Red24 has now released their interim results for the year ending 2016.

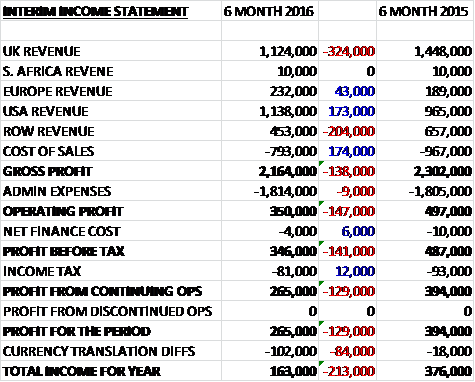

Revenues declined when compared to the first half of last year (irritatingly there is no longer a split by market sector, just geography) as a £175K increase in USA revenue and a £43K growth in European revenue was more than offset by a £324K decline in UK revenue and a £204K fall in ROW sales. Cost of sales did fall but the gross profit was £138K below that of the first half of 2015. Admin expenses were broadly flat and there was a small decline in finance costs and tax so that the profit for the half year was £265K, a decrease of £129K year on year.

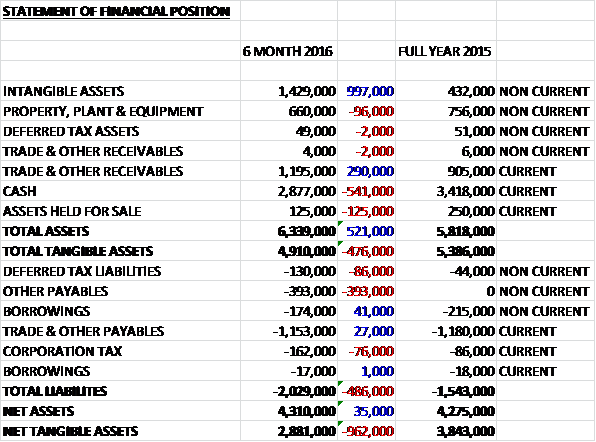

When compared to the end point of last year, total assets increased by £521K driven by a £997K growth in intangible assets and a £288K increase in receivables, partially offset by a £541K decrease in cash, a £125K halving of the value of the asset held for sale and a £96K fall in the value of property, plant and equipment. Total liabilities also increased during the period due to a £393K increase in other payables relating to deferred consideration, an £86K growth in deferred tax liabilities and a £76K increase in current tax liabilities. The end result if a net tangible asset level of £2.9M, a decline of £962K over the past six months.

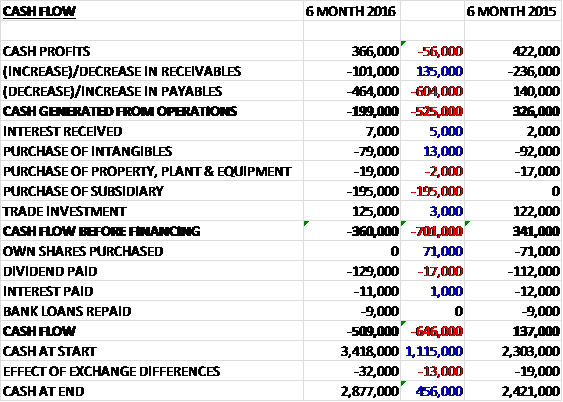

Before movements in working capital, cash profits fell by £56K to £366M. A large fall in payables meant that there was a £199K cash outflow at the operating level, a detrimental movement of £525K year on year. The group then spent £79K on intangibles, £19K on fixed tangible assets and £195K on the purchase of a subsidiary, but they did get £125K from the sale of the interest in Linx so that the cash outflow before financing was £360K. The group then paid £11K in interest and some £129K that is clearly not covered by cash flow on dividends. The end result is a £509K cash outflow for the period to give a cash level of £2.9M at the period-end.

The travel assistance service has been enhanced by the investment in the tracker product, which has placed it onto a new technical platform that will make it easier to interface with new clients and with new travel data-bases. The product was launched at the business travel show in London in February and met with an encouraging response. The board think that this will materially assist in ensuring that this revenue stream is maintained in 2016 notwithstanding the loss of business from HSBC, of which the addition of a number of new clients has replaced 75% of the lost revenue.

During the period, gaining contracts with Allianz has been a significant development and has opened a large potential market for the travel services and 2016 should see a significant increase in the travel assistance business across the globe. In October the group launched their online training platform, the red24 academy. Initial modules are aimed at the business traveller, but the platform is capable of supporting requirements across all revenue streams and suitable courses will be added as they receive external accreditation.

The special risks business had a quiet half year and dealt with few significant incidents. They continue to publish their “Treat Forecast” and have added new books of business over the year. The office they set up in Munich, primarily to service this unit, has created a number of promising opportunities and has brought on books of business with German insurers and opened sales channels to their clients.

Throughout the year, the consulting and response unit has been busy with requests for close protection work and for evacuation planning services. Last year a Far Eastern client requested a large evacuation from Libya involving several hundred of their staff which generated revenues of about £500K and was the largest project to date. This year the largest response to date has been in Nepal, following the earthquake, which produced revenue of £210K.

The product safety brand has had a busy half year and this is expected to accelerate in the second half of the year following the recruitment of a US product safety team to provide additional resource to US insurers and to provide capacity to service the business to business market there. In the summer they responded on a serious food contamination case for a manufacturer, not through an insured incident, and they believe there is significant opportunity in helping food businesses manage their product safety risks.

It seems as though the group has been unable to fully replace the lost £600K of HSBC revenues, they faced a tough comparison with a large project in Libya and last year (I wish these kinds of things were pointed out at the time) and they invested in the development of the US based product safety team along with launching Red24 Academy. This investment may hold back the results in the short term but apparently places the group on a firm growth path in the future. Apparently the good results in H2 last year were as a result of the last few months of revenue from HSBC but without the costs – why was this not made clear at the time? To add to the issues, the group also made a £100K loss on Rand/Sterling currency hedging activities during the period.

On the 1st July the company acquired RISQ Worldwide for an initial cash consideration of £259K and a deferred consideration of £371K depending on the future pre-tax profit of the business which is something to keep an eye on. The purchase generated goodwill of £584K and generated £26K in pre-tax profits in the three months since acquisition which doesn’t look too bad. RISQ specialises in employee vetting and business investigations as well as supporting the consulting and response businesses.

The board anticipate significant medium term growth in revenue from the acquisition of RISQ, from the new product safety team in the US and from the partnership with Allianz. In the short term, however, the recent investment made in the business is likely to continue to impact on the current year profitability.

After a 9% increase in the interim dividend, the shares are now yielding 2.4%.

Overall then this has been a difficult period for the group. Profits fell, net tangible assets were down and operating cash flow deteriorated – in fact there was a cash outflow at the operating level. This is mostly because of the large contract with HSBC that was not renewed as this half was the first half that it didn’t feature, which means that the second half is likely to have tough comparatives too. Additionally, the special risks division was quiet and the response division did not have a contract on the same scale as Libya evacuation last time. The product safety division and newly acquired RISQ business do seem to be performing well.

I have to say I am rather disappointed by this. I felt that the business had worked hard to replace the lost HSBC contract and must say I am rather surprised by these poor results – there was no warning about this. With a forward PE of 15.2 and a dividend yield of 3% for the full year, I don’t think the risks are fully priced in here yet. I am out.

On the 30th November the group announced a strategic contract with Hiscox whereby they provide strategic support for its product contamination insurance clients with immediate effect. They will help Hiscox’s clients prepare for risks relating to their products as well as respond to immediate crisis situations arising from product recalls and/or contamination. Support includes access to specialist technical, regulatory and PR advisors, product testing facilities and crisis communications facilities.

This seems like a decent contract to me but not sure how material it will be. I am tempted to jump back in here.

On the 3rd May the group appointed Nick Powis as Head of Operations and John Brigg as a non-executive director. Nick joins from Marsh ltd where he was Crisis Consultancy Director and Michael has been a long standing shareholder with current directorships at EMIS International and Royal & Sun Alliance Middle East.