Serabi Gold has now released its interim results for the year ending 2016.

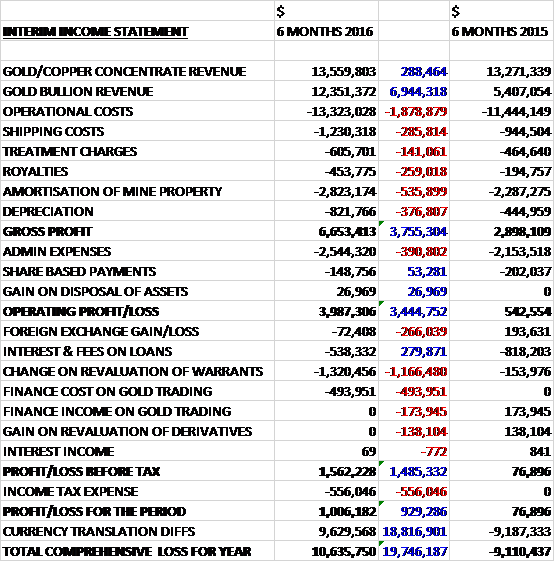

Revenues increased when compared to the first half of last year with a $6.9M growth in gold bullion revenue and a $288K increase in concentrate revenue. Operating costs only increased by $1.9M due to higher labour costs and higher maintenance costs reflecting the use of generators to provide reliable power for the operations, with smaller increases in amortisation and depreciation to give a gross profit $3.8M higher. Admin expenses increased by $390K which meant that the operating profit was $3.4M higher than last time. We then see a $1.2M charge relating to the revaluation of warrants relating to the Sprott call option over gold, after the gold price increased, and there was a $494K finance cost on gold trading compared to a $174K gain last time reflecting short term movements in the gold price. Tax charges increased by $556K to give a profit for the period of $1M, a growth of $929K year on year.

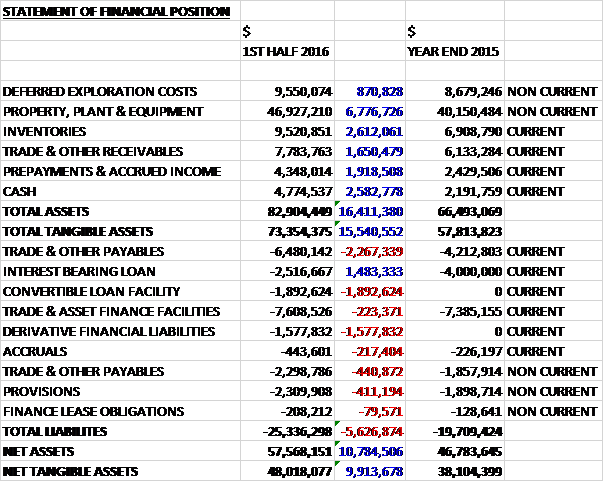

When compared to the end point of last year, total assets increased by $16.4M to $82.9M driven by a $6.8M growth in property, plant & equipment, mostly as a result of the strengthening of the Peso; a $2.6M increase in inventories; a $2.6M growth in cash; a $1.9M increase in prepayments & accrued income and a $1.7M growth in receivables. Total liabilities also increased during the period as a $1.5M decrease in the interest bearing loan was more than offset by a $1.9M growth in the convertible loan facility, a $2.3M increase in payables and a $1.6M increase in derivative financial liabilities. The end result was a net tangible asset level of $48M, a growth of $9.9M over the past six months.

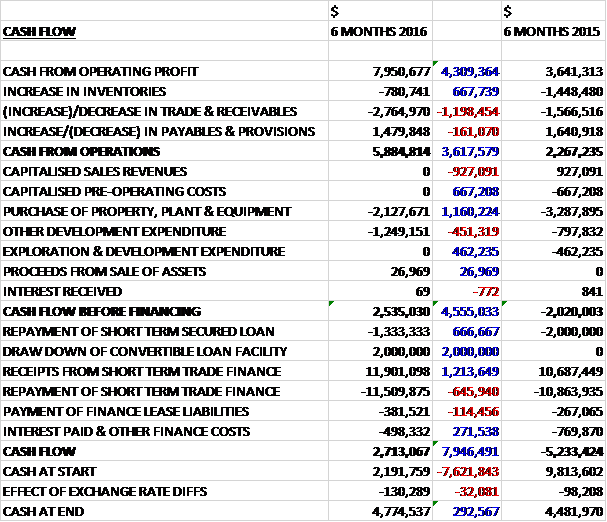

Before movements in working capital, cash profits increased by $4.3M to $8M. There was a modest outflow from working capital and the cash from operations came in at $5.9M, a growth of $3.6M year on year. The group spent $2.1M on tangible assets and $1.2M on development expenditure which still left $2.5M of free cash flow. After interest payments of $498K and finance lease payments of $381K and various movements in different borrowing facilities, the cash flow for the period was $2.7M and the cash level at the end of the half was $4.8M.

The average gold price received in the period was $1,216 per ounce compared to $1,182 in the first half of last year and the all in sustaining cost was $945 per ounce, compared to $967 last time. During the half, 71,152 tonnes of ore was mined at a grade of 10.33g/t (compared to 63,992 tonnes at 9.85g/t last year) which corresponds to 33,606 tonnes at 9.56g/t in Q2 and 37,546 tonnes at 11.02g/t in Q1. In all, 76,017 tonnes was milled at 8.37g/t in H1 (compared to 63,662 tonnes at 8.36g/t last year). This corresponds to 39,402 tonnes at 8.17g/t in Q2, producing 9,896 ounces of gold; and 36,615 tonnes as 8.58g/t in Q1, producing 9,771 ounces of gold. In all, 19,667 ounces was produced in H1, an increase of 4,041 ounces year on year.

Of the 33,606 tonnes of ore mined in Q2, 25,198 tonnes at a grade of 10.48g/t was mined from Palito and 8.408 tonnes at 6.81g/t was mined from Sao Chico. At Palito, management expect that output for 2016 will be between 105,000 and 110,000 tonnes at an average grade of between 8.5g/t and 8.9g/t. The ore from Sao Chico continued to be derived from development operations rather than from stoping, a situation that is expected to start to reverse in the second half of the year. At Sao Chico, in all, 8,408 tonnes of ore was mined in Q2 at a grade of 6.81g/t compared to 10,794 tonnes at a grade of 9g/t in Q1.

In the first half of the year, ore output from Palito was 5.5% less than in the first half of last year. This lower production level was expected, however, reflecting the limitations of the level of ore that can be processed and the availability of ore from the Sao Chico mine to supplement this production. The mine production for Q2 was 13% higher, however.

At Palito, during the year the group has focused on opening up new sectors as well as continuing to develop the existing ones. Up until this year, mining operations at the mine had focussed on the G1, G2 and G3 vein complex as well as the Palito West sector. This year they have continued to develop these two sectors but have also given increased priority to developing previously drilled but undeveloped sectors in the upper levels, namely Senna and Chico da Santa. The latter lies to the east of the G1, G2 and G3 vein complex whilst Senna is located to the west. With four sectors now being developed underground at the mine, the group completed about 3,800 metres of horizontal development in the first half of the year.

In the G1, G2 and G3 complex, the main ramp was further deepened and is now close to reaching the -50 metre relative level which will be the next production level. Currently the -20mRL is the lowest development level at the mine where the G3 vein is being developed and about 400m of ore development has been completed so far this year. In the Palito west sector, an internal ramp from the 61mRL to the 31mRL has been completed and about 100 metres of ore development on the 31mRL has been completed so far.

The Senna zone is not entirely new. It was mined during 2008 and 2009 as a small open pit where about 25,000 tonnes of oxide ore with a grade of 3g/t was extracted. Based on the ore grades recovered from the open pit operation and deeper exploration drill holes, management is hopeful of the potential of this zone. One exploration drill hole reported an intersection about 300m below the surface of 0.55 metres at a grade of nearly 51g/t. In December last year the Senna vein was exposed for the first time underground, since which time 570 metres of ore development and 410 metres of waste development have been completed on the 225mRL and 237mRL during the year. Internal ramps are currently being advanced to access the next development levels of 210mRL and 250mRL during August. The zone has independent access from the surface.

Further improvements undertaken within the process plant during the year have included the installation of additional flotation capacity and automation, along with new carbon screens within the CIP tanks to improve inter-tank flow rates. These improvements have been funded from the cash flow from the current operations. Processing rates for ROM ore have increased by 18% to 417tpd

It should be noted, however, that once the surface stocks have been consumed and with the group’s current understanding of the mining resources at both Palito and Sao Chico, management currently consider it unlikely that in the near term future mine plans can support the increased plant capacity. As a result the operation will then become limited by the tonnages that can be mined and the third ball mill will revert to its primary purpose of providing contingency in the plant. Since the plant started operating, the time available for essential maintenance has been scarce so the new mill means the operation can now comfortably accommodate much needed maintenance time as well as absorbing any unexpected interruptions to operations.

At Sao Chico, during the year the decision to implement sublevel open stoping as the principal mining method was taken, and this resulted in the development of sublevels with 12 metre vertical spacings. Each sublevel is advanced three metres at a time and channel sampled. The closer sample spacing that this allows has greatly increased the understanding of the orebody and this increased mine development has enabled the group to now define a clear two year mine plan.

The group has reported that the high grade mineralisation is dominantly hosted in a constant alteration zone that can be anything from two to ten metres wide. The zone itself is readily identifiable but the high grade gold zones within this alteration zone are much less so, and as a result the mining operations require on-lode development at regular vertical intervals with regular channel sampling and in-fill drilling between these levels to best define the high grade gold mineralisation. This approach allows the group’s mining personnel to readily identify stoping blocks and optimise mining of the high grade gold zones.

The main vein at Sao Chico has gold grades that are quite erratic and are hosted in four steeply plunging pay shoots. In these pay shorts the grades are often truly spectacular, often being in excess of 100g/t of gold. Outside the pay shorts the vein is continuous but with low gold grades and as a result it is unavoidable that, as the mine development passes between the pay shorts, lower grade ore has to be mined. The central pay shoot is the most established of these four high grade shoots and is some 100 metres long. The group will continue to focus, in the near-term, on developing this part of the main vein and some consistent higher grade development ore is being generated as a result. Access to other pay shoots along the strike will not be lost and these will be available for development later in the year.

During Q2, the group started underground exploration drilling of the central pay shoot targeting its down dip extension. The results from the first hold that has been completed were encouraging with an intersection about 100 metres below the current deepest workings and about 240 below the surface over a drilled width of 2.3m being made with a grade of 46.2g/t. Averaged mined grades for the quarter across both mines continued to be around 10g/t o gold which has been the case for the past two years. At the end of the period, combined ore stocks from Palito and Sao Chico were about 12,000 tonnes with an average grade of 5g/t of gold compared to the same period of last year when they were 11,900 tonnes at a grade of 4g/t.

As well as the potential that exists to grow resources at Sao Chico, the Palito south, Curretela and Piaui prospects close to the Palito mine still provide good opportunities for identifying additional resources which could both enhance current production levels and extend the life of the mine. The group is undertaking geophysical programmes within the vicinity of both working mines in the second half of the year. The objective of these programmes is to secure additional geological data to better plan the next stage of exploration drilling that is expected to be undertaken during 2017. At this time no surface drilling or other surface exploration activities are currently planned.

In the longer term, dependent on levels of cash flow, the group will step up its exploration activity and will be looking to add to its resource base and production potential by establishing additional satellite high grade gold mines in relatively close proximity to the current operation which would have a centralised processing facility. In this way the group expects to be able to grow its production base at low capital cost, avoid the need for major infrastructure improvements and have low environmental impact.

The forecasted gold production for 2016 is expected to exceed 37,000 ounces but reflecting the 22% strengthening of the Brazilian Real, the group has revised its cost guidance and now expects all in sustaining costs for the year will be between $950 and $985 per ounce.

Over the next year or so, the group has $5.4M of contractual obligations consisting of $4.9M of short term debt, $431K of capital lease obligations and $94K of operating leases.

In December 2015, the group’s major shareholder, Fratelli Investments, agreed to provide an interim unsecured short term working capital convertible loan facility of $5M to provide additional working capital facilities. The loan is for a period expiring at the end of January 2017. It can be drawn down in up to three separate instalments of an initial $2M and two further instalments of $1.5M each. Interest is chargeable at the rate of 12% per annum.

The first $2M of the loan is convertible at the election of Fratelli into new Serabi shares at an exercise price of 3.6p per share at any time. The remaining amount of the loan, if drawn down, could be repaid by the group at its option at any time before the end of June.

Thereafter, Fratelli would have the right to convert all or part of the remaining amount into new shares at 3.6p per share. In January the group made an initial draw down of $2M but not further draw down has been made.

In August, Fratelli exercised its right to convert its outstanding $2M convertible loan into shares at a price of 3.6p per share which means that they now own 55.3% of the total share capital.

At the start of the year the group granted Sprott a call option over 2,500 ounces of gold at a price of $1,125. Just after the period-end, at the start of July, Sprott exercised options over 1,250 ounces of gold, establishing a liability of $298K, of which $150K has been settled with the remaining amount due for repayment by the end of the year.

As of the period-end, Sprott held a call option exercisable over 2,500 ounces of gold exercisable at a price of $1,125 per ounce. In July they exercised options over half this amount, establishing a liability on the group of $298K of which $150K has been settled with the remaining amount due for repayment at the December.

Overall then the increase in gold prices has meant that this has been a fairly successful period for the group. Profits were up, net assets increased and a growth in operating cash flow gave rise to some free cash generation. The group achieved a price of $1,216 per ounce compared to $1,182 last time and costs per ounce fell from $967 to $945, although the appreciation of the Brazilian currency means that they are guiding towards annual costs of between $950 and $985 per ounce, which although not ideal, should still be profitable.

The process plant improvements have been completed which should give the group some much-needed back up. Grades being mined in Q2 did decline somewhat but this was due to Sao Chico where grades are more erratic. I have a lingering concern that Fratelli is becoming even more powerful with the recent convertible loan conversion and the Sprott call option is now looking fairly costly and I have decided to take profits here for now whilst the gold price takes a breather.