Serabi Gold has now released their interim results for the year ending 2017.

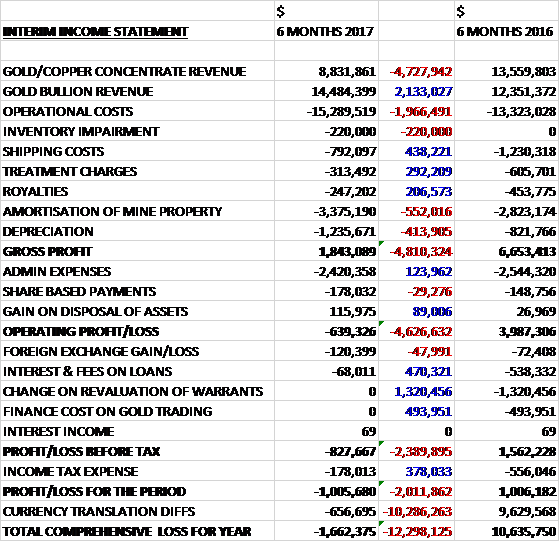

Revenues declined when compared to the first half of last year as a $2.1M growth in bullion sales was more than offset by a $4.7M decline in concentrate sales. Operational costs increased by $2M, mainly due to forex movements and staff pay rises, amortisation was up $552K and depreciation grew by $414K, also reflecting forex movements, although shipping costs were down $438K due to a reduction in concentrate shipments, treatment charges declined by $292K, and royalties fell by $207K which meant that the gross profit was $4.8M lower. Admin expenses saw a modest decline which gave an operating loss that saw a $4.6M negative swing. Loan interest charges declined by $470K, there was no finance cost on gold trading and no revaluation of warrants, which cost $494K and $1.3M last year respectively. After tax expenses fell by $378K the loss for the period was $1M, a detrimental movement of $2M year on year.

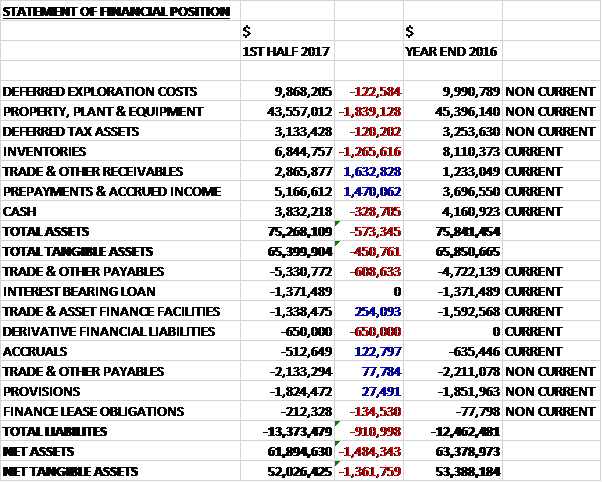

When compared to the end point of last year, total assets declined by $573K driven by a $1.8M fall in property, plant and equipment and a $1.3M decrease in inventories due to lower levels of ore stockpiles, partially offset by a $1.6M growth in receivables reflecting settlement timings and a $1.5M increase in prepayments and accrued income reflecting the funds not yet received from the new Sprott loan and higher prepaid taxes. Total liabilities grew during the period, mainly due to a $650K increase in derivative financial liabilities relating to Sprott’s call option over some gold and a $609K growth in payables reflecting timing differences. The end result was a net tangible asset level of $52M, a decline of $1.4M over the past six months.

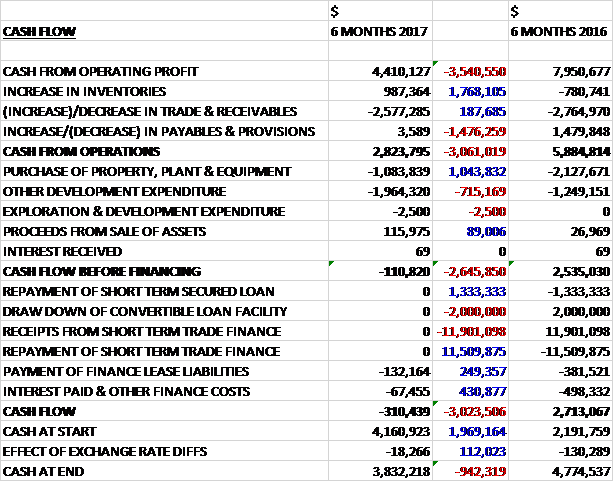

Before movements in working capital, cash profits declined by $3.5M to $4.4M. There was a cash outflow from working capital but this was slightly less than last time so the cash from operations was $2.8M, a decline of $3.1M year on year. The group spent $1.1M on property, plant and equipment and $2M on other development expenditure so there was a cash outflow of $111K before financing. The group repaid $132K of finance leases and $67K in other interest so the cash outflow for the half year was $310K and the cash level at the period-end was $3.8M.

During the half year period the group produced 18,009 ounces of gold compared to 19,667 in the prior year. In Q1 they produced 9,861 ounces with 8,148 ounces being produced in Q2. The sales price was broadly flat at $1,221 per ounce but the AISC cost of production increased from $945 per ounce to $1,072. The cost guidance for the full year is between $950 and $975 per ounce but the cost profile is subject to change as a result of exchange rate variations between the Real and US dollar. They are currently forecasting gold production of around 40,000 ounces for the year.

The group mined a total of 78,993 tonnes of ore compared to 71,152 tonnes last year reflecting he increased number of working faces now available at Sao Chico, but the grade fell from 10.29g/t to 8.89g/t with the figure in Q2 even worse at 7.8g/t. They started to increase the level of stoping activity in Q1 but the stoping method at Sao Chico requires the use of remote controlled loaders and during the period they were still in the process of building up their fleet. In Q1 they had one loader with a second due to arrive in June but the first loader, despite being only four months old, suffered a mechanical problem which significantly reduced stoping production in April and May. It was therefore necessary to use development ore, at a lower grade, as alternative mill feed.

By June, with the original unit returning to full operation and the second unit being commissioned, production improved significantly reflected in 42% of the gold production from Sao Chico being achieved in June. With the additional development completed in the quarter, making available additional stoping blocks, the group is confident that the Q2 shortfall will be recovered over the second half of the year.

The group milled 90,568 tonnes of ore at a grade of 6.69g/t compared to 76,017 tonnes at 8.38g/t, reflecting the increased plant capacity installed in H2, allowing the processing of lower grade stockpiled material. The throughput of the plant increased by around 19% with the introduction of the third ball mill at the end of June 2016 having a significant effect on rates. The increase also reflects the improvements in operational efficiency of the plant with the introduction of the gravity circuit and ILR for treating Sao Chico ore, reducing the levels of gold that would otherwise have been treated in the CIP circuit.

As far as exploration is concerned, a programme is being undertaken at Sao Chico using surface IP and, whilst it is also being undertaken around the Sao Chico orebody, it is also being undertaken in some of the recently acquired tenements around Sao Chico. The programme has to be suspended during Q4 2016 due to poor weather and will restart in the second half of this year. Management considers that these areas, which are located to the south and west of the original license area, offer good potential for hosting strike extensions of the current Sao Chico veins.

In consideration of a loan facility with Sprott for $5M the group has granted them call options over 6,109 ounces of gold at a strike price of $1,320 per ounce (currently the price is around $1,275) exercisable up until the end of 2019. These funds were received after the period-end.

At the current share price the shares are trading on a PE ratio of 8.4 which falls to 4.3 on the full year consensus forecast.

Overall then this has been a difficult period for the group. They made a loss as opposed to a profit last time, net assets were down and the operating cash flow declined with no free cash being generated. Gold production was down due to the group having to use development ore stockpiles as the new loader malfunctioned. This has apparently been sorted out now but the group will have to hope for no more issues in order to hit their production target for the year. If they do hit it, the forward PE of 4.3 looks cheap but this is a big if. I hold on for now, however.

On the 23rd October the group released an update covering Q3. After a disappointing Q2 production of 8,148 ounces, production improved somewhat in Q3 to 9,657 ounces and the total production for the year to date is around 28,000 ounces.

Mine production from both orebodies progressed well, and there were improvements in the average grades mined during the quarter, with average grades over 9g/t. Mine development at Sao Chico has been encouraging with the 40mRL level exhibiting greater than forecast payable strike lengths.

With current plant limitations there has been little success in running down the levels of the flotation tails. To date they have pumped the tailings wet to the CIP plant but this has proven to be slow and labour intensive. Passing the material dry is restricted by belt capacity, and therefore would be displacing higher grade ore. They are now designing and constructing and independent conveyor to feed these tails directly into the ball mills, which means that the material can be added to the current dry mill feed, and therefore increase the levels that can be treated each month. They hope to be operational with this by mid-November.

There is also an intention to introduce an x-ray ore sorter after the main crushing plant that will separate material ahead of milling and remove from the mill feed a significant proportion of the waste that would otherwise have formed part of the feed into the plant. Not only will this reduce process costs, but it will also liberate capacity in a mill constrained operation. They therefore hope they can de-bottleneck the plant using this technology, elevating mill feed grade in the process, and free up plant capacity for the future organic growth. This equipment is built to order and it is expected to take up to a year before it can be commissioned. Payback of the estimated $1.2M costs is expected to be less than a year, however.

With improved metal prices and exchange rates, the group have recently been enjoying better margins and cash generation. They have now been able to commit to an initial 8,000m surface drill programme, which will focus on drilling the many potential vein extensions they have at Palito.

The full programme they would like to undertake is substantially greater than 8,000m and both ore bodies could benefit from higher levels of strike extension drilling. The full programme, targeting 60,000m would be completed in two phases. This initial 8,000m forms part of phase one and is a programme they can start comfortably out of operational cash flow. Drilling will get underway in November.