Redrow is a UK house builder. They also have two joint ventures. They have a 50% shareholding in the Waterford Park Co in order to pursue the potential redevelopment of Watford Junction and a 50% shareholding in Menta Redrow to pursue redevelopment opportunities in Croydon.

The group is able to make land purchases on deferred payment terms. The deferred creditor is recorded at fair value and nominal value is amortised over the deferred period via financing costs. The interest rate used for each deferred payment is an equivalent loan rate available on the date of land purchase so it begs the question as to why not just take out a loan?

The group has a number different brands. Heritage homes includes traditional homes for modern living, Elegant homes are more luxury spec and focused on location, Regent is based on a townhouse designs in a suburban location, Abode has open plan urban designs where space is limited, and Bespoke involves unique designs and locations.

Redrow has now released its final results for the year ended 2015.

Revenues increased by £286M when compared to the prior year and with cost of inventories up £193M and other cost of sales increasing by £7M, the gross profit was some £86M ahead. Admin expenses also increased with growth in operating lease costs along with R&D and other expenses to give an operating profit £75M up on 2014. There was the lack of any profits from the joint ventures and interest on deferred land creditors grew along with a £12M hike in the tax charge which gave a profit for the year of £162M, a growth of £59M year on year.

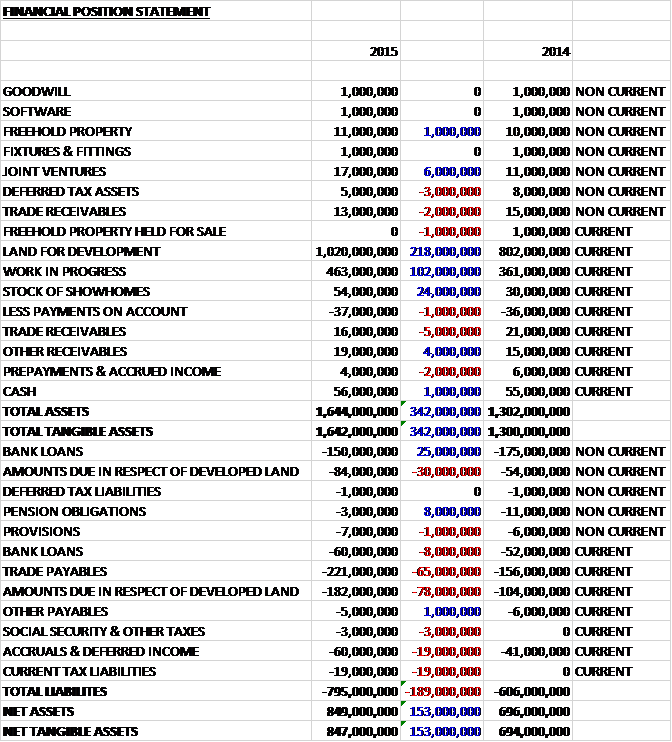

Total assets increased by £342M when compared to the end point of last year, driven by a £218M growth in land for development, a £102M increase in work in progress and a £24M growth in the stock of show homes. Total liabilities also increased during the year as a £108M hike in amounts due in respect of developed land, a £65M growth in trade payables, a £19M increase in accruals & deferred income and a £19M growth in current tax liabilities were partially offset by a £17M decline in the bank loan. The end result is a net tangible asset level of £847M, a growth of £153M year on year.

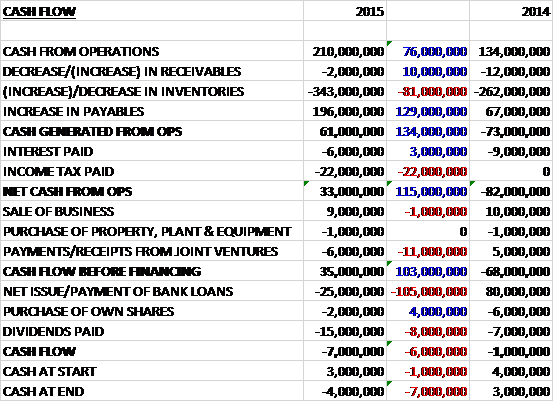

Before movements in working capital, cash profits increased by £76M to £210M. There was a cash outflow from working capital with a large increase in inventories but the overall outflow was less than last year as payables also increased considerably. After a £22M growth in tax payments as the tax-losses were used up, the net cash from operations came in at £33M, a positive movement of £115M year on year. The group then received £9M from the sale of a business, offset by a £6M payment in joint ventures and a £1M spend on capex to give a free cash flow of £35M. The group then spent £15M on dividends, £2M on buying their own shares and £25M on net debt repayments so that there was a cash outflow of £7M for the year and a cash level of -£4M at the year-end, which seems a little precarious.

The number of planning applications granted in the UK is at its highest level since 2008 and the approval rate has been maintained at the 13 year high achieved last year. Residential transactions in England and Wales increased by 14% in calendar year 2014, increasing to 1.1M. UK average prices increased by 4.1% in the year to June 2015, significantly down on the 11.5% increase observed in the prior year. These price increases were influenced by the London market where average prices grew by 7.3% in 2015 and 25.8% in 2014.

The early months of the year were tougher than in the same period of the prior year which was buoyed by the introduction of the government’s Help to Buy scheme. The scheme continues to be an attractive incentive for house buyers and accounted for around 40% of reservations for the group during the year. As the year progresses, the market improved with both sales rates and prices lifting before the election outcome brought further stability to the market with the announcement that Help to Buy would be extended to 2020.

The Central London market softened during the year in response to the threat of mansion tax, increases in stamp duty and uncertainties in the wider global economy. As a consequence the group curtailed their land buying in the “super prime” areas and focused more on sites in the outer London boroughs where demand is strong and selling prices remain affordable.

The group completed 4,022 new homes during the year, an increase of 12% over last year. Of the £1.15BN of turnover, some £65M was from the sale of commercial property, freehold reversions and land with the core housing turnover up 26% to £1.085BN due to the rise in legal completions and a 13% growth in average selling price to £270K. Gross margin improved from 21.7% to 23.8%, as 88% of the completions came from sites purchased post downturn with normal margins and as house price inflation exceeded build cost inflation, particularly in the South of the country.

The number of private apartments completed during the year increased by 24% and represented 14.8% of private sales completed, an increase on last year. Social Housing, as a consequence of the timing of delivery, reduced from 17.6% to 14.2% in 2015 but moving forward this position will be reversed and social housing is set to be a larger proportion of output, the government’s announcement regarding year on year reductions in social rents has created a hiatus that will affect the delivery of social housing in the short term.

The group continued to invest significantly in land and work in progress. They have increasingly entered into deferred terms on many of the land purchases and have also purchased more land on a subject to planning basis which has enabled them to reduce their net debt to £154M at the year-end which seems a bit of a dubious claim to me – they still have to pay up on those deferred purchases so what makes that less of a debt than the bank debt? Sounds dubious to me. In any case, the board expect net debt to increase over the next year with the ongoing investment in inventory.

Due to the roll out of the Regent and Abode brands along with apartment schemes around London, it was expected that the turnover accounted for by the primary brand, Heritage would reduce over time to about 70% and in 2015 it declined from 77% to 76%. The roll out of the Regent brand continued and it now represents 4%, up from 1.6% and there is now a number of Abode developments under construction.

During the year the group secured 5,892 new plots across 52 sites, of which 1,975 were converted from the forward land bank across 22 sites with 2016 expected to be even stronger with over 3,800 plots at Colindale and Woodford in Stockport on track to contribute. As of the end of the year the current land bank totalled 18,216 plots, a 9% increase on the previous year. The average plot cost increased from £63K to £70K, primarily as a result of a change in geographical mix of the land bank, with over 50% of plots being in the South of England compared to 44% at the end of last year. The plot cost equates to 23.5% of the current average selling price, broadly in line with previous years. The percentage of provisioned land in the land bank has now reduced to 2% and by the end of 2017 it will be zero. Despite the strengthening housing market, they group have found plenty of land opportunities within the areas that they operate.

Although the local plan process has noticeably improved since the introduction of the NPPF, the group still see the process as being too slow in some parts of the country and they state that gaining reserved matters and detailed planning consents is still taking far too long.

The group continued to experience trade shortages in some parts of the country, most acutely in new operating areas where they need to establish a base of subcontractors. As a consequence they have experienced delays that have had a knock on effect on customer satisfaction. They have also seen build costs increase during the year. Material prices have stabilised but labour costs have risen substantially and the board estimate that overall build costs have increased by in more than 5% over the past year and it is expected that this trend will continue for some time to come. It is expected, however, that any build cost increases will be more than offset by modest house price inflation.

Through “My Redrow”, a service that allows customers to tailor their homes to meet their needs, the group has managed to sell £10M of extras.

In December 2014 the group acquired a former test track and storage centre from General Motors. The 59 acre brownfield site is situated within the Bedfordshire Green Belt and has an outline planning permission for the development of up to 325 homes and a community centre. More than 30 acres of the site will be given over to open space and woodland with the remaining area creating a leafy setting for Heritage branded homes. There is also a plan for 46 affordable homes to be provided at no cost to a community trust with the rental income from those homes being used to fund a local bus service and other facilities which will benefit residents of the development. Work is scheduled to start later in the year.

Last year the group established a West Country division based in Exeter that has made a significant contribution in the year and the group recently split their business in the East to create divisions north and south of the Thames. They have also recently reorganised their London operations with London now operating as a region in its own right with two divisions initially. The Colindale Gardens division will focus entirely on delivering that highly important development. The division recently received a resolution to grant planning for 2,900 new homes and up to 100K square feet of commercial space. Under the planning agreement they will also be providing healthcare and nursery facilities, land for a new school, a significant contribution to upgrade Colindale tube station and four hectares of public open space and gardens. The project has a gross development value of over £1BN and is expected to take ten years to build. The Greater London division will oversee the other sites across the capital including the joint venture in Croydon.

As the group’s sales rates and average selling prices reach optimal levels, the future growth will rely largely on increasing the number of outlets from which they operate and expanding the divisional structure. Last year they opened 54 new outlets, and after taking into account the closure of 40, they ended the year on 117 outlets, a net increase of 14. In 2016 they expect to open around 55 new outlets, and after taking into account a higher number of closures weighted to the second half, they are forecasting to end the year on 128 outlets.

The group has a self-administered defined benefit pension scheme and a funded defined contribution scheme with the defined benefit scheme closed to new entrants in 2006 and both schemes were closed to future accrual from 2012. There is currently a deficit of just £3M on the schemes which have total obligations of £106M, so nothing really to worry about here. There is obviously a risk if interest rates were to rise, however, on two fronts with the increase in interest payments and the reduction in interest in housing following any rise. The group have £365M of committed bank facilities of which £215M is currently undrawn.

During the year the group appointed Sir Michael Lyons as a non-executive director. He chaired the Lyons Housing Commission to produce a road map for increasing house building in this country and prior to this, following a long career in local government, he was chairman of the BBC.

Demand for new homes continues to be strong which is being reflected across the country. The group has entered the year with a record order book and reservations to date are running 5% ahead of last year. They have secured 820 reservations in the first ten weeks of the year, some 28% ahead of last year and the board are looking forward to another year of significant progress. The group have updated their targets for 2018. They expect turnover to increase by 40% to £1.6BN, operating margins to improve to 19% and ROCE to be in excess of 21% despite the ongoing investment in land and inventory to grow their outlets. As the number of outlets grows, it is worth noting that it will increase the pressure on the teams and contractors to deliver.

At the current share price the shares trade on a PE ratio of 9.4 which falls to 8.2 on next year’s consensus forecast. After an increase in the final dividend, the shares are currently yielding 1.4% which increases to 2.2% on next year’s forecast.

On the 10th November he group released an AGM trading statement where they stated that the positive sales trend has continued. Currently, net private reservations are 28% ahead at 1,560 and the sales rate for the 19 weeks to 6 November 2015 is 0.68 per outlet per week, up 5% on last year. The Average Selling Price of private reservations for the financial year to date is £334,000, an 18% increase mainly driven by better quality outlets coming on stream to replace lower priced sites. With this strong sales performance, the board are confident this will be another year of significant progress.