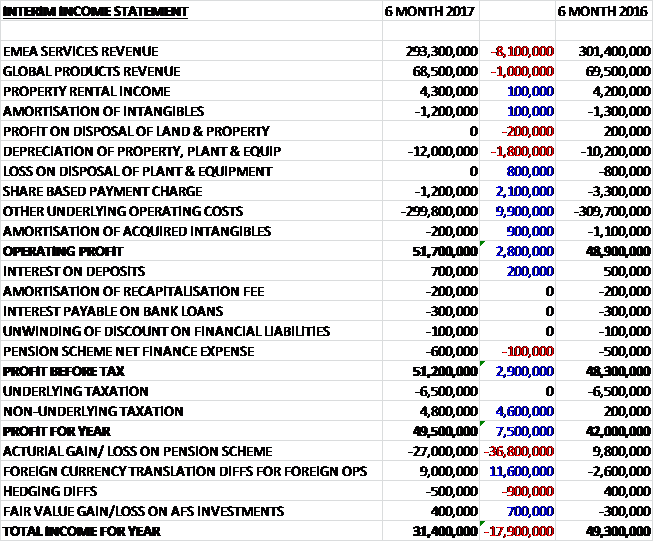

Revenue declined when compared to the first half of last year due to an £8.1M decline in EMEA services revenue due to the lumpy nature of revenues and a £1M fall in global products revenue. Depreciation increased by £1.8M but share based payments fell by £2.1M, amortisation of acquired intangibles decreased by £900K and other operating costs fell by £9.9M to give an operating profit £2.8M above that of last time. Underlying tax remained steady but non-underlying tax receipts increased by £4.6M to give a profit for the period of £49.5M, a growth of £7.5M year on year.

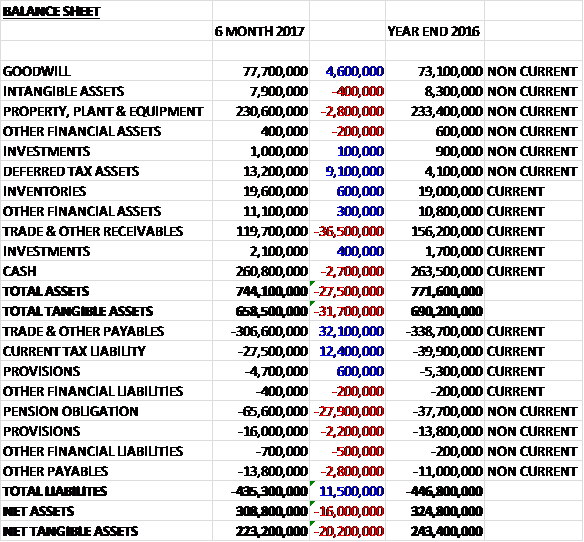

When compared to the end point of last year, total assets declined by £27.5M driven by a £36.5M fall in receivables, a £2.8M decrease in property, plant and equipment and a £2.7M reduction in cash, partially offset by a £9.1M increase in deferred tax assets and a £4.6M growth in goodwill. Total liabilities also declined during the period as a £32.1M decrease in payables and a £12.4M fall in current tax liabilities was partially offset by a £27.9M increase in pension obligations, a £1.6M growth in provisions and a £2.8M increase in other payables. The end result was a net tangible asset level of £223.2M, a decline of £20.2M over the past six months.

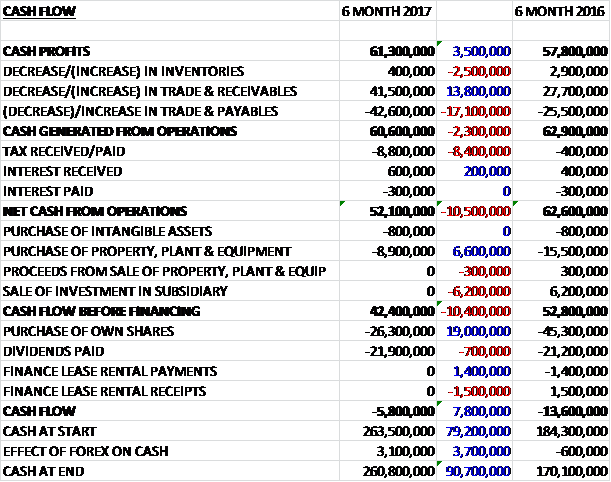

Before movements in working capital, cash profits increased by £3.5M to £61.3M. There was a modest cash outflow from working capital compared to an inflow last year but tax payments increased by £8.4M to give a net cash from operations of £52.1M, a decline of £10.5M year on year. The group spent just £8.9M on tangible assets and £800K on intangible assets to give a free cash flow of £42.4M. This was used to pay dividends of £21.9M and £26.3M was spent on buying back shares which meant there was a cash outflow of £5.8M during the period and a cash level of £260.8M at the period-end. Capital expenditure is expected to increase in future as the group invests in the LTPA and other long-term contracts.

In the UK in the short term there may continue to be some uncertainty and the potential for interruptions to order flow. The SSRO is developing a new methodology for calculating the baseline profit rate in future years, potentially introducing multiple profit rates. This baseline rate acts as the starting point for agreeing the profit rates of new and renewed contracts, and suppliers can both under or over perform the contracted rate. About 70% of the total EMEA Services revenue is derived from single source contracts, including the non-tasking element of the Long Term Partnering Agreement and they anticipate that the majority of their single source revenue will fall under the regulations within the next three years.

The underlying operating profit in the EMEA Services division was £43M, a growth of £300K year on year. Within air and space, the business is continuing to work in partnership with the MOD and the supply chain to deliver the Strategic Enterprise model which transforms the provision of aircraft test and evaluation and which has now been in place for a year. The model represents a new way of working under which they are paid on results and output rather than input. Under this model, contracts totalling £20M were won in the period to provide in-service support for Apache and Puma helicopters, as well as Tornado jets, and test and evaluation services for the Wildcat Future Air to Surface Guided Weapon programme. Since the end of the first half, the business has won a contract to provide safety advice for the Merlin helicopter programme under the Strategic Enterprise Model.

During the period the group secured £2M of research funding to lead a group from industry, academia and SMEs to upgrade the scale models used in the Farnborough wind tunnel using technology adapted from F1, leading to improved efficiency and increased capacity. The business also revealed a new material, Titan Weave, that will help reduce the weight of aircraft, while being three times stronger than current materials used to protect against bird strikes and other impacts.

In October, as part of its ExoMars mission, the ESA attempted to place its lander of the surface of Mars, equipped with a QinetiQ-built transceiver responsible for transmitting data back to earth. The lander was lost, but the transceiver operated successfully, providing data that helped scientists to understand what happened to the spacecraft in its final moments. The business also continues to deploy significant resources to develop the gridded ion engine electric propulsion system for the flight module to be used on ESA’s BepiColombo mission to Mercury.

The Maritime, Land and Weapons business was awarded an eleven year contract extension with £109M for the Naval Combat Systems Integration and Support Services based at Portsdown Technology Park.

In the weapons domain, the business won an £8M contract to implement and evaluate vehicle survivability for Dstl, including installing a Soft-Kill Defensive Aids System on a Challenger 2 Tank, international customers continue to want to use the group’s expertise for their own development, with the South Korean Agency for Defence Development committing to a £3M programme to test their latest warhead designs using the Long Test track at MOD Pendine.

In October, the Maritime, Land and Weapons business led a team from across the group to deliver Unmanned Warrior for the Royal Navy, a demonstration by 40 companies of how autonomous vehicles under the water, on the surface and in the air, can be used for future operations such as mine hunting. International delegations from the US, Canada and Australia visited the demonstration alongside senior MOD and UK Government Ministers. Next year, building on Unmanned Warrior and At Sea Demonstration 2015, another international exercise will be taking place at MOD Hebrides, Formidable Shield 2017.

In Cyber, Information and Training, although competition is fierce, the SDSR and the focus on counter-terrorism are likely to drive increases in budgets for C4ISR ad cyber security. The business was awarded an Open Source Intelligence contract to help customers keep pace with the rapidly evolving technical and social media landscape.

The business is continuing to see interest from regional and local government customers on initiatives to support local business growth, and is delivering training and simulation services to customers in North America, Europe and the Middle East. During the period they secured a number of contracts worth a total of £10M for secured navigation, working with the European GNSS Supervisory Authority to help enable the effective exploitation by users of Galileo – the European version of GTS which goes live in 2017. This included the first demonstration of accessing the encrypted Public Regulated Service via the cloud. The business is also working on collaboration with Lloyds Register to improve the security on board cyber-enabled ships.

QinetiQ Australia secured more than $30M of wins. These included support to tanker aircraft, the AP-3C Orion replacement, Navy guided weapons systems, ground-based air defence, the Australian Artillery Regiment, and a contract to extend the provision of technical advice at munitions manufacturing plants. The business also gained accreditation from Australia’s Defence Aviation Safety Authority to approve structural changes on all Australian Defence Force aircraft, building on its Aircraft Structural Integrity services contract which supports the airworthiness of military aircraft.

The Canadian business is recently established but has already secured cost engineering and award procurement software contracts. Additional consulting contracts are being pursued and the business is being positioned, through prime contractors and potential partners, for strategic campaigns. The advisory services business is delivering a major contract to provide early stage advice and business care support to a Middle Eastern client for a complex engineering project.

The underlying operating profit in the Global Products division was £8.9M, an increase of £1.8M when compared to the first half of last year, assisted by a credit of £1.3M relating to the resolution of an overseas licensing dispute. Orders grew from £57.6M to £92.5M mainly due to improved order flow in North America, in particular $28M of orders for next generation US aircraft carriers.

Excluding £4.5M of forex variance, there was an 8% decline in the organic revenue primarily due to lower robot shipments in the period and illustrating the lumpy nature of the revenue profile. At the beginning of the second half of the year, the division had 98% of its 2017 revenue under contract compared to 81% at this point of last year, although the delivery of this is dependent on the timing of the shipments in the remainder of the year.

In North America the period saw a strong orders performance, driven by awards in robotics, air and ground armour, R&D, and in particular for Advanced Launch and Recovery Equipment for US aircraft carriers. The ALRE equipment includes control hardware and software for the Electromagnetic Aircraft Launch System and the Advanced Arresting Gear to be installed on the next generation of US aircraft carriers. Demand for the reset and recapitalisation of robots previously used in operations has remained high, as has demand for capability upgrades such as detection of CBRNE.

The business is also positioning for multi-year programmes of record that will be funded out of the DoD’s base budget. Through both internal and external funding, QNA has added to the capability and strategic relevance of its robotic fleet, especially for the Talon family of robots, its flagship mid-sized offering. In October 2016 it announced a strategic partnership with the Estonian company Milrem for Titan, a modular, hybrid military unmanned ground vehicle for dismounted troop support.

Outside of robotics, the business launched in September a new meteorological product, iQ-3, that provides real-time atmospheric data in support of military requirements such as artillery fire support, tactical weather modelling and air drop. Its Line Watch product, which accurately measures the current and voltage of power distribution lines, is being piloted by ten North American utility companies.

Optasense is a distributed acoustic sending business. It continues to make progress in infrastructure security, delivering ahead of schedule on the world’s largest distributed fibre sensing project for the 1,850km Trans-Antolian Natural Gas pipeline that frons from Azerbaijan to Europe. Following the establishment of an advisory board to provide expertise in key target markets, the business has signed an agreement to work together with Siemens to pursue new opportunities in the rail sector. The business is also undertaking collaborative research with Stanford School of Earth, Energy and Environmental Sciences in California that includes the installation of a fibre-optic seismic array on the Stanford campus to better understand the complex geology of the Bay Area.

In Space Products, during the period the group’s P200 satellite was listed in the NASA catalogue which will help aid the procurement of spacecraft by US federal agencies. The business also won a $2M contract with the ESA to develop the next generation computer and power management for the Proba series of satellites.

In EMEA Products, during the period the US DARPA invested a further $3M in the group’s electric hub-drive technology that will improve mobility and survivability of future military ground vehicles. The new agreement builds on previous contract awards and will take the technology from concept design to the building and testing phase, including the production of two fully working units.

Internationally, ASX airborne surveillance products have been delivered and there has been further interest in wind farm radar impact assessments to help secure planning permissions in Europe and other regions including South Africa. Following the development of advanced materials for the Department of National Defence in Canada, the UK MOD has no placed an order for similar equipment as a technology demonstrator for the Royal Navy.

In November last year the group were awarded a £153M Strategic Enterprise contract that changed the way they deliver aircraft engineering services for the MOD to an output-based model where they are paid and measured on deliverables. In the first half of this year they added £20M of additional work into this model so they are now providing engineering services for nine aircraft types, both fixed and rotary wing. There are further opportunities to expand this contract, working with partners to pool skills and bring collaborative teams together across industry.

At the end of September they signed the 11 year, £109M contract extension for Naval Combat System Integration Support Services to the MOD, under which they lead the T&E, integration and development of mission systems that keep the UK’s warships at sea. This is an example of the focus on partnership within their customers and across the broader supply chain as they look to develop their Portsdown Technology Park site as the UK Centre of Excellence for maritime mission systems for the whole supply chain. While not delivering increased revenue in the short term, the extension of this contract for eleven years improves the security of future revenues and provides a platform to win incremental work.

Further work is underway with the Front Line Commands and prime contractors to develop the future vision for UK T&E to ensure it meets the needs of the UK defence plan, supports exports and international partnerships, and delivers the right outputs to enable future military capability.

In September 2016 the MOD announced that it was finalising the agreement of a £30M contract with UK Dragonfire, a UK industrial team led by MBDA and including QinetiQ, to conduct the Laser Capability Demonstrator Programme that will deliver a step change in the UK’s capability in high energy defensive laser weapon systems. Once under contract the group will provide the high-powered laser technology for this programme and conduct trial engagement of land and maritime targets that are due to take place at the ranges that they manage under the LTPA in 2019.

In July, QinetiQ, Thales and Textron AirLand announced that they will partner to bid for the MOD’s Air Support to Defence Operational Training programme. The team will propose a service using the Textron AirLand Scorpion jet equipped with Thales and QinetiQ sensors to train all three armed services. The competitive contract is expected to be awarded in September 2018 with a service delivery start in January 2020, and is expected to be worth up to £1.2BN over fifteen years. The group will provide the safe operation of aircraft – including maintenance, provision of pilots, and certification, as well as the integration of sensors, jamming pods and synthetic training capabilities.

During the period, a deferred tax asset of £4.1M has been recognised in respect of unused tax losses (£22M) expected to be utilised in the foreseeable future. The group also has current tax liabilities of £27.5M which decreased considerably during the period partly due to part settlement of a tax liability in respect of taxes payable in respect of the group’s acquisition of Dominion Technology in 2008. The funds required to make this part settlement were recovered from the vendors of Dominion (which had been included as a receivable). An insurance policy was taken out by the group at the point of acquisition and if the Tax Court’s decision is upheld, the funds required to fully settle this dispute will be provided by the insurers so an offsetting receivable for the residual balance is reported on the balance sheet.

The group bought back £29M of the previously announced £50M share repurchase by the period-end and they expect to complete the rest in the second half of the year.

As previously announced, CFO David Mellors will leave the group in December to become CFO of Cobham and will be replaced by David Smith, current CFO of Rolls Royce. He will be in the post no later than the start of March.

The group expect to pay about £7M in the second half relating to a court order over a very old overseas dispute over a contract signed in 2005. This payment, fully provided for in the accounts in prior years, must be made even though the group expects to make a court appeal.

Going forward, in 2017 the UK government’s strategic defence and strategic review, together with ongoing defence transformation, are expected to continue to have an impact on the UK defence market. This will provide future opportunities for EMEA Services to build on its strong record of delivering more for less, while recognising that there may continue to be some uncertainty and the potential for interruptions to order flow. At the end of September, revenue under contract for 2017 was in line with the prior year, and the division’s performance as a whole is expected to remain steady this year.

The Global Products division has shorter order cycles than EMEA Services. At the end of the period, 2017 revenue under contract was above that of a year ago, but the performance of global products remains dependent on the timing of shipments of key orders. Overall the board’s expectations for group performance this year remain unchanged.

At the period-end the group had a net cash position of £260.8M compared to £263.5M at the end of last year. At the current share price the shares trade on a PE ratio of 16.5 which increases slightly to 16.6 on the full year consensus forecast. After the interim dividend was increased by 5% the shares yield 2.2% which increases to 2.3% on the full year forecast.

On the 2nd December the group announced that it had been awarded a £1BN contract amendment to the LTPA from the UK MOD under which the Test and Evaluation services have been delivered since 2003, committing approximately half the core LTPA revenues until 2028. Under the amendment the group will modernise and operate the air ranges at MOD Aberporth and MOD Hebrides, and test aircrew training through the Empire Test Pilots’ School at MOD Boscombe Down. Efficiencies delivered through this programme will enable future MOD and QinetiQ investment in developing further Test and Evaluation services.

The MOD and QinetiQ have agreed to invest about £180M in modernising facilities, equipment and developing new ways of working as part of their wider strategy to lead and modernise test and evaluation across the lifecycle, from experimentation and research of new capabilities through to training and rehearsal of current capabilities.

On the 21st December the group announced that it has acquired Meggitt Defence Systems and Meggitt Holdings Canada from Meggitt for £57.5M. Meggitt Target Systems is an international provider of unmanned aerial, naval and land-based target systems and services for test and evaluation and operational training and rehearsal. The business is expected to generate about £28M of revenue and about £5.5M of operating profit in 2016.

The business provides target systems to about 40 countries from its operations in the UK and Canada, and performs on-site target services in fifteen of those countries. It will form part of the group’s new international business unit and will be reported within the Global Products division. The acquisition is expected to be EPS accretive in the first full year of ownership and will be financed from existing cash resources.

Overall then this has been a steady period for the group. Profits were up but net assets declined due to increased pension liabilities but although the operating cash flow declined, this was due to an increase in tax payments and a reduction in payables and the cash profits increased with plenty of free cash being generated. The EMEA services division was broadly flay but the global products division saw profits increase with particular strength in the US.

Going forward the SSRO new baseline profit rate may offer some uncertainty but the group seems to have been awarded some large contracts and with a forward PE of 16.6 and yield of 2.3% this is a solid beast, unlikely to show any exciting growth anytime soon but the steady nature of the work, backed by solid cash flows and balance sheet makes it safer than most – I continue to hold.

On the 16th January the group announced that non-executive director Paul Murray purchased 18,865 shares at a value of just under £50K which is nice to see, although not a huge amount.

On the 15th February the group released a trading update covering Q3. In December they were awarded a £1BN amendment to their LTPA with the MOD which commits about half of the core LTPA revenues until 2028.

They are already delivering against their commitment to modernise UK air ranges and the Empire Test Pilots School at Boscombe Down, including the purchase of new aircraft to meet the future training needs of test pilots and aircrew.

Also in December they completed the acquisition of Meggitt Target Systems which generates 90% of its revenue from outside the UK and forms part of the group’s international business unit. In January a consortium involving the group was awarded a £30M programme by the MOD to deliver a Laser Directed Energy Weapon Capability Demonstrator. QinetiQ’s role is to provide the high-powered laser technology for the programme and conduct trials at various ranges over land and water.

Underlying trading was as expected during the quarter. In EMEA Services, revenue under contract for the year is similar to the same time last year with resilient margins (does that means lightly lower?). The performance as a whole is expected to remain steady this year. The global products division has revenue under contract slightly ahead of this point of last year driven by improved order inflow in North America, although its performance remains dependent on the timing and shipment of key orders.

The incremental capex associated with the amendment to the LTPA contract is expected to be in the region of £10M this year. The group is completing the previously announced £50M share repurchase with £13M of the buyback remaining to date. Going forward, the board’s expectations for group performance in the current year remain unchanged from those set out at the interim results period.