Vertu has now released their interim results for the year ending 2018.

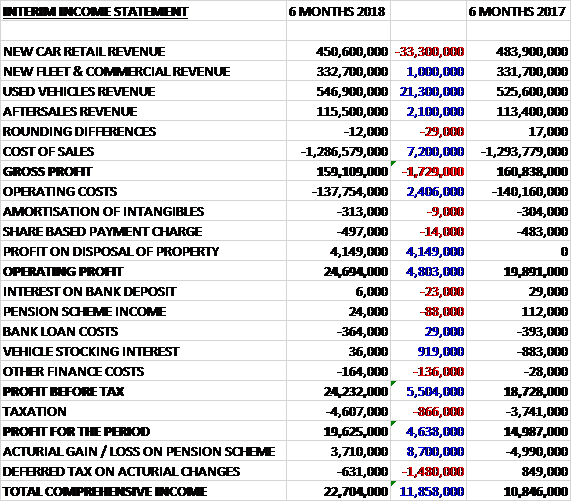

Revenues declined when compared to the first half of last year as a £21.3M growth in used vehicle revenue was more than offset by a £33.3M decline in new car revenue. Cost of sales also reduced but not enough to stop the gross profit falling by £1.7M. The group did manage to reduce operating costs by £2.4M, however, due to lower numbers of sales executives and less marketing, and after the £4.1M profit from the sale and leaseback the group saw operating profit rise by £4.8M. We then see a £919K positive movement in vehicle stocking interest, offset by an £866K increase in tax to give a profit for the period of £19.6M, a growth of £4.6M year on year or a £489K increase excluding the property sale.

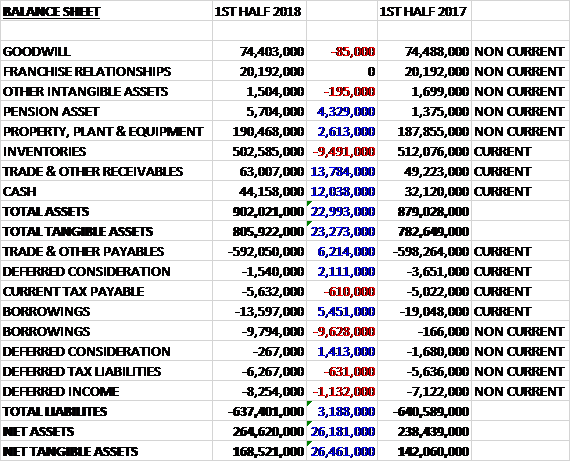

When compared to the end point of last year, total assets increased by £23M driven by a £13.8M growth in receivables, a £12M increase in cash, a £4.3M growth in the pension asset and a £2.6M increase in property, plant and equipment, partially offset by a £9.5M decline in inventories. Total liabilities declined during the period as a £4.2M growth in borrowings and a £1.1M increase in deferred income was more than offset by a £6.2M decrease in payables and a £3.5M fall in deferred income. The end result was a net tangible asset level of £168.5M, growth of £26.5M over the past six months.

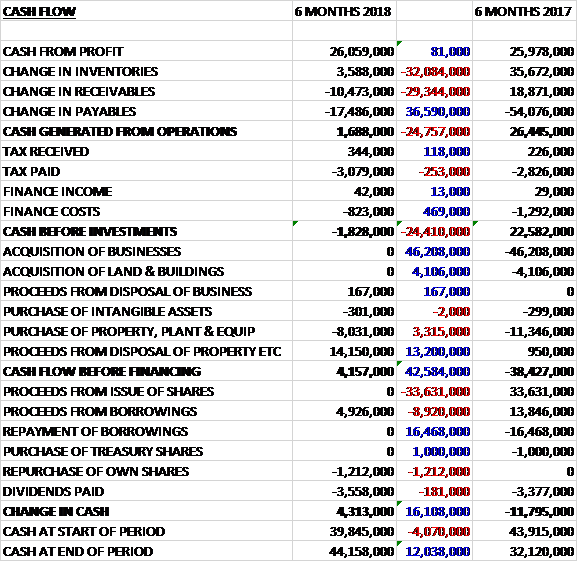

Before movements in working capital, cash profits were broadly flat. There was a large cash outflow from working capital, however, due to a reduction in payables and a growth in receivables. After tax payments increased by £135K and finance costs fell by £469K, there was a cash outflow from operations of £1.8M, a detrimental movement of £24.4M year on year. There were no acquisitions and a net £6.1M was received from the sale of property so there was a free cash flow of £4.2M. Of this, £3.6M was spent on dividends and £1.2M on share repurchases but the group also took out £4.9M of new loans to give a cash flow of £4.3M in the period and a cash level of £44.2M at the period-end.

As can be seen there was a significant cash outflow from working capital in the period. As the pipeline of manufacturer new vehicle consignment inventory expands, the group benefits from the cashflow relating to the VAT reclaimed on this inventory which has yet to be paid for in cash. Equally when the pipeline of new vehicle consignment inventory contracts, the group repays the VAT on the amount of the reduction. During the period the group repaid £16.8M of VAT as pipeline new vehicle consignment inventories fell. This sounds a little dubious to me actually! No mention of this when the group was benefiting from the cash flow!

Current year estimated capex is expected to reduce from £37.5M indicated at the time of the May results to £29.7M currently.

The gross profit in the Aftersales division was £64.2M, a growth of £1.3M year on year. The main driver was the servicing and repair of vehicles, where like for like revenues grew by 4.4%. A key tool to drive customer retention is the sale of service plans, and the group now has 104,142 (97,427) customers who are paying monthly for their service and MOT on the group’s own plans. In addition, a significant number of manufacturer service plans are in place with the group’s customers which further aids retention.

Like for like service margins fell slightly due to the shift in mix towards lower margin warranty work and increasing technician pay levels. Initiatives are being introduced across the group to increase capacity through shift patterns, longer opening hours, mobile van servicing and utilising two technicians per ramp for routine service work to enhance productivity.

The gross profit in the Used Vehicles division was £49.8M, a decline of £2.5M when compared to the first half of last year. Used vehicle sales from internet derived enquiries rose 22% reflecting the importance of the internet. The group is now embarking on an aggressive marketing strategy of its all-encompassing online retailing platform for used cars which is a unique proposition in the UK.

Like for like used vehicle volumes grew by 1.1% in the period while like for like gross profit per unit fell from £1,266 to £1,205. Like for like margins fell from 10.2% to 9.5%, in part due to continued higher average selling prices. The decline in margin was most acute in the premium franchises where weakness was particularly evident around the General Election. Used car margins stabilised later in the period with reduced supply into the market following the reductions in new car volumes.

In March the market was strong, mirroring the new car environment and continued high levels of consumer confidence. Between April and June consumer confidence weakened. High supply levels of part-exchange used cars from the March plate change month coincided with a more challenging consumer environment which resulted in drops in residual values in the wholesale market. This impact was more evident in premium marques and nearly new vehicle segments where margins saw considerable pressure. July and August saw improving wholesale market stability driven by a shortage of supply as new vehicle sales volumes declined, which has created a more robust environment for residual values.

The gross profit in the New car retail and Motability division was £34.3M, a decrease of £700K when compared to the first half of 2017 due to the enhanced performance from the dealerships acquired in the prior financial year (core gross profit declined by £1.3M due to the lower volume of vehicles sold). Like for like car retail volumes in the group fell by nearly 15% with pricing pressures due to currency evident as selling prices rose 5%. The Motability new car market has been under pressure due to the impact of Government welfare reforms, coupled with the pressure on manufacturers in this low margin channel due to currency fluctuations. Motability registrations in the UK fell 4.8% with the group seeing a 5% like for like fall in sales. The gross margin strengthened from 7.2% to 7.6%, however, despite the impact of rising sales prices.

The gross profit in the New fleet and Commercial division was £10.8M, a growth of £200K year on year. The group has increased its market share of the higher margin premium fleet market and engaged less in low margin supply in the volume sector which is reflected in the 6.8% reduction in like for like volumes.

During the period, Sterling traded at lower levels against other major currencies and this currency depreciation has impacted the supply side of the UK new vehicle market as it is less profitable for most manufacturers to import vehicles into the UK. As a consequence, many manufacturers have increased selling prices, reassessed their UK marketing budgets and sought alternative and more profitable markets to which to divert production. These trends have been most acute in volume franchises and have reduced the supply of new vehicles into the UK market.

On the demand side, the uncertainty around the General Election and Brexit vote created a very volatile consumer environment, although confidence has appeared to recover from July onwards. During the period there was considerable media focus on the impact of diesel vehicles on emissions and urban air quality. Consumer demand across vehicle markets reacted to this with a moderate shift of demand into petrol and alternative fuel vehicles. Over the period consumers increasingly realised that diesel vehicles under current production and produces in recent years have a lower environmental impact than older vehicles and demand levels for diesels remained resilient.

Against this background, the March plate change months, which was helped by the pull-forward of registrations due to increase in excise duty in April was a very strong month for UK new vehicle registrations with growth of 4.4% but since March, the remaining five months of the period recorded declines with UK retail registrations for the period down 6.4%.

In August the group completed the sale and lease back of a property operated by a JLR dealership in Leeds. This transaction realised £14.2M in cash and a profit of £4.1M. Further realisations of surplus property is expected over the next year.

During the period the group started a programme of share buy backs under which 3.8m shares have been purchased, deploying £1.6M of cash. A further programme of up to £3M of share buy-backs has just been announced.

Going forward, overall the full year pre-tax profit is expected to be in line with market expectations. The aftersales outlook looks strong with 104,142 active service plans compared to 97,427 last year, used car residual values are strengthening due to reduced supply into the market and the board expect there to be opportunities for acquisitions at more attractive valuations over the next year and a half.

The market conditions described above have not changed significantly during September with weak Sterling causing supply constraints on new vehicles along with pricing pressures. During September, several manufacturers announced scrappage, swappage and switch schemes in an attempt to stimulate the new vehicle market but UK new vehicle private registrations in September were down 8.8%.

The group’s September like for like new vehicle retail volumes fell by 14.8% and this reduced overall profitability from new vehicles year on year. New vehicle margins remained robust as the group achieved manufacturer targets for the quarter at high levels. The group’s used vehicle volumes in September were flat. In recent months, used car residual values have hardened which continued into September and manufacturer scrappage schemes may further tighten supply and underpin used car residual values going forward.

The market for aftersales remains strong as the vehicle parc has continued to grow following several years of strong new vehicle markets. In conjunction with the group’s customer retention strategies, this provides the board with confidence regarding the sustained and growing profit generation from this channel. Aftersales revenues and profits in September were strong.

At the period-end the group had a net cash position of £20.8M compared to £21M at the end of last year. At the current share price the shares are trading on a PE ratio of 8.1 which falls to 7.6 on the full year consensus forecast. After a 10% increase in the dividend the shares are yielding 3% which increases to 3.1% on the full year forecast.

Overall then this has been a robust performance in a difficult market. Profits were up, net assets increased but despite cash profits being flat, there was a big fall in the operating cash flow as the group repaid VAT – it is unclear whether this has unwound or will continue. The new car performance is clearly struggling and volumes were down nearly 15% in September. This weakness has also indirectly affected used cars but margins seem to be firming there. Aftersales continue to be strong and really are the main driver if profitability.

I still don’t get the strategy of selling and leasing back property, only to spend the cash on share buy-backs – this seems very short sighted to me, particularly as the group only recently hit up the market for more cash. Despite this, with a forward PE of 7.6 and yield of 3.1% this is starting to look decent value. The new vehicle market will remain tough but I suspect the other areas will keep the group going so I am tempted to make a purchase here but I note that the consensus forecast is for EPS to fall in 2019 so I might hold fire.

On the 25th January the group released a trading update covering the four months to December. The board expects trading performance for the year as a whole to be moderately below current market expectations, following further declines in the new car market resulting from the depreciation of sterling and a softer general consumer environment.

In the Aftersales market, the group reported continued like for like revenue growth of 3.7%. Whilst service margins declined slightly due to increased labour costs, overall like for like aftersales gross profit grew by 2.2% as parts margins strengthened. There was a 3.2% reduction in like for like used vehicle volumes and a slight reduction in gross margin in the period due to a softening consumer environment and lower levels of pre-registration undertaken as new cash supply into the UK declined.

The group’s like for like new retail vehicle volumes declined by 13.2%, reflecting the franchise mix, and was below the SMMT data of 9.5%. They achieved their manufacturer volume targets, however, and like for like margins were stable with gross profit per unit increasing by 3% to £1,450. The group’s fleet car and light commercial van business has continued to gain market share during the period with new like for like fleet cars growing by 12.4% against an SMMT decline of 11.8%; and new light commercial vans up 0.4% compared to a decline of 4.9% in the market as a whole. This is a very strong performance but the changing mix between car and van sales resulted in a reduction in fleet and commercial margins from 3.7% to 3.3%.

The group has now completed its exit from the Fiat Group business with the closure of Worcester Fiat and Alfa Romeo. In addition, in January the group disposed of a dealership in Boston which was loss making, realising an estimated £1.7M in cash including a freehold property.

Going forward the market for aftersales remains strong as the UK vehicle parc has continued to grow and the board are confident regarding the continuation of a strong performance. The board believes that the used car market will be more buoyant than the new car market in the months ahead and they remain cautious in the new car arena ahead of further forecast updates from the SMMT.

UK new car volumes in the current quarter are likely to reflect the wider trading environment and are likely to be significantly lower than the comparative period, which will include the strong pull-forward impact in the month of March of the changes to Vehicle Excise Duty which took effect in April 2017. While positive on the performance of aftersales and used car channels, the board is cautious on the outlook for the next financial year as new car profitability remains under pressure and cost increases continue. I’m steering clear of this for now.