Victoria Oil and Gas has now released its interim results for the year ending 2016.

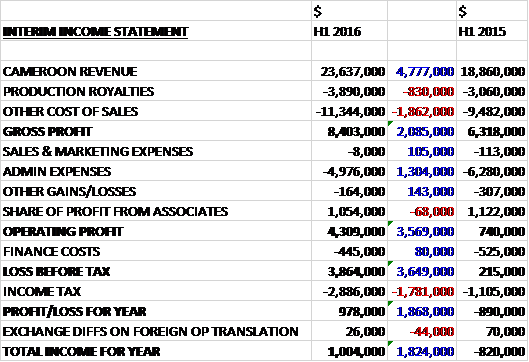

Revenues increased by $4.8M during the period and after royalties were up $830K and other cost of sales increased by $1.9M the gross profit was $2.1M ahead. Admin expenses fell by $1.3M, mainly as a result in a fall in share based payments, and other losses reduced by $143K to give an operating profit $3.6M above that of last time. Finance costs fell by $80K (although finance costs of the facility taken out for the drilling campaign have been capitalised which seems a bit dubious to me) but tax charges grew by $1.8M as the group fully utilised the deferred tax losses previously recognised over unused tax losses in Cameroon, to give a profit for the period of $978K, a positive movement of $1.9M year on year.

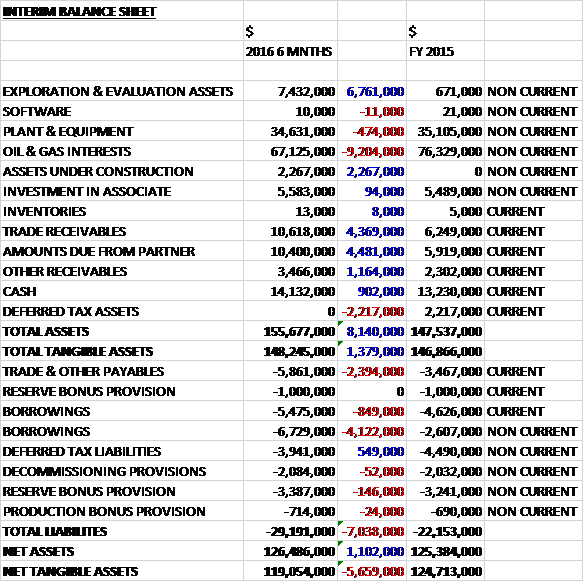

When compared to the end point of last year, total assets increased by $8.1M driven by a $6.8M growth in exploration assets, a $4.5M increase in amounts due from a partner (RSM, received post-period-end), a $4.4M growth in trade receivables (ENEO, also mostly received post period-end), a $2.3M increase in assets under construction and a $1.2M growth in other receivables, partially offset by a $9.2M reduction in the value of oil and gas interests and a $2.2M fall in deferred tax assets. Total liabilities also increased in the period due to a $5M growth in borrowings and a $2.4M increase in payables. The end result was a net tangible asset level of $119.1M, a decline of $5.7M over the past six months.

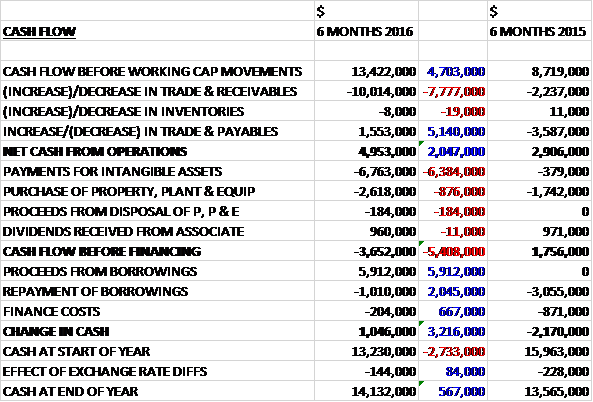

Before movements in working capital, cash profits increased by $4.7M to $13.4M. There was a big cash outflow from working capital due to a growth in receivables reflecting delays in payment from ENEO which has largely been rectified after the period-end, and the net cash from operations came in at $5M, a growth of $2M year on year. The group then spent $6.8M on intangible assets along with $2.6M on property, plant and equipment although they did receive $960K from an associate to give a cash outflow of $3.7M before financing. They took out a net $4.9M of new borrowings to give a cash flow for the period of $1M and a cash level at the period-end of $14.1M.

The Cameroon operation made a profit of $1.9M during the period. There was a 93% increase in the average daily production rate to 13.1mmscf per day with a total of 2,282mmscf of gas sold. Depressed heavy fuel oil prices creates substitution risk and pricing pressure, particularly to the thermal gas sales but this is largely mitigated by the long term gas sales agreement that the group enters into with their customers together with security of supply and environmental benefits. Of the total sales, thermal and retail power sales declined by 114mmscf to 529mmscf but grid power sales grew by 873mmscf to 1,753mmscf. In addition, the group sold 26,047bbls of condensate, a growth of 3,229bbls.

The increase in gas and condensate sales volumes is due to the fact that the group signed a two year take or pay agreement with ENEO and started with the supply of gas to generate electricity in March 2015. The current and prior periods both benefited from the gas consumed by ENEO but the take or pay consumption during the dry season, from January to June, is significantly higher than in the rainy season (which is included in last year’s figures as they cover a different time period.

Despite the fixed gas contracts they have in place with their customers, gas prices came under pressure during the period. The global downturn in oil prices impacts the price of competitive products which can affect the way their customers consume energy. They continue to monitor the impact of the price of HFO and engage with customers to maximise profitability.

The group will be drilling two wells intended to move some of their 2P reserves in the proven reserve category. One of the wells drilled will be a twin of the La-104 well drilled in 1957. The other well will be a step out well that will be drilled into a target that is intended to prove up more of their probable reserves. Both wells are intended to be production wells.

Significant preparation work for the drilling campaign has been completed during the period. The rail mounted rig was delivered to site during July and is currently being commissioned. Weather disruptions, including significant rains and a lightning strike have delayed commissioning but they are now in the testing and certification process and expect spudding to occur shortly.

The Phase II Bonaberi pipeline expansion is well underway and the group expect new customers will be receiving gas before the end of 2016. By the end of the period, 7km of pipeline had been laid and a further 3km was laid up to the end of August, The phased expansion will be completed and commissioned before the end of the year. Expansion of the process plant is scheduled to be performed in three phases. The first phase is to increase the plant capacity by 5mmscf per day to 25mmscf/d. The later phases will increase capacity to 40mmscf per day but are dependent on successful completion of the drilling programme.

The Russia and Kazakhstan operations made a loss of $464K during the period.

As of the end of September the group had $17.6M of commitments pertaining to the drilling programme, the majority of which is expected to be incurred during 2016. In addition to this, they are committed to performing seismic activities on the Matanda concession. The majority of the estimated costs of between $8M and $10M will be incurred during 2017 and 2018.

In April the group reached an agreement with Glencore to acquire a 75% interest in the Matanda block. It neighbours the Logbaba block and provides them with access to additional gas reserves in the area. They will be the operator of this block. The consideration for the transaction was nil but they have assumed the work programme obligations which include seismic work to be performed in the near term and further exploration costs. Included in the acquisition was drilling equipment with a market value of $3.8M but this equipment is included in the accounting records for $0.

Matanda covers an area over 60 times the size of Logbaba and is highly prospective for significant natural gas and condensate resources. The block, with four drilled wells and three discoveries, is estimated to hold P50 gas in volume of 1.8tcf and condensate in place of 136mmbbl.

In August 2016, after the period-end the group entered into formal mediation proceedings with a counterparty regarding the reserve bonus payments. A settlement was reached which resolves all of the outstanding issues and terminates the 1.2% royalty payable to the counterparty. The terms are confidential but the payment is about $10M, only half of which has been provided for.

After invoking a contractual default provision for their Logbaba partner, after the balance sheet RSM has settled all amounts due. RSM have filed an application for arbitration concerning the selection of the drilling rig and contractor for the current drilling programme but the group are confident of their position and will continue to work towards resolving this dispute.

In accordance with the Logbaba farm in agreement, the group is entitled to 100% of the revenues generated by the project until the initial exploration costs, which they incurred, are recovered. Thereafter revenues will be shared 60/40 with VOG receiving 60% which is the same manner that operating costs and post-exploration capital costs are shared. As of the end of May, the initial exploration costs were finally recovered and from June 2016 onwards, revenues are shared in accordance with participating interests of the parties. Therefore, in addition to the seasonal impact of the grid power customer, revenues and operating profits in the second half of 2016 will be impacted by this change.

During the period the group secured a debt facility of up to $26M. With this facility, operating cash flows and partner funding they intend to complete the planned gas expansion programme without recourse equity markets.

Ther have been a number of board changes during the period. Deputy Chairman Grant Manheim retired at the end of May; Ahmet Dik was appointed CEO in June; Finance Director Robert Palmer retired in June; Andrew Diamond joined as Finance director at the end of June and Roger Kennedy joined as a non-executive director in July.

The only forecast I can find seems to suggest the group will make a loss this year so using PE ratios is not going to be very useful. At the period-end the group had a net cash position of $1.9M compared to $6M at the end of last year. By the end of September 2016, however, there was a net cash position of $9M.

On the 27th October the group released an update covering Q3 2016. The average gas production was 7.14mmscf per day, a reduction of 1.05mmscf/d and there was a 12% decrease in gas sales to 630mmscf. Thermal gas sales increased by 76mmscf to 290mmscf representing good growth from the existing customer base, retail power was up 4mmscf to 31mmscf but grid power reduced by 601mmscf to 630mmscf due to the onset of the wet season (they were in line with expectations). The condensate sold fell by 5,768bbl to 6689bbl.

Revenue decreased by $6.1M to $4.7M with the collapse attributable to the reduction in gas sales due to the wet season and the fact that the group are now earning just 60% of revenues.

The Savannah drilling rig was delivered in July and rig up started in August. Two lightning strikes in August caused significant damage to electrical circuits and instrumentation, however. Some of this damage was not apparent until various components were tested individually during commissioning.

Almost all of the lightning related damage has now been repaired. The contractual arrangements on the drilling programme are such that the group only incurs major financial commitments once drilling starts so whilst the delays have been frustrating, they are not expected to suffer any significant cost increases.

The 3.17km of pipeline laid during the quarter, part of the Bonaberi expansion, brings the total pipe laid to 12.25km this year. Of this, 7.13km was commissioned be the period-end, bringing the group’s total commissioned pipeline network to 40.05km. The remaining 5.12km was commissioned shortly after the period-end. In Q4 they will focus on the branch lines to customers and the installation of the PRMS units at customer sites with the aim of bringing new customers online with gas before the end of the year.

Phase one of the gas plant expansion is progressing with the preliminary engineering phase. Further phases of the gas plant expansion will depend on the drilling programme results. At the period-end the group had a net cash position of $2.3M compared to $1.9M at the same point of last year and they had $14.1M of cash on hand.

On the 2nd November the group announced the spudding of the development wells La-107 and La-108. The budget total for the two well programme is about $40M which is expected to be funded by revenue and partner contributions. Drilling is expected to be completed in Q2 2017.

On the 28th November the group announced that it has drilled, cased and cemented the uppermost section of the well La-107 to a depth of 400m. Operations were then suspended as planned and the rig was skidded at a distance of 10m along the rail system to the La-108 well location. Well La-108 was spudded in November and has been drilled and cased to a depth of 400m.

On the 23rd December the group announced that it had completed both the phase II and III of the Bonaberi pipeline extension programme. Three of the new customers are now consuming gas for thermal applications and the remaining four thermal customers are scheduled to commission their burners during Q1 2017. The estimated consumption from the seven new customers will be 600,000scf per day.

Customers currently online or scheduled to be online in January are Maya & c, a palm oil refinery; OK Foods, a biscuit and sweet manufacturer; Agrocam, a packaging company; NAYA, a food processing company; Batoula, a plastic processing company; Bocom, a car battery recycling business; and Camaco, a cocoa processing group.

Drilling of wells La-107 and La-108 is continuing and the group is working with the contractors to make up for the delayed start to drilling. They have drilled and cased the 17.5” section of La-107 to 1,004m and are preparing to drill the 12.25” section to 1,600m where they will set the production casing prior to drilling the reservoir section. The 17.5” section of La-108 has also been drilled and cased to 1,173m and its 12.25” section will be drilled after the current section of La-107 is completed.

On the 3rd February the group released a Q4 operations update. The average gas production increased by 0.5mmscf per day to 7.64mmscf/d and there was a 4.5% increase in the gross gas sales to 654mmscf. This resulted in revenue of $4.6M, a $100K reduction when compared to Q3. So far this year, January has seen a monthly production record, however.

Thermal gas sales were in line with Q3 and were 24% above that of Q4 2015 as three new gas customers started consuming in December following the pipeline expansion. The impact of the new gas supply and the increased ENEO consumption as the dry season starts has already been seen during January with a record monthly supply figure of 14.5mmscf/d.

Grid power sales for the quarter were 12% up on Q4 2015 following increased usage by ENEO. The contract is a two year gas supply agreement which will expire in Q2 2017. Negotiations are underway with ENEO and Altaaqa to renew the contracts for the supply of gas and generation sets, installed at the Logbaba and Bassa power stations in Douala.

Retail power gas sales fell by 63mmscf to just 16mmscf. This reduced consumption is a result of the termination of the lease period of the generators used by these customers to generate electrical power for their operations. They were originally brought into the country to prove the concept of gas to power which resulted in the group being awarded the initial ENEO contract. The customers are individually in the process of purchasing their own generators which are sized appropriately and significantly more energy efficient and the board expect to have them consuming gas again in the future.

At the end of the quarter, well La-108 had been drilled and cased to 1,173m and the 12.25” hole section on well La-107 has been drilled to its target depth of 1,618m. Since the start of January, the La-108 well has been drilled to its 12.25” target depth of 1,953m. MPD technology will be employed during the drilling of the over-pressured Logbaba formation and DDV was set into the casing to assist with this. The addition of this technology to produce higher quality wells and reduce failure risk in the high pressure environment under which they are being drilled has added to the initial estimated budget. In addition, higher than expected non-productive time related to various operational uses has increased the schedule. The revised budget range for the two well programme has now been increased by about 15% to $40M-$48M.

About $23M has been spent to date on the project so the balance of the group’s $13-15M share of the programme will be funded by cash generated from operations and existing debt facilities. The gas processing plant expansion is progressing with the preliminary engineering phase being worked into the pending new flow line works to tie in the new wells.

At the year-end they had a net cash position of $1.3M compared to $2.3M at the end of last quarter and had a cash balance of $15.8M with undrawn lines of credit of $16M.

Overall then this has certainly been a period of progress for the group. In the first half, profits were up as was the operating cash flow but no free cash was generated and net assets declined. This was a long time ago, however, and since then grid power sales seem to have been decent but retail power has been hit by the end of the generator lease period – I must have missed the fact this was happening as it was a surprise to me. The group managed to sort out the royalty issue but this seems to have come at quite a substantial cost. Still, this is a positive development in my view. Also the Matanda acquisition seems a very shrewd bit of business – that looks a great purchase.

The Bonaberi pipeline expansion seems to be progressing well and should bring in more gas sales going forward and January which coincides with the start of the dry season has been very strong. It is important to remember though that the group is only earning 60% of the revenues from this compared to 100% in the last financial statements we have seen so revenues and profits are unlikely to be as strong. The delays and cost-overruns to the drilling in the drilling campaign are a pain too. In conclusion, things seem to be progressing OK here but I would like to see some financial statements where the group is earning its 60% share of revenues before jumping in I think.

On the 6th March the group announced that they had signed a farm-out agreement with Bowleven relating to the Bomono production sharing contract. Gas produced from the contract will be fed into the customer distribution network owned by VOG and first gas supply is expected to start following the granting of a provisional exploitation authorisation.

On completion, a Bowleven will have a 20% working interest in the Bomono PSC with VOG have an 80% working interest. Bowleven will remain as operator of the product despite owning just 20%. Gas from Bomono PSC will be sold to GDC less a tolling fee. The gas price paid will be a weighted average received by GDC(VOG) for its total domestic sales less a tolling fee for the use of the pipeline network.

The pipeline connection from the Bomono POSC to the main network will be managed and funded by VOG and they will complete the civil engineering works necessary for the gas processing plant installation at the Bomono site, the estimate cost of which will be $6M. Bowleven have agreed to pay VOG 50% of any deficit if the first three years of net income is less than the development expenditure incurred, up to a maximum of $2M.

Bowleven will receive a 3.5% royalty from VOG’s production share of hydrocarbons with an aggregate cap limiting the total royalty payments of $20M and Bowleven will also receive £100K of new shares in VOG.

As previously announced the detailed prospect inventory prepared indicates there is 146bcf and 263bcf of mean un-risked GIIP in the Tertiary and deeper Cretaceous reservoir intervals respectively. Overall this seems like a pretty good deal to me, although the royalty payments are a bit of a shame. The company is looking more and more investable.

On the 13th April the group released a Q1 operations update. There was a 10.7% increase in gas production from Logbaba to 14.57mmscf per day and the gross Logbaba gas sales increased by 22mmdcf to 1,152mmscf as a reduction in sales for grid power was more than offset by a growth in thermal power sales. Due to the fact that the group is now only earning 60% of revenues, however, the total net sales was 692mmscf compared to 1,131mmscf in Q1 2016. The gross amount of condensate sold declined by 4,775bbl with the net amount even lower. Phases 2 and 3 of the Bonaberi pipeline extension programme were completed by the end of 2016 and six new customers are now online and consuming gas.

Grid power sales were higher than Q4 but lower than Q1 last year. The ENEO contract expires in April 2017. Negotiations are well advanced and the board expects a renewal for the supply of gas to the Logbaba and Bassa power stations.

The group made $8.1M of net revenue, up from $4.6M in Q4 last year and had a net debt position of $10.7M compared to a net cash position of $1.3M at the end of December. The current cash position is $14.1M.

In the Logbaba drilling programme, significant gas-bearing sands have been identified in the La-108 well and once completed it is expected to contribute to an increase in proven reserves. At the end of Q4, La-108 had been drilled and cased to 1,173m. In this quarter the casing has been run and cemented in La-107 in preparation to drill the 8 ½ hole sections through the Logbaba gas-bearing reservoir sections.

As the La-108 8 ½ hole section was drilled through the Logbaba formation to a depth of 3,076m a mechanical problem with the drill string led to a gas kick and the well control incident. While the well was brought under control, the drill pipe became stuck in the well and the team was unable to retrieve it. In late March, a cement plug was placed in the 8 ½ hole and preparations were made to sidetrack the well to re-drill the Logbaba formation and complete the well which is ongoing.

The well control and pipe issues, coupled with the side track have resulted in a scheduled slippage of some five weeks and an estimated budget increase of about $8M, taking the expected cost to complete both wells to $56M. Planned completion of the wells is now mid Q3 but it is expected that the wells will be under test before this. The group’s share of well costs will be covered by cash generation and existing facilities.

The gas processing plant expansion is progressing the preliminary engineering phase underway. A 300m long, high pressure gas flowline is being installed from the new wells to the gas processing plant to utilise gas produced during flow tests and enable early production from wells La-107 and La-108. In addition, gas plant improvements such as installation of a heat exchanger and high and low pressure liquid separators are also being installed in anticipation of new production from the wells.

At Matanda, while the analysis is at an early stage, the board are encouraged by the indications of onshore prospects in the Northern area of the license. The evaluation is expected to yield an updated prospect inventory by Q3, from which drilling plans can be made. This will provide the opportunity to target the most attractive and lowest cost opportunities for early drilling with the aim of bringing further wells on production in 2018-2019.

Following the execution of the agreement with Bowleven, they announced significant board changes. The group is apparently continuing their good relationship with the board of Bowleven and progressing the project as intended.