Vertu has now released its final results for the year ending 2015.

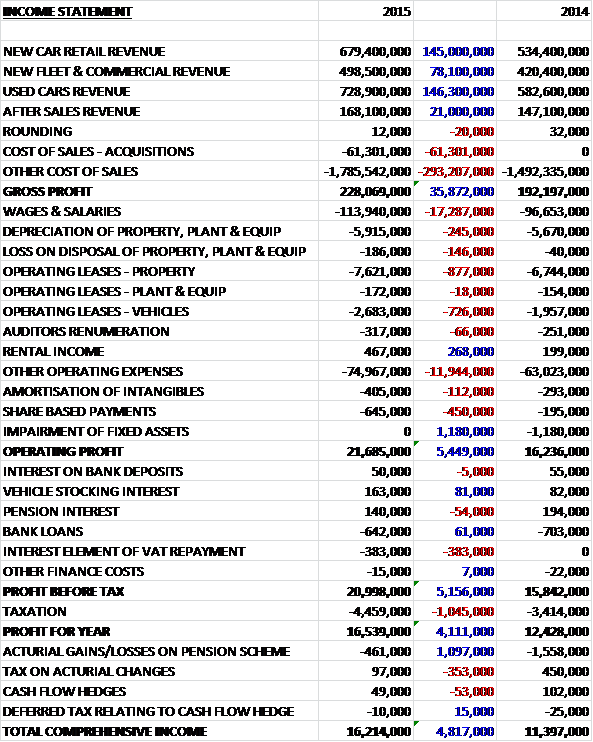

Revenues were up across all business sectors with new car retail up £145M, new fleet and commercial up £78.1M, used cars up £146M, and after sales up £21M. We also see cost of sales increase to give a gross profit some £35.9M ahead of last year. Most operating expenses increased, with wages up £17.3M due both to increased commissions on higher sales and a growing headcount, and “other expenses” up £11.9M, with advertising expenditure increasing by £1.4M and operating leases increasing by £1.6M, although there was no impairments this year which accounted for £1.2M in 2014, but there was a £383K charge relating to HMC that did not occur last time and tax costs were over one million pounds higher to give a profit for the year of £16.5M, a £4.1M increase when compared to last year.

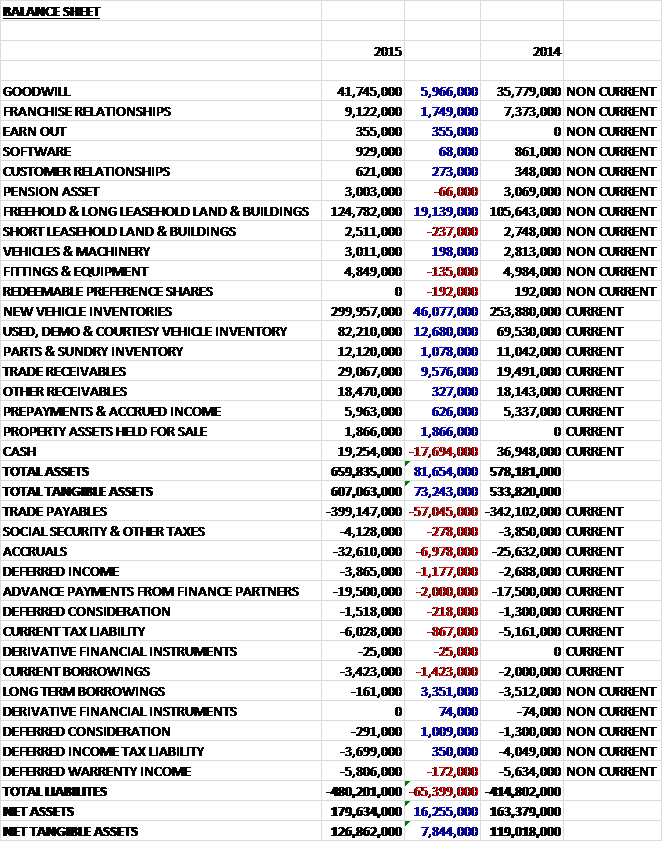

When compared to the end point of last year, total assets increased by £81.7M driven by a £46.1M increase in new vehicle inventory, a £19.1M growth in the value of property, a £12.7M increase in used car inventory and a £9.6M increase in trade receivables, partially offset by a £17.7M crash in the cash level. Liabilities also increased with a £57M growth in trade payables and a £7M increase in accruals (partly relating to outstanding service plans) being offset by a £1.9M decline in the value of borrowings. The end result is a £7.8M increase in net tangible assets to £126.9M which looks like a very healthy balance sheet, although it is worth remembering that there are outstanding operating leases totalling £81.5M that are off the balance sheet.

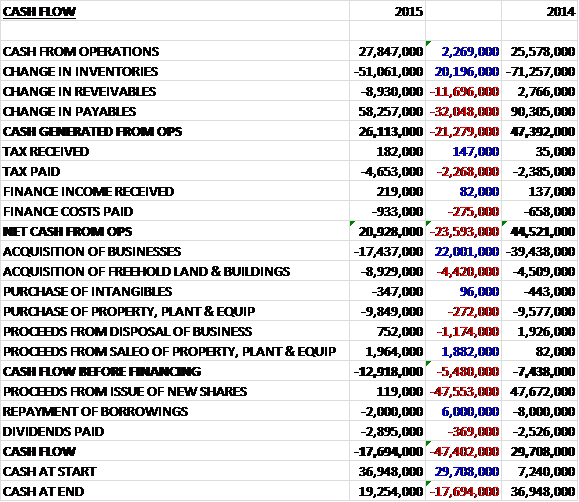

Before movements in working capital, cash profits increased by £2.3M to £27.8M. Changes in working capital broadly cancelled each other out, as increases in receivables and inventory due to the growth of fleet and commercial operations were offset by higher levels of receipts from service plan and warranty customers, although payables increased at a slower rate than last year so that cash generated from operations was £21.3M lower at £26.1M. After tax and finance costs, the net cash from operations stood at £20.9M. This was enough to cover the buildings acquired and other capital expenditure but could not cover the £17.4M spent on acquiring new businesses so that before financing, the cash out flow was £12.9M. After dividend payments and the repayment of loans, the cash outflow for the year stood at £17.7M to leave a cash pile of £19.3M at the year end. This is still a considerable amount of cash but it seems the group will eat through last year’s £47.7M raised through new shares in a couple of years which is a bit of a concern and it must also be pointed out that due to the timing of year end, the cash reserves are some £20M higher than during the majority of the year, so it starts to look a little less comfortable.

Market conditions in the UK continued to be buoyant due to improving consumer confidence and continued attractive finance offers from manufacturers. The rate of growth did slow somewhat, however, as was predicted. During the second half of the year, as sales started to slow, it became apparent that there were higher levels of self-registration by retailers that created a disconnect between the actual sales of vehicles to private customers and vehicle registrations. The self-registered vehicles are then sold to the market as used cars. Due to the strength of Sterling against the Euro and the relatively buoyant economic conditions in the UK, the country remains the market of choice in Europe for car manufacturers. Equally, improving economic conditions and the rise of online shopping has created a robust commercial vehicle market in the UK with registrations rising 12% last year.

New car retail and motability recorded a gross profit of £50.9M, an increase of £10.1M when compared to last year, although gross margin fell from 7.6% to 7.5%. New retail car volumes rose by 6.4% in the year on a like for like basis compared to an increase of 8.4% in the market as a whole but the board considers that the shortfall is explained by the registration data reported in the market figures including self-registered vehicles by retailers and manufacturers when the group’s sales volumes excludes them. Volumes of sales on the Motability Scheme rose by nearly 11% on a like for like basis against a 6.3% increase in the market. This performance is due to an increased focus of the sector and the fact that the group was awarded Motability Dealer of the Year in 2014. The sales in this category have a near 100% retention into service operations in the three years following the sale so despite the low margins, the growth in sales should auger well for future aftersales profitability. The profit per unit of new cars increased during the year from £12,170 last year to £13,639 by the second half of this year which was due to the change in unit mix towards higher-end vehicles as the year progressed.

New fleet and commercial recorded a gross profit of £12.3M, an increase of £2.1M when compared to last year on a margin that increased slightly from 2.4% to 2.6%. Like for like car fleet volumes rose by 16% with a similar increase seen in light commercial vehicles which reflected market share gains against a market that increased by 12%. These improvements were obtained due to the increased number of dealership based local business specialists and prior year acquisitions which have gained traction.

The used car business recorded a gross profit of £75.5M, an increase of £12.3M when compared to last year on a margin that declined from 10.8% to 10.4%. Used car volumes increased by 16.6% in total and 9.2% on a like for like basis, which was ahead of the market as a whole. The UK used car market was stable during the first half of the year with constrained supply leading to stable prices and margins but in the second half of the year the market returned to a more typical seasonal depreciation cycle due to retailer self-registration and an increase in the supply of nearly new vehicles which compete with competitive finance-led new vehicle offers. Additionally, rising new car sales increased the general supply of used cars in the market so for the first time since 2009, the market is no longer supply constrained which reduced the margins achieved in the second half of the year.

The margins were also affected by the higher value vehicles on offer in the new JLR dealerships which have higher selling prices but consequently lower margins as a percentage of purchase price. Indeed on a like for like basis, margins improved from 11.5% to 11.6% with an increase in the first half of the year offset by a decline in the second half. With the supply constraints now lifted, it is likely that margins will come under further pressure but volumes of sales should rise.

The aftersales business recorded a gross profit of £89.4M, an £11.4M increase when compared to 2014 on a margin that increased from 43.1% to 43.5%. The increase in margin is due to an increased focus on “technician” efficiency and higher volumes in the vehicle health check process, which seeks to ensure that all customer vehicles visiting the dealerships were given a full mechanical health check by a technician who identifies any service work which may be required. The group now has over 71,000 customers who pay monthly for service and MOT via the three year service plan product, which is a good increase from the 55,397 achieved last year.

The accident repair sector experienced another year of stabilisation and there is evidence that industry capacity restrictions have led to a greater balance in supply and demand in the sector with the group’s accident repair revenues growing by 5.5% on a like for like basis on incredible margins that increased from 65.6% to 65.8%. There are now nine accident repair centres in the portfolio. Supply of manufacturer parts saw revenues rise 2.9% on a like for like basis on a stable margin – parts represent about 27% of total aftersales profits. Due to the fall in petrol prices, there was a 5.4% decline in like for like petrol forecourt revenues but stronger margins saw profits rise by £100K.

A strong part of the group’s strategy is to try and turn around failing dealerships by implementing their own processes and customer service offering, of which they seem rather proud. They were recognised within Honda and Hyundai for having amongst the best UK dealerships in those brands for customer service and the Darlington Nissan outlet has won the best large dealership award in the Nissan franchise. Many of the acquisitions undertaken in recent years have still to reach maturity in terms of performance enhancements which provides the opportunity for margin improvements and profit growth over the medium term. Operations deemed not able to meet return on investment hurdles are identified and either closed, disposed of or refranchised.

In line with the group’s strategy to expand through acquisition, there have been a number of business buys this year. In May they acquired Hillendale, which operated a Land Rover dealership in Lancashire and a Jaguar dealership in Bolton for a total consideration of £8M, £6M through cash and the remainder from the issue of shares. The acquisition came with £2.9M of net assets, £1.7M of which were intangible so it cost £5.2M in goodwill. The dealerships are profitable and if the acquisition had taken place at the start of the year, profits would have increased by £393K. The group also acquired the Taxi Centre & Easy Vehicle Finance for a total consideration of £2.1M, £1.5M of which was satisfied in cash, £400K through an earn out arrangement and £200K in shares. The business sources vehicles for private operators in the taxi sector. The acquisition generated just £807K in goodwill and had it taken place at the start of the year, would have contributed £229K in earnings, so this seems to be a good deal.

In November the group acquired four Ford dealerships – Bolton, Wigan, Horwich and Walkden for a total consideration of £11M, £109K of which was deferred. This acquisition generated no goodwill as the group paid the market price for the assets. Additionally, they acquired Addison Motors with Alfa Romeo, Chrysler, Jeep and Fiat franchises in Newcastle; 3e Autos, operating a Renault repair centre in Nottingham, and a Nissan dealership in Halifax for a total consideration of £1M satisfied in cash. The group also disposed of a Nissan dealership in Altrincham for a consideration of £752K which relates roughly to the fair value of net assets disposed of.

It seems that there is likely to be higher capital expenditure next year as the group has capital commitments in respect of property, plant and equipment amounting to £7.6M compared to just £1.5M at this time last year. The group has also indicated that it will continue to acquire dealerships across the volume and premium spectrum as the board continues its growth strategy.

The group has a decent amount of undrawn bank facilities available to it with an overdraft of £5M, a CMML facility of £30M and a loan facility of £15M. After the year end, the group refinanced its borrowing facilities by converting the £15M acquisition facility into a £20M facility that can be increased to £40M with the overdraft and other facilities increasing from £35M to £45M. Other changes that occurred after the balance sheet are that the group sold its only Suzuki dealership, based in Mansfield in order to have greater scale relationships with manufacturers (the outlet is currently being refurbished and will open as an additional Renault/Dacia dealership) along with one of the peripheral sales outlets of the Bolton Ford business acquired this year, in addition to a small Peugeot sales outlet in Ilkeston – there were no significant costs associated with these disposals. Additionally, the group disposed of the second peripheral freehold sales outlet acquired with the Bolton Ford business for a consideration of £700K which is equal to the net book value of the property. Finally, the group acquired the Bradford Jaguar outlet from Jardine Motors for a consideration of £900K including goodwill of £750K; and Bury Land Rover from Pendragon for a consideration of £7M, all of which was goodwill. The consideration was settled from existing cash resources.

Ford is the largest franchise partner to the group in both profit terms and number of outlets, with 22 currently in operation and Vertu is the 3rd largest Ford dealer in the country. This year, the group acquired four new outlets in Lancashire, two of which have subsequently been closed. The manufacturer is rolling out 65 Ford stores in the UK which will be large scale dealerships selling the full range of products including the Vignale premium product and the iconic Mustang. This year the group will open its initial Ford stores in redeveloped existing dealerships in Kent, Birmingham, Gloucester and Bolton. During the year the group completed the rebuilding of its Durham Ford dealership. The £2.3M investment significantly increased the sales potential of the dealership and further significantly redevelopments are planned in 2015 at Birmingham, Shirley and West Brom in order to further grow sales at these locations.

The Nissan franchises represent an increasing proportion of the group’s profitability, with 10 sales outlets now in operation. Vertu is now the sole Nissan partner in Glasgow with two outlets and there are plans to build a landmark Nissan dealership in the coming 18 months. In the past two years, the group has acquired five VW dealerships in the East Midlands and capital expenditure in these dealerships to expand showroom capacity and implement latest manufacturer standards is ongoing. Lincoln and Boston were completed during 2014 with the remaining three in Nottingham and Mansfield to be completed during the current year. The group currently operates a multi-franchised Renault, Dacia and Hyundai dealership in Exeter and due to increased sales volumes, they are relocating the Hyndai outlet to a separate dealership in a new freehold property which will cost £2.3M.

During the year, the group also saw the purchase and lease of additional properties next to the Waltham Cross Vauxhall operation at a cost of £1.1M which is facilitating a wider redevelopment of the dealership providing additional showroom, workshop and used car sales display capacity which will be complete by September. Early this year, two new outlets were opened in one location in Nottingham and the group now operates a Renault/Dacia outlet along with a Honda Motorcycle dealership. At the moment there are a number of manufacturers simultaneously requiring investment which did not take place during the financial crisis which means that capital expenditure is currently running at high levels and will fall back to much lower levels in due course.

Other infrastructure investment includes a significant support centre in Gateshead which operates activities such as service booking, sales enquiry management and customer experience activities (whatever they are). Previously these activities were spread across three different locations but a single office building was acquired for £1.5M which will enable to the group to consolidate into one location, thereby saving on costs and it should be opened by June this year. Another important area for investment is online functionality, for example the group has installed online chat in order to help customers any time of day and the website is regularly ranked in the top two for visitors which suggests the group has a good handle on digital marketing.

Capital expenditure this year included £7.3M in respect of the purchase of property for dealership development projects, £7M for refurbishment projects, £1.6M for the new support centre property and £3.3M on IT and other ongoing capital expenditure. In the coming year the group expects to pay £9.8M on current dealership redevelopment projects and £12.8M on new dealership developments so substantially more than this year, although there are five surplus properties with a book value of £4.8M that could bring a bit of cash in if sold.

Trading after the year end has been good, ahead of both the current year financial plan and the same period of the prior year with like for like sales volumes increasing by 4.3% against a figure of 2.7% in the market as a whole for sales to private buyers with stable margins. Group fleet and commercial new vehicle sales delivered improved profitability due to strengthening margins, and the market continues to show significant growth in volumes year on year. Like for like used retail volumes were up 6.2% in the post-year end period despite the impact of cheaper, finance-led new car offers but as with the second half of the previous year, increased availability has led to softening margins, declining from 10.8% to 10.4%, although the increased volume has more than made up for this with regards profits.

After the year end, group aftersales profitability increased on a like for like basis due to higher revenues and margins, with the overall margin increasing from 44.9% to 46% with service, accident repair centres and parts all showing both revenue and margin improvements. Petrol forecourt sales declined due to the falling fuel price but margin again increased. Service like for like revenues rose 7.2% in the post year end period and continued to benefit from the successful customer retention initiatives being executed by the group with over 71,000 customers now paying monthly for service and MOT service plan packages. Given this encouraging trading at the start of the year, the board is confident that the group will grow profits and the business again this year.

At the year end, net cash stood at £15.7M compared to £31.4M at the end point of last year. The shares trade on a P/E ratio of 12.5 which falls to 10.8 on next year’s estimates, which indicates the shares are in value territory whilst the dividend yield currently stands at 1.8%, which after increasing by 31% this year, is not spectacular but not bad for a growing business, with 2.1% expected next year.

Overall then this seems like a good update. Profits are up, as are net assets with inventories increasing considerably on last year, although this should be put in the context of the £47.4M raised in last year’s placing. There is a decent amount of free cash flow but this is nowhere near enough to pay for all the acquisitions and the cash levels start to look less attractive considering they are some £20M higher due to the timing of the March plate change. There is some concern that the new car sales seem to be behind the market as a whole but this is explained by the fact that Vertu does not include any self-registrations in its figures. The fall in margins is not a concern in new cars as this is caused by the higher value vehicles being sold in the newer dealerships, with earnings per car up. The lower margins in the used car business could be more of a concern, though, with the fall due to the increase in supply. The aftersales business continues to be strong and should get stronger with the warranties sold with the higher used car sales.

The shares only trade on a forward P/E ratio of 10.8% and there is a decent 2.1% prospective dividend on offer here but my issue with this company is that its continued expansion rate is not sustainable with the current cash pile probably disappearing by this time next year and with the increased capital expenditure already flagged up, I would not be surprised if the group will have to come back to investors for more cash in order to sustain its growth rate. If the company was expanding using its own funds then I think this share would be a definite buy but it does seem a bit risky as things stand, without even considering what might happen should the UK economy take a dive and people stop buying cars.

On the 13th May the group announced that Kenneth Lever will join as non-executive director. He has held senior executive roles at Alftred McAlpine and Tomkins and was CFO at Numonyx in Switzerland, he has also been CEO of Xchanging and will replace David Forebes.

On the 13th May it was announced that Chairman Peter Jones purchased another 125,000 shares at a cost of £73.5K so that he now owns 1,125,000 shares in the company which seems a good statement of confidence.

The share price has been generally range bound for the past year, can it gain enough momentum this time in order to break out?

On the 23rd July the group released a statement covering the first four months of the year. They saw continued growth in like-for-like revenues and gross profits, both from the vehicle sales and aftersales activities. The profitability in the period was strong and head of last year. It is expected that the trading performance for the year as a whole will be in line with market expectations.

There have been a number of acquisitions and disposals during the period. In June, the group acquired Blacks Autos which operates a Skoda dealership in Darlington. This is their first Skoda dealership and operates out of a leasehold premises adjacent to the current Darlington Nissan business. The total consideration came to £1.5M and included £750K of goodwill. Last year the dealership made a pre-tax profit of £372K so this looks like an excellent deal to me.

In July the group disposed of its Dunfermline Peugeot dealership, selling the assets to Eastern Western Motor Group. The dealership made an operating loss last year of £200K from revenues of £6M. Also the group sold a vacant property in Crewe for £1.1M which equates to the book value of that property.

All in all a decent update and things continue to run smoothly by the look of it.

On the 1st September the group released a trading update covering the first five months of the year. Overall, the board believes that results for the year as a whole will be in line with expectations. The group’s like for like new retail sales volumes to private customers grew by 0.4%. This was below the reported market registration levels that grew 1.5% for the franchises represented by the group and 2.9% as a whole, as they do not include pre-registered vehicles that are included in the official figures. The group’s like for like new retail vehicle gross profit per unit strengthened during the period.

The group increased like for like Motability sales by 6.4% during the period, gaining market share in this market with total UK sales volumes of vehicles under the Motability scheme declining by 1% during the period. Motability volumes represented 21.6% of the group’s total net car retail during the period which sounds like a lot. Although the margins on these sales are not high, these customers provide very high levels of aftersales retention during their three year contract.

The UK commercial van market continues to perform very strongly with total market registrations up 18.8% in the period. The group’s like for like van sales performed even better than the market, increasing by 22.9% on stable margins. Following a shift in sales mix with reduced supply to lower margin channels, the group’s like for like fleet car volumes fell by 6.7% but with an improved gross profit per unit.

The strong supply push characteristics of the UK new vehicle market over the last three years have resulted in an increase in the supply of vehicles to the used car market. This has grown the newer element of the vehicle parc and increased supply, competing with highly attractive finance led offers for new vehicles which has caused the market to return to more normalised seasonal depreciation of used vehicles. In the period, the group saw like for like sales volumes grow by 4% with like for like gross profit per vehicle declining modestly in line with the board’s expectations.

During the period, the group increased like for like aftersales revenue by 3.8% and gross margins from 44% to 45.7%. In the high margin service area, like for like revenues increased by 6.4%. Increased sales of service plans have yet again improved customer retention into the service channel but lower margin fuel sales through the group’s forecourts declined with fuel prices, muting overall aftersales revenue growth but strengthening margins due to a more favourable mix.

So far, like for like new car retail orders for September are up on last year’s levels which gives the board confidence for a successful conclusion to this critical month. Overall, the UK economy continues to grow, the UK consumer is spending and cars are very affordable so the macro signals all look good for car retailers generally.

This is a decent update from Vertu, the new car sales continue to be disappointing but the all-important aftersales seem to be doing well with the higher margin areas growing nicely. It looks as though used car profitability is declining somewhat but this seems to be in line with the market. This does seem like a decent company to me but as I already own shares in Cambria Autos I don’t think I will be jumping in here too.

On the 1st October the group announced the acquisition of SHG Holdings which operates Audi, VW passenger cars and VW commercial outlets in Hereford. The acquisition introduces Audi and VW Commercials to the group as a new franchise. In addition, the business also includes two VW group parts distributions operations in Hereford and Gloucester along with a used car and aftersales facility in South Herefordshire. Prior to this transaction, VW accounted for about 6% of group turnover and but it will increase to 9% going forward.

The consideration paid is £12.8M which has been settled in cash from existing resources. Further consideration of £1.5M is deferred for two years and will be payable under certain conditions. The business comes with net assets of £4.3M and generated profit before tax of £1.5M last year so the board expects it to be earnings enhancing in its first full year of ownership. The price paid for this doesn’t look too bad but expanding into VW sales is an interesting move given the current scandal surrounding the car maker.