RPS is an international consultancy that provides advice on the exploration and production of oil and gas and other natural resources; the development and management of the built and natural environment; and the development of infrastructure to ensure the supply of energy resources to market and to provide appropriate transport, water and power resources.

The group has a number of different business segments. Energy involves the provision of integrated technical, commercial and project management support and training in the fields of geoscience, engineering and health, safety and environment on a global basis to the energy sector. Built and Natural Environment involves consultancy services to many aspects of the property and infrastructure development and management sectors. These include environmental assessment, the management of water resources, oceanography, health and safety, risk management, town and country planning, building, landscape and urban design, surveying and transport planning. Consultancy services are provided on a regional basis in Europe and North America. In the Australia Asia Pacific division there is a single board that manages both the energy and build and natural environment sectors so this is taken as a separate segment.

In the case of fixed price contracts, revenue is recognised in proportion to the stage of completion of the transaction at the balance sheet date measured by reference to the milestones achieved or cost incurred as a proportion of the total forecast cost. RPS has now released its final results for the year ended 2014.

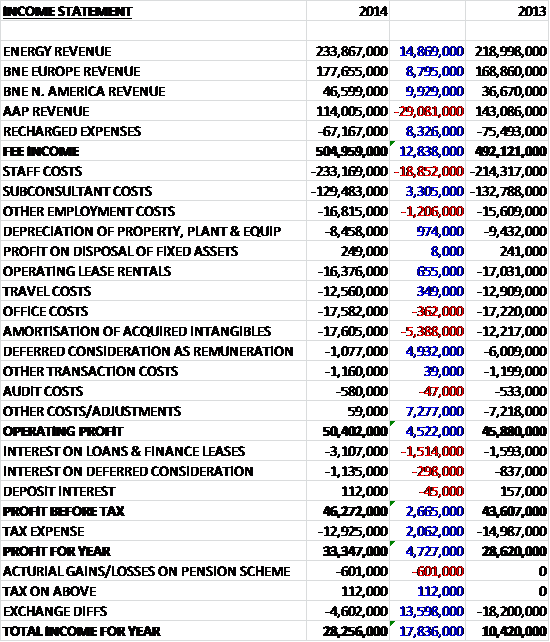

Overall revenue increased year on year as a £29.1M decline in Australia Asia Pacific revenue was more than offset by increases in all the other business segments. Recharged expenses fell during the year so fee income was £505M, an increase of £12.8M when compared to last year. Staff costs saw a significant increase, up £18.9M and amortisation increased by £5.4M but more modest falls in sub consultant costs and depreciation, along with a £4.9M decline in deferred consideration considered as remuneration and other operating costs meant that operating profit was some £4.5M ahead of last year. There was a considerable increase on finance lease interest and a smaller growth in deferred consideration interest but this was counteracted by a £2.1M fall in tax expenses so that the profit for the year stood at £33.3M, an increase of £4.7M when compared to 2013.

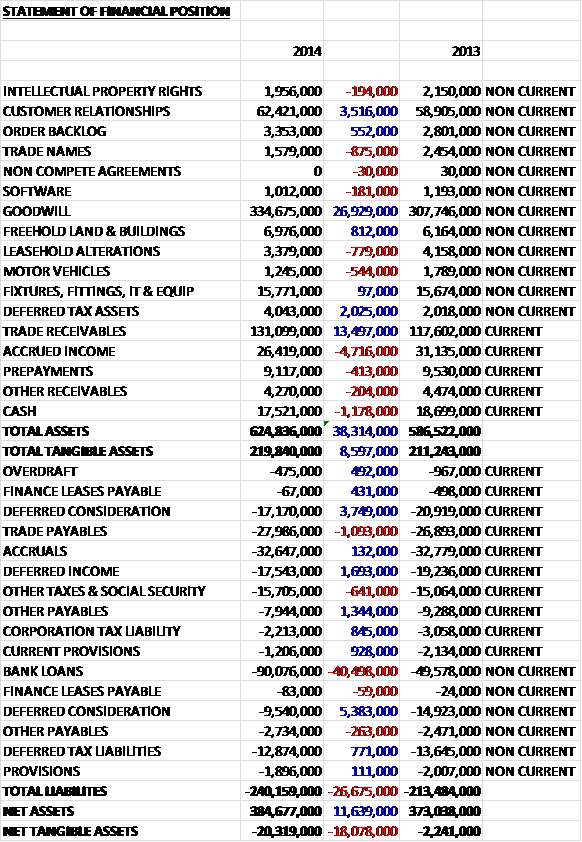

When compared to the end point of last year, total assets increased by £38.3M driven by a £26.9M increase in goodwill, a £13.5M growth in trade receivables, a £3.5M increase in customer relationships and a £2M growth in deferred tax assets, partially offset by £4.7M fall in deferred income and a £1.2M decline in cash. Liabilities also increased during the year as a £40.5M hike in bank loans was partially offset by a £9.1M fall in deferred consideration, a £1.7M decline in deferred income and a £1.3M decrease in other payables to give a net tangible asset level of -£20.3M, a deterioration of £18.1M year on year and a bit of a disappointing balance sheet in my view. It is also worth noting that there is £46M worth of operating leases off the balance sheet, although these have declined year on year.

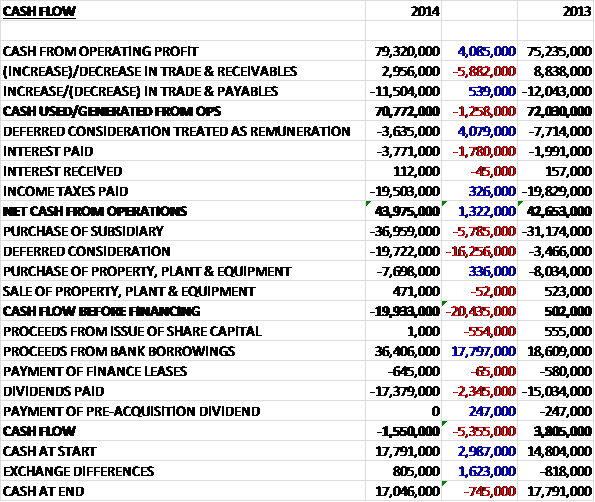

Before movements in working capital, cash profits increased by £4.1M to £79.3m before this was eroded somewhat by a large fall in payables to produce cash from operations of £70.8M. After significant deferred consideration as remuneration and interest, the net cash from operations after tax stood at £44M, an increase of £1.3M year on year. The group then spent an incredible £19.7M on deferred consideration, £7.7M on capital expenditure and £37M on acquisitions to give a cash outflow of £20M before financing. This necessitated £36.4M of new borrowings, offset by £17.4M spent on dividends to give a cash outflow for the year of £1.6M and a cash level of £17M at the year end. Another company that is borrowing to pay its dividends then, not something I am a fan of. If the group is short of cash then I would prefer they cut the divi for a year if it is a one-off but not everyone will agree with me!

The profit in the energy sector was £38.8M, an increase of £2.5M year on year on a margin of 19% compared to 19.5% last year. The energy business continued to grow, with an improved result in the second half supported by acquisitions made last year, managing the rapid decline in oil price and political unrest in the Middle East. The group experienced good demand for their consultancy advice, including transaction and asset valuation support. During Q2 some of the group’s clients sought to reduce their expenditure which continued through the second half of the year against the backdrop of falling oil prices. Their trading was also affected by the political disruption in the Middle East which caused clients to delay investment in Iraq. Recent market conditions have been unusually volatile. As a result clients are likely, in the short term, to continue to focus on cost management and therefore the group are reducing their cost base and concentrating on the parts of the market and projects likely to receive benefit.

The profit in the built and natural environment Europe sector was £21.1M, an increase of £2.4M when compared to last year on a margin of 13.6% compared to 12.8% last year. The group experienced some clients looking to cut costs in the operational and environmental management sectors but still managed to secure good performances in the Dutch and UK businesses providing support to the nuclear and defence industries. The acquisition of Clear Environmental Consultants will assist the development of the business as they seek to renew and win a significant number of contracts with the UK water utilities. It is expected that this business should sow further growth in 2015.

The profit in the build and natural environment North America sector was £9.1M, an increase of £700K year on year on a margin of 22% compared to 25.4% last year. The acquisition of GaiaTech has boosted the group’s offering in the environmental due diligence market, a high margin activity, and has integrated well so far. The parts of the business close to the oil and gas activities experienced some modest expenditure tightening from clients and staff retention became difficult in the part of the business involved in permitting and licensing of industrial facilities which significantly reduced the performance in that area. The oceanography business performed well, however. The addition of GaiaTech gives the board confidence about the division’s performance in 2015.

The profit in the Australia Asia Pacific sector was £8.2M, a fall of £600K when compared to last year on a margin of 9.3% compared to 7.9% last year. The acquisitions of Point and Whelans, both property consultants, enabled the business to offset the significant impact of the severe slowdown in investment in the resources sector in this region. Throughout the year the mining and energy clients in the region remained focused on operational efficiency rather than capital expenditure which has caused a significant number of projects to be delayed or cancelled which has led to a reduction in the cost base in the region.

As the business is repositioned, they are benefiting from increased client investment in urban development and public sector infrastructure projects but state funding in Queensland and Victoria has been slowed by recent changes in government but despite this, they remain attractive markets and the board expect an improved performance for the division in 2015.

It is noticeable this year that trade receivables more than 30 days overdue increased from £13.5M last year to £22.3M which is something that we should keep an eye on and could help explain the big jump in receivables that we have seen this year.

The group really relies on acquisitions for growth, in fact I don’t remember seeing another company that has been as acquisitive as this one. The board have stated that this will continue to be a part of their strategy and are seeking to acquire further small to medium sized businesses in North America, Australia and Europe. They expect further transactions during the course of 2015 supported by their “strong” balance sheet – definitely their words, not mine!

During the year the group made a total of six acquisitions. Whelans Corp is a surveying business based in Australia. It was purchased for £1.4M in cash and another £619K in deferred consideration and generated goodwill of £773K. Since the acquisition the business has generated £407K in profit so this looks to be a good value acquisition to me. Clear Environmental Consultants is a water consultancy based in the UK. It was purchased for £6.8M with a contingent consideration of £1.2M depending on the renewal of a key contract and generated goodwill of £3.2M. Since the purchase the business has generated operating profits of £423K so this also seems to be reasonable value.

GaiaTech Holdings is an environmental consultancy based in the US. It was purchased for £17.9M in cash and generated goodwill of £11.1M. Since the acquisition date the business has contributed £1.2M to operating profits. CgMs Holdings is a project management company based in the UK. It was purchased for £7M in cash and £5.8M in deferred consideration and generated goodwill of £7.6M. Since the acquisition date in August the business has generated operating profit of £173K so the value here looks a little toppy. Delphi is an oil and gas consultancy based in Norway. It was purchased for £384K in cash and £358K in deferred consideration and generated goodwill of £501K. Since the acquisition the business has contributed £13K to operating profits. Point Project Management is a project management company based in Australia. It was purchased for £10.4M in cash and £6.4M in deferred consideration and generated goodwill of £9.5M. Since the acquisition in September the business has contributed £449K to operating profits.

The group has two defined benefit pension schemes which are closed to new entrants. Although they are showing a deficit, the amount doesn’t seem to be particularly material. There are two main borrowing facilities. There is a committed £125M multi-currency revolving credit facility that has a couple of covenants attached. There is also a $150M seven year US private placement shelf facility. Seven year notes with principle of £30M were drawn in September bearing fixed interest at just under 4% per annum and seven year notes with principle of $34.1M were drawn at the same time bearing interest at 3.84% per annum. The group has £86.8M undrawn on the credit facility and is rather susceptible to interest rate increases with a 1% hike decreasing profit before tax by £694K. The group hedges the majority of its transactional foreign currency exposures, so the sensitivity to foreign currency risk is not material.

The real risks involve the global economic environment. Continued Eurozone uncertainties may affect the businesses in Ireland and the Netherlands, and the continued slowdown in the Australian natural resources sector has continued to affect the group’s trading performance there. In addition the reduction in global oil prices and the resultant project delays has had an impact on the performance of the energy business. As well as the general economic environment, the group is also sensitive to political events and this year their operations in Iraq have been affected by the continued conflict there whilst sanctions imposed on the Russia are likely to affect their business sin that part of the world. In addition, recent state elections in Australia may reduce demand for their services there.

It has to be said that in my view the executive directors are very generously paid with CEO Alan Hearne earning nearly a million pounds during the year, of which £243K was a bonus. Interestingly he has been CEO for over thirty years and is still only 62.

After the end of the balance sheet date the group acquired Klotz Associates, a Texas based consultancy providing engineering, planning and environmental services for a maximum consideration of £15.9M payable entirely in cash. The amount paid on acquisition was £11.1M with £3.2M to be paid on the first anniversary of completion and £1.6M to be paid on the second anniversary. Last year the business had a profit before tax of £2.4M.

At the current share price the shares trade on a PE ratio of 14.4 decreasing to 10.2 on next year’s consensus forecast which doesn’t look too taxing. After a 15% increase in the total dividend, the shares currently have a yield of 3.9% which increases to 4.5% on next year’s forecast which again seems pretty good but whether the group can actually afford dividends of this size is up for debate. At the year end the group was in a net debt position of £73.2M compared to £32.4M at the end of last year.

So, this has been a bit of a mixed year. Profits were up as was operational cash flow but this only seems to be because more of the deferred consideration was counted as remuneration last year which apparently means it is an operating expense for reasons I don’t really understand. There is some free cash flow but it is not enough to cover the acquisitions which have to be considered operating expenses too in my view as that is an important part of the group’s strategy. The balance sheet is stuffed full with goodwill and as such there is quite a hefty negative net tangible asset figure which got worse during the year.

Operationally, the energy business did OK due to prior acquisitions and the build environment businesses seem to be doing quite well but the Australian business has been hit by the continued low commodity prices and collapse of the oil price. Indeed, the balance sheet concerns aside, the real issue at the moment is the beleaguered state of the markets in which the group operates – I find it difficult to imagine that the energy and Australian businesses are going to pick up any time soon, which brings me on to the large increase in overdue receivables – I am concerned this could be because some of the group’s customers are finding cash flow a bit of a problem. The shares look cheap on both a PE ration basis and on the dividend yield but I feel the risks of things getting worse outweigh the potential value on offer given the increasing debt and falling net assets.