Shoe Zone has now released its final results for the year ended 2015.

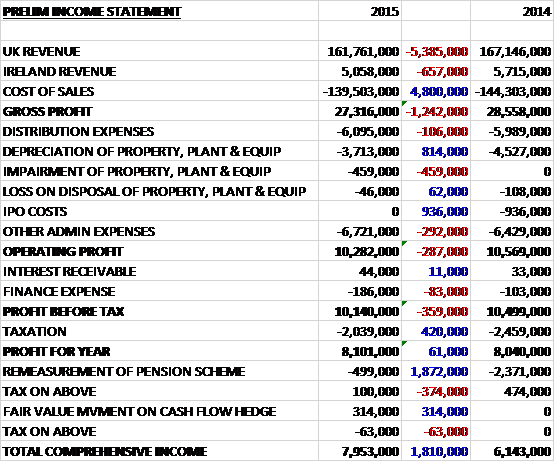

Revenues declined when compared to 2014 due to a £5.4M fall in UK revenue and a £657K decrease in Irish revenue caused by the closure of some stores and difficult trading conditions following the warm autumn weather. Cost of sales also fell but gross profit still came in £1.2M below that of last year. Distribution expenses were up modestly but we see an £814K decline in depreciation, partially offset by a £459K impairment of property, plant and equipment and a £292K increase in other admin costs. Despite the IPO costs of £936K not being repeated this time, the operating profit fell by £287K and after finance costs increased, the pre-tax profit was down by some £359K. A large fall in tax, however, meant that the profit for the year came in at £8.1M, a growth of just £61K year on year.

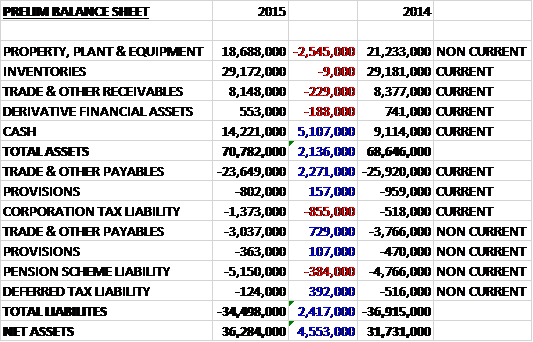

Total assets grew by £2.1M when compared to the end point of last year driven by a £5.1M increase in cash, partially offset by a £2.5M fall in property, plant & equipment and a £229K decline in receivables. Conversely, total liabilities fell during the year as an £855K growth in corporation tax liabilities and a £384K increase in the pension liability was more than offset by a £3M fall in payables, and a £392K decrease in the deferred tax liability. The end result is a net tangible asset level of £36.3M, a growth of £4.6M year on year.

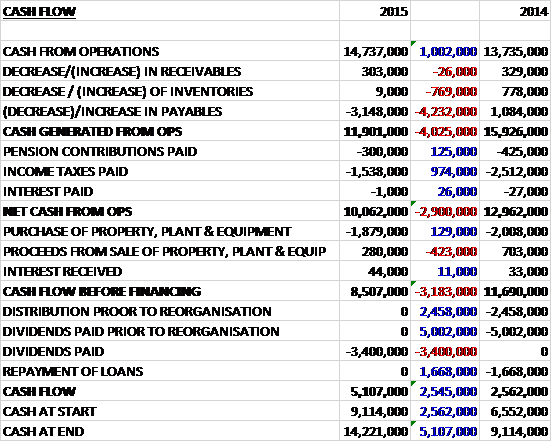

Before movements in working capital, cash profits increased by £1M to £14.7M. There was a cash outflow through working capital, in particular a fall in payables, but pension contributions, interest and taxes were all lower than last year to give a net cash from operations of £10.1M, a decline of £2.9M year on year. The group then spent a net £1.6M on capex which meant that free cash flow was £8.5M. The group then only spent £3.4M on dividends to give a cash flow for the year of £5.1M and a cash level of £14.2M to at the year-end.

Following a slow start to the year the group made some adjustments to their future ranges to ensure greater diversity of product and to give them future confidence about average price and transaction value. These transaction values stabilised in the second half of the year and have reverted to historic levels after the year-end. The group have made progress in their non-footwear ranges. During the year sales were up 33% to £5.5M and 2016 is already showing good signs of further growth and they have extended the full non-footwear range in their Grade 3 stores which has apparently had a great start.

At the end of the year the group were trading from 535 stores with 12 new ones opening, including seven relocations. They also completed 40 store refits during the year, at a total capex of £1.9M. They continue to rationalise their store portfolio and will close further loss making stores in the coming year, reducing sales but improving profitability.

The rents at lease renewal over the past year have fallen by 27.2% which seems to be a remarkable result. The board still see opportunities to reduce rents and relocate to better sites and therefore continue to open larger, more profitable grade one stores while closing smaller grade three stores. The average lease length is now just 2.7 years which provides the group with some flexibility with secondary locations showing limited signs of rental recovery outside London. The group have also been trialling new equipment during the year to increase store densities without the need for refitting which so far have been successful and will rapidly increase the number of grade one stores in 2016.

Since the launch of the fully responsive upgraded website, the group’s customer database grew by 47% which has helped e-mail campaign sales increase by 65%. Conversion improved on all devices and overall e-commerce growth was significantly ahead of market expectations, growing by 44.7%. In addition to their own website, the group also sells via Amazon and eBay which represent some 40% of online sales. The group have now started selling to over 30 additional countries via Amazon and eBay and they will continue to increase the number of countries in which their products are offered. In addition, they are working on further developments over the next year that will improve delivery options for international customers on shoezone.com.

Trading in the first quarter of 2016 has been challenging amid the well documented high street trading conditions for apparel retailers. The stock position, however, is well controlled and they have achieved strong gross margins having chosen not to discount stock before Christmas, as usual. Capital investment for the full year will be increased to about £3M from the original £2M expectation to allow increased investment in stores, warehouse and IT. This includes refitting an additional ten stores, significant investment in the distribution centre to allow for increasing volume of e-commerce sales, and a roll out of new point of sale terminals which will be completed by 2018.

So far in the new year, the group have opened six new stores and refitted a further four. In August a trial project will be launched in three stores. These stores will be twice the size of an average grade 1 store. These stores will benefit significantly from an extended product range, higher priced footwear and an enhanced environment which will allow the group to benefit from the out of town market as well as creating a strong new avenue for growth. The falling oil price is already having a positive impact on the cost of logistics and should also impact the price of raw materials which should have a positive effect on margins in the coming year.

Trading in the first quarter of the year has been challenging, amid the well documented high street trading conditions for clothing and footwear retailers. Despite this we have continued to make progress against our strategic objectives whatever that means.

At the year-end the group had a net cash position of £14.2M compared to £9.1M at the end of last year. At the current share price the shares trade on a PE ratio of 11.7 which falls to 10.6 on next year’s forecast. Following the announcement of the special dividend of 6p, the shares are now yielding 8.3% which falls to 5.6% on next year’s consensus forecast – good stuff and the group have stated that they will pay excess cash over £11M to shareholders.

Overall then this has been a fairly decent year for the group although pre-tax profits did fall, net assets increased and despite a decline in operating cash flow due to a reduction in payables, cash profits increased and there was plenty of free cash generated. The 27% reduction in operating leases sounds really good and the group have indicated more could be to follow. In addition, the closure of the smaller stores and opening of the more profitable larger ones seems to be a good strategy. The e-commerce side of the business seems to be doing very well and with a forward PE of 10.6 and dividend yield of 5.6% these shares are looking rather good value to me.

Unfortunately they state that trading in Q1 has been challenging but don’t say quite how challenging it has been which is very frustrating and until I seem some brokers estimates, it makes this a difficult investment to make.