Telford Homes has now released its final results for the year ended 2016.

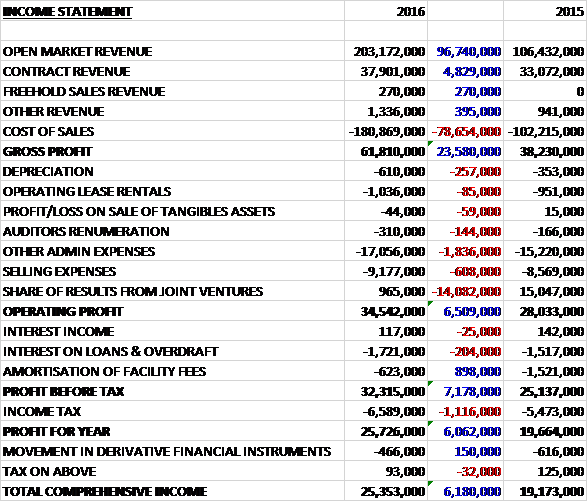

Revenues increased when compared to 2015 with a £96.7M growth in open market revenue and a £4.8M increase in contract revenue. Cost of sales also increased to give a gross profit £23.6M above that of last time. Depreciation was up £257K and selling expenses increased by £608K with a £1.9M growth in admin expenses. There was a £14.1M fall in the profit from joint ventures which meant that the operating profit grew by £6.5M. A £204K growth in interest on loans was more than offset by an £898K reduction in the amortisation of lending fees so that after a £1.1M growth in tax, the profit for the year came in at £25.7M, an increase of £6.1M year on year.

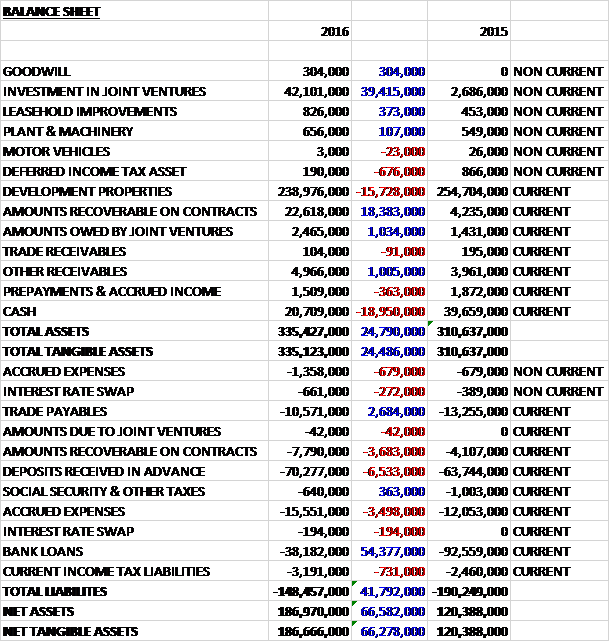

When compared to the end point of last year, total assets increased by £24.8M, driven by a £39.4M growth in investments in joint ventures relating to the acquisition of United Home Developments and the land purchase at Chobham Farm; and an £18.4M increase in amounts recoverable on contracts, partially offset by a £19M decline in cash and a £15.7M fall in the value of development properties. Total liabilities decreased during the year as a £54.4M fall in bank loans was partially offset by a £6.5M increase in deposits received, a £3.7M growth in amounts recoverable on contracts and a £3.5M increase in accrued expenses. The end result is a net tangible asset level of £186.7M, a growth of £66.3M year on year.

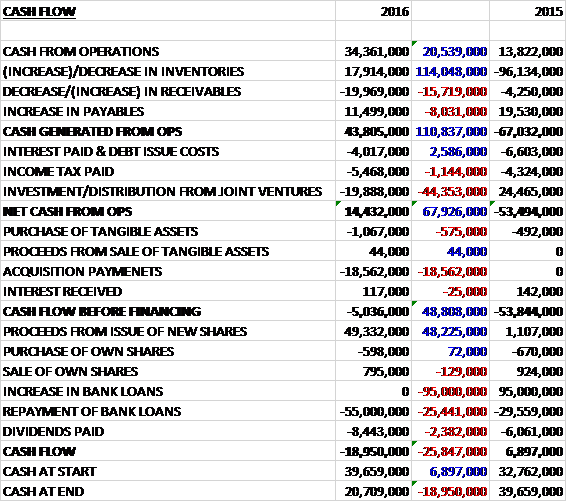

Before movements in working capital, cash profits increased by £20.5M to £34.4M. There was an inflow of cash from working capital compared to a large outflow last year so after interest costs fell, tax payments increased and there was a large investment into joint ventures, the net cash from operations came in at £14.4M, a growth of £67.9M. This did not cover the acquisition payments of £18.6M, however and after a £1.1M investment in other tangible assets, there was a cash outflow of £5M before financing. The group received proceeds of £49.3M from the placing and this was used to repay £55M of bank loans and pay £8.4M in dividends to give a cash outflow for the year of £19M and a cash level of £20.7M at the year-end.

Overall the number of completions increased from 374 to 482 but the average selling price of the properties reduced from £439K to £417K. This reduction was due to the mix of developments completing in the year in terms of their location and not an indication of a fall in underlying price.

During the year the group completed their first substantial Private Rented Sector (PRS) transaction with the sale of Pavilions for £66.75M to L&Q, one of the country’s leading housing associations. More recently they have also exchanged contracts on a second PRS sale of the open market homes at Carmen Street to M&G Real Estate for £63.2M in May 2016. These transactions are de-risking existing developments and mark the start of a new direction for the group in terms of customer mix and have the potential to become increasingly significant over the coming years. They are forward funding arrangements and involve regular payments during the construction process.

The transaction is accounted for as a construction contract and the group will recognise revenue on a percentage of completion basis over the life of the development with completion of the Pavilions transaction expected in mid-2018. This enables the group to recognise profits earlier than if the homes were sold on the open market. They are also forward funded by the investors which means an initial payment is made reimbursing the cost of the land then monthly construction payments and finally a substantial payment on completion. Very little equity is therefore used during construction but the transactions are at a moderately reduced margin.

The recent launch of the Liberty Building demonstrated that individual investor demand continued to be healthy. The group secured over £40M of future revenue across the launch in March and April with 68 of the 105 open market homes sold. A third of these were sold to UK investors and the remainder to international investors, particularly those from China. The development does not complete until 2019 and the average price achieved was around £900 per square foot, which is at the upper end of the typical price range and ahead of initial expectations.

In addition to the development specific launches throughout the past year, there have been more than forty sales with a combined value of over £25M secured through the new central sales and marketing suite in Stratford.

In total, the group exchanged contracts for the sale of 403 open market properties in the year and negotiated the contractual sale dates on a further 145 open market homes at City North which formed part of the acquisition from United House, which has effectively secured forward sales of more than £67M on this development, a joint venture with the Business Design Centre in Islington. In summary, the group have added 548 new sales in the year compared to 661 achieved last year.

The sales achieved in the year were split 28% to UK investors, 41% to overseas investors, 7% to owner-occupiers and 24% to institutional investors. This compares to 38%, 49%, 13% and 0% respectively in the prior year. The low percentage of sales to owner-occupiers is apparently down to the timing of sales and not a lack of demand. The group aspires to forward sell its developments to de-risk existing projects and investors tend to purchase much earlier in the development process than owner-occupiers. Despite recent tax changes, individual investors are expected to remain an important component of the group’s sales mix.

Since late 2014, sales prices have been tempered by affordability constraints and are now increasing at a more sustainable rate of 4-5% per annum, offset to some extent by overage payments to land vendors where they share in uplifted values. Build cost inflation has also been evident across the industry but has been controlled to a similar rate of increase and in accordance with forecasts. They group have still not experienced any significant shortages in supply in any of its subcontracted trades or materials.

The gross margin has reduced to 26.5% from 32.4% last time, although it remained above the 24% target. The board expected margins to trend towards this level given the similar rate of inflation of both prices and costs. PRS sales are also expected to reduce margins going forward.

During the year the group completed the sale of two smaller undeveloped sites for revenues of £6.7M. These sales are as a result of the change in strategic direction where smaller sites have become less attractive to build out.

On the 30th June the group acquired the regeneration business of United House Developments which consists of a group of companies that have various interests in four significant development opportunities in North and East London. An amount of £23M was paid which included an amount held in escrow relating to Gallions Quarter where completion is conditional on the business securing a legal interest in the site. The revenue and profit recognised since the date of the acquisition are minimal and not significant to the group.

In November the group issued 13,888,889 shares at 360p per share as a result of a placing which raised £50M before expenses. There is also headroom of £140M on the revolving credit facility. Immediately following the placing the group acquired the site in Carmen Street for £20M which was swiftly turned into a PRS sale in the following months. Many opportunities are being appraised and the board is confident of committing the remainder of the placing funds to site acquisitions before the end of the current year. Following the placing, the group has sufficient resources to fund its longer term growth plans.

In February 2016, the group appointed a new non-executive director, Jane Earl. She replaces David Holland who will retire in July after being with the group for fifteen years, including ten as Chairman.

The group started 2017 with a forward sold positon of £579M of revenue, up from £503M at the same point of last year. This will increase further as sales are achieved during the year and already represents more than double the total revenue reported last year. In total they have secured over 50% of the cumulative revenue expected in the next three years.

There have been some recent concerns over prime residential properties in London but this is a different market to that served by the group as they are focused on non-prime locations in London at a price point that continue to see strong demand. The board have a pre-tax profit forecast to exceed £50M by 2019 and the development pipeline now represents over £1.5BN of future revenue. The board expects 2017 to show no more than a slight improvement in profit compared to this year with substantial growth into 2018 and 2019 to become more than £50M by the end of 2019, ahead of previous expectations.

At the current share price the shares trade on a PE ratio of 10.1, reducing to 9.6 on next year’s consensus forecast which looks pretty good value. After a 28% increase in the total dividend, the shares are yielding 4.1% which increases to 4.6% on next year’s forecast.

Overall then this has been a strong year for the group. Profits were up, net assets increased (although the placing would have responsible for most of this) and the operating cash flow grew. Despite that, the group did not generate any free cash, however. Completions were up but the average selling price declined which is being put down to a change in product mix. The addition of PRS transactions mean that margins will come down but hopefully also mean that there is a healthier cash flow.

Investor demand at the price point where the group operate seems strong but they do seem to rely on Chinese investors, so the health of their economy is important. Build cost inflation seems to be being controlled well but the group had to rely on a placing to patch up its development cycle which is disappointing – I would much prefer companies to grow out of their own operational cash flow. Despite this, a forward PE of 9.6 and dividend yield of 4.6% seem good value and after the referendum outcome is known I might think about buying in here.

On the 23rd June, in a very well times sale just before the Brexit vote, Land Director James Furlong sold 100,000 shares at a value of £350K. It was also announced that group planning and design director sold 100,000 shares at the same value. James in now interested in 1,156,789 shares and David is interested in 1,192,357 shares.

On the 4th July the group announced that Land Director James Furlong purchased 48,917 shares at a value of £147K. This seems a canny trade considering he sold a chunk before the referendum result.

On the 14th July the group released a trading update. In recent months they have continued to build a substantial forward sold position, including £130M from two PRS contracts, and raised £50M of new equity. As a result they are in a strong financial position to manage the impact of market uncertainty following the Brexit outcome.

Total forward sales now exceed £640M which has been boosted by the PRS sales of the Pavilions, sold to L&Q in February; and Carmen Street, sold to M&G in May. As a result of these sales, the £50M of placing funds are largely uncommitted and in addition the group has significant headroom in its £180M revolving credit facility – one has to ask then whether the fundraising was necessary at all.

The EU referendum has created significant short-term uncertainty and it is too early to predict how long that will last. Due to the forward sold position, the group has now major sales launches planned until the autumn so they will monitor other market activity as a barometer of transaction levels and pricing. In addition, they continue to consider opportunities for further PRS sales, both on existing sites and potential land acquisitions.

Not really much to go on then – the group seems strong but it is too early to tell what effect the Brexit vote will have.

On the 29th July the group gave an update on the acquisition of the regeneration business of United House Developments. The group have completed the purchase of their interest in Gallions Quarter and have secured a £110M loan facility for its City North development. The purchase was deferred from the original acquisition of the regeneration business. The development is controlled by Notting Hill Housing Group and Telford has acquired a 50% interest in two of the phases to be developed. The first of the phases has a detailed planning consent for 292 new homes which are due for completion in 2020. The second phase, which will start after phase one has completed, has outline consent for a further 254 new homes.

The loan facility to finance the development of City North, a joint venture with The Business Design Centre, has been secured from the LaSalle Residential Finance Fund. This will provide funding for the mixed use development comprising 355 apartments and 109,000 square feet of retail, leisure and office space next to Finsbury Park station. The group have recently commenced work on site.

Since the acquisition the group has also made good progress on the other two developments purchased from United House. Planning consent has been secured at Balfron Tower, a 26 storey grade II listed building in Poplar consisting of 146 existing homes that being refurbished. In addition a planning application has been submitted for the regeneration of Chrisp Street market which, along with providing new homes, will transform the area around the existing market square into a new commercial and leisure destination.

On the 30th August the group announced that Land Director James Furlong sold 48,917 shares at a value of £156K. This is quite a heft sell and has been a very profitable trade.

On the 12th October the group released a trading update covering the first half of the year where they stated that they continue to hold a positive view of both the current and future housing market in non-prime areas of London and they have not revised their growth targets following the Brexit vote.

The group started the year with a substantial forward sold position that has subsequently exceeded £650M of revenue to be recognised in 2017 onwards. They have experienced increased sales activity in respect of residual availability across a number of developments. Since the start of September, greater interest levels and more visitors to the central sales centre have resulted in an increased number of reservations. This has included the sale of three of the remaining penthouses at Horizons where the average price is over £1M. The average price of open market homes in the group’s future pipeline is £517K.

The next significant launch will be City North in Finsbury Park, a joint venture development with the Business Design Centre which is planned for November. This development is now underway and the group recently announced the signing of a £110M loan facility with LaSalle which will fund this scheme of 355 homes, 140K square feet of commercial and leisure space and a new entrance to the underground station.

Build to Rent remains a significant focus for the group following the sale of the Pavilions to L&Q, and Carmen Steet to M&G. Following these two development sales, the group has recently progressed to detailed discussions on a third transaction. There has been a noticeable increase in institutional interest in these kinds of investments which complements the group’s desire to extend its involvement in the sector.

The group has an accelerated development pipeline as a result of the purchase of the regeneration business of United House in September 2015. They have resources to add to that pipeline and an increasing number of opportunities are being appraised with some sites now the subject of more detailed negotiations.

There were far fewer open market completions in the first half of this year compared to the first half of 2016 due to development timings despite completions proceeding with no unexpected delays. As a result of this, profits in the period will be lower than last year but in line with expectations. To date the group have secured 95% of the open market homes expected to complete this year and 87% of the gross profit expected in the year. The board’s expectations remain unchanged.