Ricardo has now released its interim results for the year ending 2015.

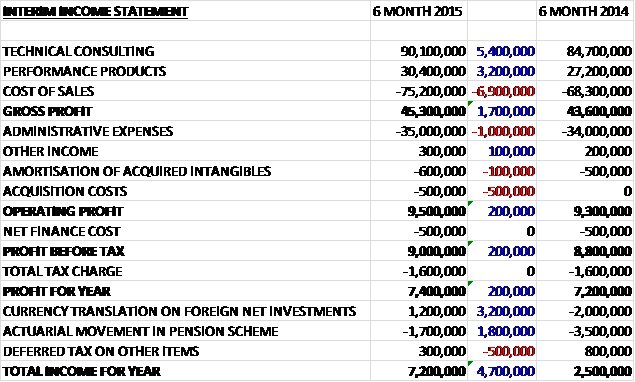

When compared to the first half of last year, revenues were up across both business segments and with cost of sales increasing by £6.9M the group recorded a gross profit £1.7M higher than last time. Admin expenses increased by £1M and there was also £500K of acquisition costs this year but with flat finance costs and tax charges the group still managed a £200K increase in profit for the period at £7.4M.

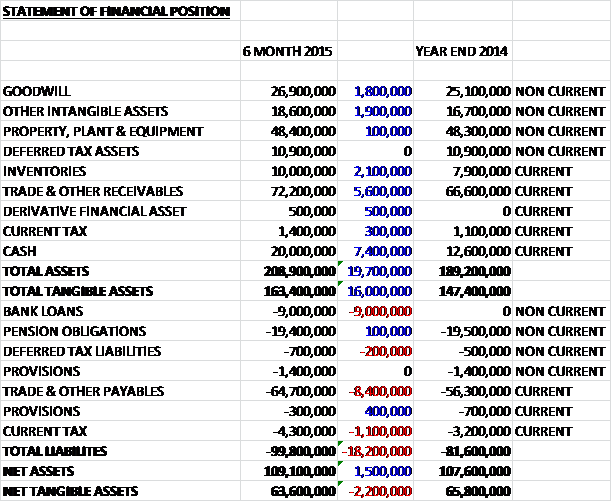

When compared to the end point of last year, total assets at the half year point increased by £19.7M driven by a £7.4M increase in cash, a £5.6M growth in trade & other receivables, a £2.1M increase in inventories and sizeable increases in goodwill and other tangible assets. Total Liabilities also increased due to a £9M increase in bank loans and an £8.4M growth in trade & other payables. The end result is a £2.2M fall in net tangible assets to £63.6M so the balance sheet remains strong despite the small decline.

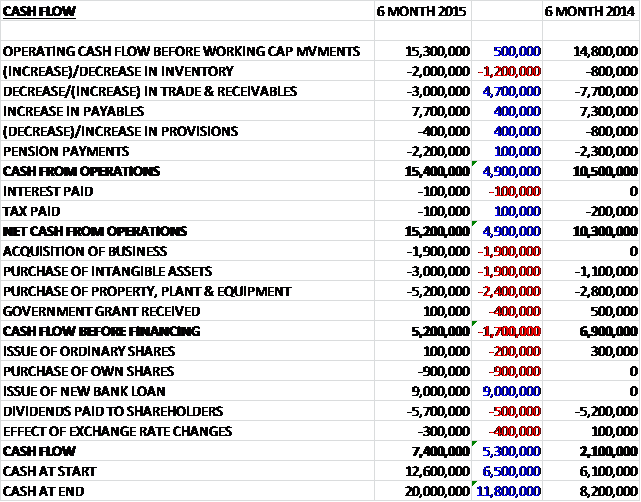

Before movements in working capital cash profits increased by £500K to £15.3M. Changes in working capital then broadly cancelled each other out so that net cash from operations increased by £4.9M to £15.2M. Of this cash, £5.2M was spent on property plant & equipment relating to the work on the vehicle emissions centre and expansion of the engine build facility as part of the supply agreement with McLaren. £3M was spent on acquiring intangible assets with the acquisition costing £1.9M in cash which all lead to a £5.2M cash flow before financing. The group then took out a new bank loan of £9M in order to cover the £5.7M of dividends and give a £7.4M cash inflow to leave the cash pile of £20M at the end of the half. It seems that the operational cash flow broadly covers the increased capital expenditure, the small acquisition and most of the dividends so the issue of new debt is intriguing – either the board are expecting a big cash out flow for the second half of the year or they are eyeing up a larger acquisition.

Operating profit at the Technical Consulting business increased by £1.3M to £6.9M. During the year the UK and German technical consulting businesses were reorganised to form a European technical consultancy division along with a separate motorcycle consultancy business incorporating the newly acquired Vepro, creating a critical mass of capability, expertise and global reach in motorcycle and scooter engineering. The European business is the main driver of profit generation with the US division much smaller in scope and performed at a similar level to the first half of last year with an encouraging pipeline of work and the environmental and strategic consulting businesses continued to make good progress. The sales offices in Asia continued to win significant orders for delivery elsewhere within the group including an order worth about £10M in January, after the end of the first half of the year.

In the Passenger Car market the group have experienced increasing levels of activity in the major automotive markets of China and Japan as well as in the US and UK. Fuel economy and CO2 emissions remain top drivers for projects. Ricardo have secured a range of large multi-year programmes in both vehicle systems and the core powertrain areas of their business, focusing on both new and existing product upgrades. Vehicle lighweighting also remains an area of growth and the group continue to invest in advanced combustion and other key technologies in areas related to overall vehicle efficiency improvement such as intelligent drivetrain and electrification. Autonomous vehicle technology is an exciting new area that is attracting interest in North America.

There has been strong growth in the commercial vehicle sector, particularly from the Asian markets and the group have secured a number of large engine and transmission orders across the medium and heavy duty sectors with interest continuing to be observed in Japan, China and Korea. Activities in the off-highway sector were largely driven by European based OEMs and the product offering focused on new powertrains and engine development, complete machine optimisation, cost effective after treatment solutions and hybridisation options, all of which attracted some interest during the year. The group is continuing to invest in energy recovery technology as part of their expansion into the wider off-highway sector.

The group’s expertise across the energy sector expanded with the acquisition of PPA. In power generation the focus remains on growing the large scale generator sets business and a number of large orders were won in Europe and Asia. Across the renewables sector the group continued to focus on offshore wind, energy storage and future cities programmes and have won a range of new contracts in these areas with electrical energy storage a key growth area in the US in particular. In defence, activities have been focused on the UK, US, Middle East and Asia. In the UK the network with the MOD has been broadened and relationships have been grown with defence contractors with the group focusing on developing products that can offer significant operational cost savings that can be integrated into existing vehicle platforms.

The rail business continued to develop in a variety of territories including North America, Europe and Asia. Recent projects have included engines, driveline, alternative fuels and strategic consultancy. Natural gas as a locomotive fuel and improving energy efficiency of current powertrains are seen as areas of growth. The group has attracted orders from a number of locomotive engine manufacturers who have to comply with ever tightening emissions regulations and satisfy their customer’s demands of for lower operating costs. Further growth is also expected in mass transit systems for large cities and high speed rail links. The key areas of growth within the marine sector are the efficiency of propulsion systems to improve fuel consumption and the implementation of a new ship energy management architecture. Growth is also being seen in emissions control as increasingly tough emissions legislation is implemented.

Growth in environmental consulting is focused on the private sector and expansion outside the UK. Key areas include air quality, waste and resources, sustainable transport and chemical risk. There has recently been announced a memorandum of understanding with the leading Saudi environmental services provider, Arensco, which will see a collaboration to provide environmental services capability to the Kingdom of Saudi Arabia.

Operating profit at the Performance Products business fell by £500K to £3.7M due to a change in programme mix despite the increase in revenues underpinned by increased activity on the McLaren engine programmes which offset a reduction in the delivery of monorail transmissions and defence vehicles. Production of the Porsche Cup and Bugatti transmissions has continued in line with the long term supply agreements and demand for engines from McLaren for both the 650S and P1 supercars has continued as expected. The group has started investing in the expansion of the engine build facility as part of the agreement that was agreed at the end of 2013. In motorsport this has been a busy year with manufacturing orders from Formula 1 customers and products such as the transmissions for the Japanese Super Formula 14, Indy Lights and the Renault World Series. Work has started on a new contract to design and manufacture a GT3 racing transmission for two new clients. In Rail the manufacture of monorail transmissions continued for contracts in Malaysia and Brazil.

During the period the group’s R&D department have been working on a number of initiatives. A prototype of the Adept 48V Mild Hybrid Electric Vehicle, which incorporates a 48 volt belt starter generator to reduce diesel engine turbo lag for downsized engines and a turbo generator to recover energy under high speed cruise situations, has been presented at a number of roadshows and initial feedback has been very positive regarding its driveability. The development for application of the TorqStor flywheel energy storage technology continues. In addition to an application for diggers in the construction industry, the group has shipped the first production intent prototype to Artemis Intelligent Power to be mated to its hydraulic transmission for use in rail diesel multiple units. Further tests should confirm a fuel economy saving of over 10%. Progress is also being made into applications using an electric generator to provide power for electric traction motors for on highway applications. The group’s wind turbine active bearing technology, MultiLife, improves the gearbox bearing life by up to 500%. It has been fully rig tested and is now ready for demonstration deployment in Ireland and will be fitted to an on shore turbine to commence trials in March.

Historically the group enjoys higher profits in the second half of the year and at the period end the order book stood at £138M, a decline of £4M compared to the end point of last year. After the period end, however, the group won a large contract which increased the order book to £152M, a record figure. Going forward the strategy will be to focus on the core areas of growth such as Transport, Security and Energy together with new opportunities in the area of Scarce Resources and Waste.

During the year the group acquired Vegro Ltd, a UK consultancy with motorcycle, power sport and niche vehicle expertise; and Power Planning Associates (PPA), a UK consultancy specialising in techno-economic and management consultancy services in the energy sector for a combined initial cash consideration of £3M (£500K of which was paid after the year-end) and a contingent consideration of £600K. The acquisitions came with intangible assets of £700K and generated goodwill of £2.2M. The acquired businesses contributed £400K of revenues and £100K of operating profit during the period since the purchase.

The shares yield 2.1% at the current share price and the group has net cash of £11M at the half year point, a decline of £1.6M when compared to the end of last year as the group drew down £9M on a committed bank facility that expires at the end of 2016. Interest is payable at a rather reasonable sounding 1.65% above LIBOR and there remains a further £26M undrawn.

This has been a decent update for the group. Profits increased fairly slowly despite the spend on the two small acquisitions. Net tangible assets fell slightly but the balance sheet remains strong and the group is generating broadly enough cash to cover capital expenditure, small acquisitions and dividends. It does seem to me that they may be targeting a larger acquisition given the increase in borrowings which otherwise seem unnecessary. Operationally, the consulting business continued to move ahead but the performance product business saw a modest decline in profits, presumably as the delivery of military vehicles slowed down. I would hope that the ramp up of the engine project for McLaren may combat this trend going forward though. The dividend yield is decent enough and I am more than happy to hold on to what is my second largest holding to see what plans they have for that cash.

After treading water for much of 2014, since the start of the year the shares seem to be on the move so this chart looks good to invest in.

As predicted above at the last update:

On the 17th April the group announced the acquisition of Lloyd’s Register Rail from Lloyds Register for a cash consideration of £42.5M which will be immediately earnings enhancing. LR Rail is an established rail consultancy and assurance business with a wide range of international clients which recorded revenues of £48.1M and EBITDA of £3.7M last year and has a 12 month order book in excess of £50M. It provides services ranging from assurance, rolling stock design, signalling & train control, intelligent rail systems, operational efficiency improvement and training. Examples of the client base include Network Rail, Nederlandse Spoorwegen, Hitachi Rail Europe, Cross Rail, MTR and Etihad Rail. The acquisition will be funded from the enlarged £75M bank facilities and should complete before July. The group intends to establish a “Ricardo Rail” business and a standalone assurance management entity known as Ricardo Certification.

This acquisition does not come cheap but it does seem a good fit and should add to the bottom line shortly after acquisition.

On the 20th May the group released a trading update to May. There has been a decent start to the second half of the year with order intake during the first four months higher than in the same period of last year with the order book standing at £152M compared to £141M at this point in 2014. Significant orders won include three engine design and development projects for customers in Asia, two vehicle development projects across the UK and Europe and a contract for the UK government in the environmental consulting business. In the US, orders continued to be slow in the traditional automotive market but a good pipeline is developing in the defence sector. Total revenue in the first 10 months of the year is up 6% and profit is tracking in line with expectations. The Technical Consulting business performed well and the Performance Products business is on track with its preparations for the new McLaren contract next year. Overall not a bad update, but the tone seems somewhat subdued and the difficult US market is a disappointment. I will continue holding here for the time being but will watch closely as Ricardo has become one of my largest holdings.

On the 1st July the group announced a few board changes. David hall has stepped down as Senior Independent director to be replaced by Peter Gilchrist. In addition Hans Schopf has retired as non-executive director having been in the role since 2009. He is being replaced by Laurie Bowen who is CEO Business Solutions, Cable & Wireless Communications.

On the 19th August the group announced the acquisition of Cascade Consulting, an environmental consultancy specialising in the UK water sector. The acquisition follows the collaboration with Cascade that began in February and will bring additional capability and reach in the areas of water resource and water quality management, ecosystem services and environmental impact assessment. The business has 34 employees and generates about £3M in annual revenues, so this is a small addition to the group. I cannot find any indication of how much was spent on the acquisition.