Trifast has now released its final results for the year ended 2016.

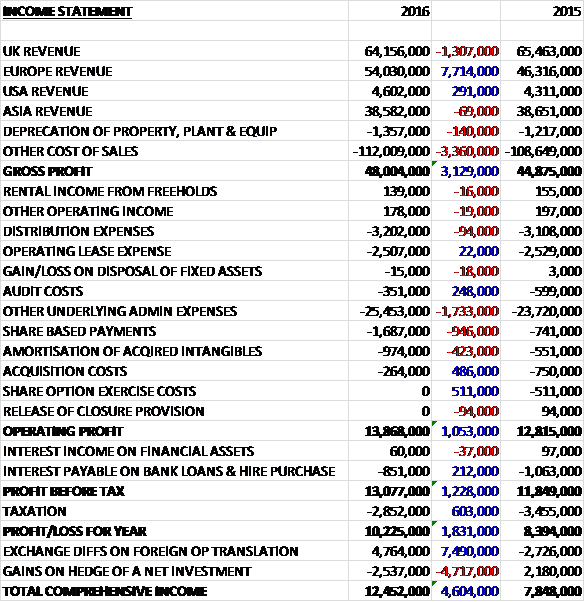

Revenues increased when compared to last year as a £1.3M fall in UK revenue and a small decrease in Asian revenue was more than offset by a £7.7M growth in Europe revenue and a £291K increase in USA revenue. Depreciation was up £140K and other cost of sales increased by £3.4M to give a gross profit £3.1M above that of 2015. Distribution expenses were up £94K and audit costs were down £248K with other admin costs increasing by £1.7M. Share based payments increased by £946K and the amortisation of acquired intangibles grew by £423K but acquisition costs fell by £486K and share option exercise costs were down £511K to give an operating profit £1.1M above last year. Interest costs were down £212K and tax expenses fell by £603K as a deferred tax asset in the US is now considered recoverable which meant that the profit for the year was £10.2M, a growth of £1.8M year on year.

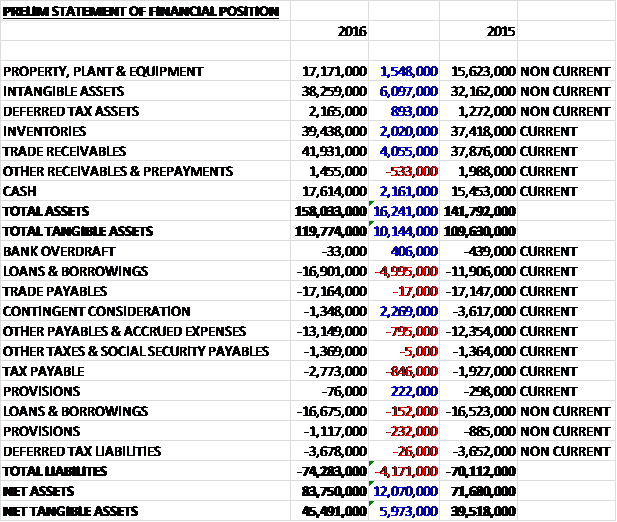

When compared to the end point of last year, total assets increased by £16.2M driven by a £6.1M growth in intangible assets, a £4.1M increase in trade receivables, a £2.2M growth in cash and a £2M increase in inventories. Total liabilities also increased during the year as a £2.3M decline in contingent consideration was more than offset by a £5.2M growth in loans and borrowings. The end result was a net tangible asset level of £45.5M, an increase of £6M year on year.

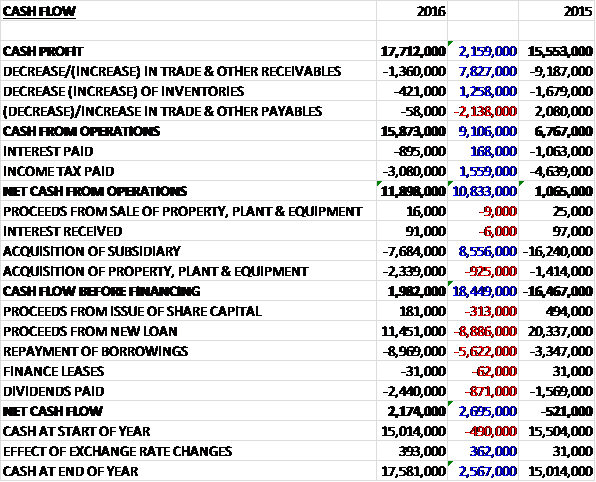

Before movements in working capital, cash profits increased by £2.2M to £17.7M. There was a cash outflow from working capital, but this was much less than last year with a much smaller increase in receivables. After tax payments fell by £1.6M, the net cash from operations came in at £11.9M, a growth of £10.8M year on year. The group spent £2.3M on property, plant and equipment, mainly related to increasing capacity in Malaysia, Taiwan and Italy, along with £7.7M on acquisitions to give a free cash flow of £2M which did not quite cover the £2.4M of dividend payments. A net £2.5M increase in loans meant that the cash flow for the year was £2.2M and the cash level at the year-end was £17.6M.

The underlying profit in the UK business was £5.9M, a growth of £370K year on year with revenues down modestly reflecting a slight softening of demand. The growth in margins are due to forex translation gains and ongoing operational efficiencies. The underlying profit in the Europe business was £6.8M, an increase of £437K when compared to last year. Gross margins declined from 28.2% to 26.5% in the region, however, due to unfavourable forex movements.

The underlying profit in the US business was £399K, an increase of £73K when compared to 2015 on operating margins that increased from 7.6% to 8.7%. The underlying profit in the Asia business was £6.7M, a growth of £1M year on year. In Singapore, revenue growth has been very strong at 9.4%, reflecting a significant growth in the domestic appliances sector. In contrast, the Malaysian operations have struggled against a backdrop of falling customer demand and domestic market weakness with revenues decreasing by 8.3%. There was a strong margin improvement in the region due to capacity increases, particularly out of Singapore.

The biggest driver of organic growth has come from multinational OEMs, contributing 3% to organic revenue growth. On the non-organic side, growth reflects the first full year of trading from VIC, acquired in May 2014, and the first six months of trading from Kuhlmann, acquired in October 2015. Both acquisitions are preforming welk. VIC has achieved over 13% revenue growth year on year and Kuhlmann is slightly ahead of expectations in its first six months, with revenue up over 12%.

The year saw significant investment across the Asian manufacturing sites with capacity increases of 15% in Taiwan and the introduction of a new £1M parts former in Malaysia. The site in Hungary has also increased storage capacity by acquiring the warehouse adjacent to their current building. Looking ahead, plans are in place to enhance manufacturing capability in Italy via the introduction of a new heat treatment line. This will allow the group to produce more product in house and better manage lead times. Further digital investment to improve access to business and management information is also planned over the next two years. In addition, a two year project to rebuild and enhance the trading website was completed in February.

In October the group acquired Kuhlmann for a total consideration of £6.2M. The initial amount of £4.9M was paid on completion in cash and consideration of £1.3M is deferred for a year and is to serve as a retention against which any potential warranty and indemnity claims will be offset. The business is a distributor of industrial fastenings within the domestic German market. It has a long standing customer base in machinery and plant engineering, sheet metal processing and industrial markets. The management team and previous owners will continue to run the business and last year it generated a pre-tax profit of £1.4M. The acquisition generated goodwill of £1.2M and in the six months since acquisition, it contributed £500K of operating profit, which would have been £600K had the business been acquired at the start of the year – this looks like a good value acquisition to me.

In the UK, after a good start to the year, there was a slight softening in customer demand. There was a marginal improvement in Q4 with higher sales starting to come back through at the Scotland and Uckfield sites and Belfast continued its rapid growth phase for the second year. The transactional and EU distributor sales teams have also enjoyed growth this year, although some margins were impacted through foreign exchange.

The recent efficiency consolidation of sites in Uckfield, Pool and the Midlands along with the roll-out of Lean-lift technology has continued to improve profitability which, couple with a forex gain, has led to a 70 basis point increase in the underlying operating margin year on year. A roll out programme is planned for installing further Lean lifts into the hubs. Through “Dead space” utilisation and a reduction in travel and picking time, this should allow them to grow the business without the need for extra premises or people.

In Europe, sales growth has been strong across a number of locations, most specifically in Holland and Sweden where revenues increased more than 10%. In both cases, this growth has been largely driven out of additional sales to multinational OEMs in the automotive sector and is a good example of how the core organic strategy of focusing on their multinational OEM customers is producing results.

VIC has continued to outperform management expectations in terms of organic revenues with an increase of 13% on the previous year. With virtually all of this additional revenue coming through from the domestic appliances sector, this ongoing trend is helping the group to maintain a balanced sector split. Non-organic growth has driven 14% of the revenue increase. This is made up of additional sales of £4M arising in VIC in April and May 2015 and the first six months of trading in Kuhlmann generating revenues of £2.5M.

The fall in underling operating margins from 14% to 12.7% has been largely the result of gross margin reductions in the Euro/USD exchange rate. Across the rest of the region, margins have remained broadly in line. Looking ahead, Europe continues to provide a key opportunity for growth, both in terms of ongoing development of the existing businesses and from potential future acquisitions with hotspots already identified in Spain and Eastern Europe.

The group are starting to see the impact of more positive movements in the Euro/US dollar exchange rate. If this situation continues then this should benefit gross margin improvements in Europe in the coming months.

In the US the group has seen growth in the automotive sector with the team in Houston making good inroads into building local relationships with top Tier 1 automotive customers based in the US. A second driver to future growth will be Mexico.

In Asia, the group witnessed a series of changes to trading conditions in the region with oil price reductions, concerns over the Chinese economy and a sharp downturn in the strength of the Asian currencies towards the end of the first half. Despite these unsettled external conditions, however, the region has experienced strong growth, particularly in the domestic appliances sector.

TR Formac in Singapore has seen the largest revenue growth at 9.4% coupled with a gross margin increase. This result has been mainly driven out of additional sales to their multinational OEM customers and increased capacity. The micro-screw, self-clinch fastener and complex part products have earned awards. PSEP in Malaysia, in contrast, had a slower year due to weak domestic demand and a highly competitive domestic automotive market. Revenues have fallen by 8.4%, although underlying operating profits have remained broadly stable reflecting a strong level of cost control.

SFE in Taiwan continued to grow with support from Europe and the US. Trading levels have increased by 4.1% and underlying operating margins also improved. Across the rest of the region, amongst the distribution businesses in Shanghai, India and Thailand, there has been some reduction in trading levels. This is predominantly due to a slower than expected production start at one of the key multinational OEMs in the automotive sector. Excluding this, there has not been any significant impacts coming out of the reported weakness in the wider Chinese economy.

The opportunities for growth across the region remain positive. The investment in to additional capacity at the Taiwanese factory is already delivering results with the growth they have seen in 2016. The £1M investment in a parts former at PSEP is complete, so they are expecting to see further capacity utilisation starting to flow through in the coming year. Looking beyond organic growth, Asia is a region of interest for potential acquisitions. As a result, at both a group and local level, they continue to actively identify and review acquisition opportunities as they arise.

CEO Jim Barker retired at the end of September and he was replaced by CFO Mark Belton. Clare Foster took over as CFO having joined the company in January 2015 as group financial controller having previously been at KPMG for over 16 years. The group are in the process of agreeing new banking facilities which will increase available funds by £5M and an accordion facility of £20M is being written into the agreement for further acquisitions – debt reduction is certainly not a priority here then.

Going forward, the enquiry pipeline is strong, whist the strategy of focusing on multinational OEMs looks set to continue to deliver growth. 2017 will be the first full year of trading from Kuhlmann and the board are already starting to see opportunities coming through as a result of the acquisition. There are some macroeconomic factors outside their control, such as the ongoing volatility in forex and raw material markets but they are optimistic for the year ahead.

Investments being made to increase capacity and the focus on making better use of existing capacity, specifically in the Malaysian sites, should start to impact positively on results in the next year. The investment in the UK business, in to both senior sales staff and driving operational efficiencies, is expected to continue to build on profitability in that region.

At the year-end, net debt stood at £16M compared to £13.4M at the end of last year. At the current share price the shares are trading on a PE ratio of 16.5 which falls to 13.4 on next year’s consensus forecast. After a 33% increase in the total dividend, the shares are now yielding 2% which increases to 2.1% on next year’s forecast.

Overall then this has been a strong year for the group. Profits increased, net assets were up and the operating cash flow improved, generating a decent amount of free cash, albeit not enough to cover the dividend. All business regions seem to have performed well although the improvement in the UK was due to cost savings rather than demand increased and the local market in Malaysia has been poor. The acquisition seems to be a really good fit to me, and at a decent price.

The debt levels are a little concerning but a forward PE of 13.4 looks decent value for such a quality company. The dividend yield of 2.1% is not too bad either and I am tempted to buy some shares once the Brexit vote is known.

On the 26th July it was announced that European MD Geoffrey Budd sold 75,000 shares at a value of just under £100K. He still retains 232,264 shares but this is not a great vote of confidence!

On the 27th July the group released a trading update at the AGM. Current trading across all regions remained in line with management expectations and they remain on track with their organic growth performance and capital investment objectives for the current year, although current forex conditions present an operational challenge. Not much to go on then, but this seems like an OK update.

On the 4th October the group released a trading update where they stated that the business remains solidly on track in terms of its organic growth performance and capex objectives despite widespread general economic concerns arising from Brexit. Three months since the Brexit vote, the positive trend dynamics for TR have been reassuringly sustained resulting in their business units across the group experiencing continued good organic growth on a constant currency basis. At the end of the period, they have settled the deferred consideration payment of €1.7M due to the owners of Kuhlmann.

Over half of the group’s revenue is derived from outside the UK, therefore their reported financial results are impacted by the effects of forex movements and during the period, they have benefited from a tailwind from the weakness in Sterling.

This month they have expanded their European presence, opening a greenfield distribution and technical centre in Barcelona with its operational focus on the Tier 1 automotive sector.

This all sounds rather reassuring and I am happy to continue holding.