From July, trading undertaken by the Environment business unit has been consolidated with the Civil and Transportation consulting business to form an infrastructure and environment consulting business. Also, the results of the other international business unit has been included in the European business. I suppose if you can’t get a business to break-even point, just merge it with one that is profitable and job done!

Waterman has now released its interim results for the year ending 2016.

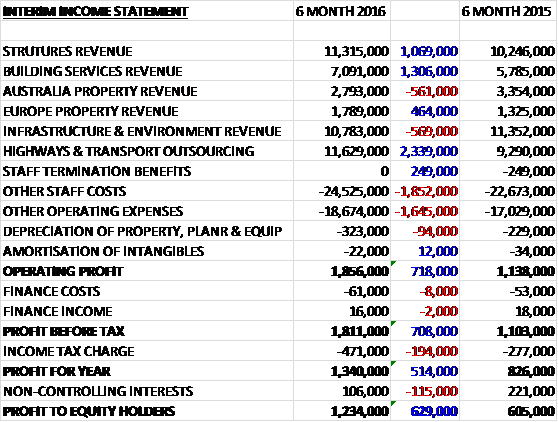

Revenues increased when compared to the first half of last year as a £2.3M growth in highways and transport outsourcing revenue, a £1.1M in structures revenue, a £1.3M growth in building services revenue and a £464K increase in European property revenue was partially offset by a £569K fall in infrastructure and environment revenue and a £561K decline in Australia property revenue due to the weaker Aussie dollar. Staff costs increased by £1.6M and other operating expenses were up £1.6M so that the operating profit increased by £718K. Income tax expenses were up £194K which meant that the profit for the period was £1.2M, a growth of £629K year on year.

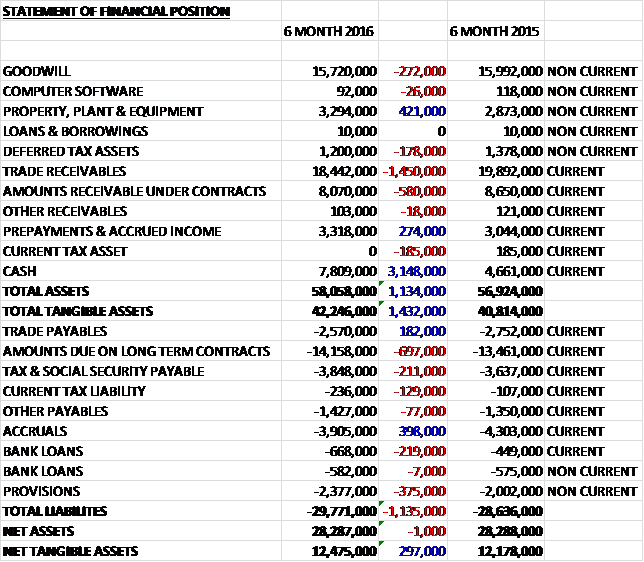

When compared to the end point of last year, total assets increased by £1.1M driven by a £3.1M growth in cash and a £421K increase in property, plant and equipment, partially offset by a £1.5M decline in trade receivables and a £580K fall in amounts receivable under contracts. Total liabilities also increased as a £697K increase in amounts due on long term contracts and a £375K growth in provisions was partially offset by a £398K fall in accruals. The end result is a net tangible asset level of £12.5M, a growth of £297K over the past six months.

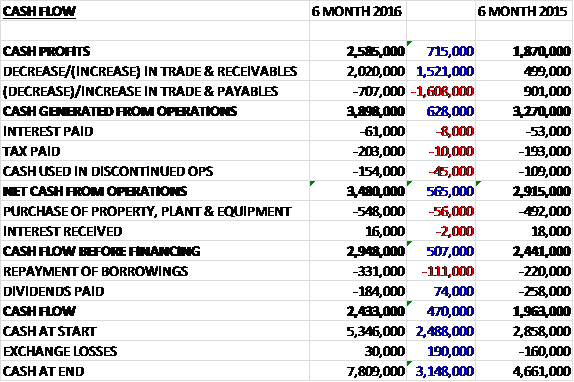

Before movements in working capital, cash profits increased by £715K to £2.6M. There was a cash inflow from working capital with a fall in receivables, benefiting from early customer receipts ahead of the calendar year end, and after modest increases in taxes paid and cash used in discontinued operations, the net cash from operations came in at £3.5M, a growth of £565K year on year. The group spent just £548K on property, plant and equipment so that there was a free cash flow of £2.9M. They then spent £331K on repaying loans and £184K on dividends to give a cash flow for the period of £2.4M and a cash level of £7.8M at the period-end.

The operating profit at the Structures business was £650K, a growth of £93K year on year and the operating profit at the Building Services business was £150K, a decline of £104K when compared to the first half of last year with investment continuing in the recruitment of additional staff and design software A number of new commissions within the property team are yet to release profits as they are still at the early stages of design.

The group continues to win and deliver new projects. Friars Walk, a 38,000m2 retail development in Newport opened in November and construction has started on the 80,000m2 retail development at Westgate Oxford by Land Securities and the Crown Estate, both projects where the group designed the structures. The 42,000m2 Victoria Gate retail development in Leeds, on which the group are the structures and building services designers, reached a significant milestone with the completion of the highest structural point of the development.

The group is the designer for Capital & Countries Properties on three of their developments which have started on sites around Covent Garden. They are all mixed use retail and residential developments with a combined area of over 11,000m2. In addition to these projects, they are also assisting them on their masterplan for the 77 acre Earls Court Development. Several commercial projects in the City of London have made significant progress on site over the past six months. In particular, Angel Court by Mitsui Fudosan and Stanhope and New Street Square by Land Securities, which is pre-let to Deliotte, are nearing the completion of the construction of the structure.

The operating profit at the Australia business was £336K, a fall of £120K when compared to the first half of 2015 with part of that decline due to the weakening of the Australian dollar. Revenues were also lower but Q2 improved after a poor Q1. The business has continued to win new commissions, particularly in the healthcare market. They have been appointed to design the building services on the A$200M Joan Kirner Women’s and Children’s hospital which will be the third largest maternity hospital in the state of Victoria.

The operating profit in the European business was £118K, an increase of £46K year on year. In Ireland the group have been appointed for the redevelopment of the Clerys Building in Dublin which is a £50M mixed use scheme for D2Private. They also advised Hammerson and Allianz Real Estate on their £1.34BN acquisition of a portfolio of retail assets in Dublin from Ireland’s National Asset Management Agency.

The group also provided engineering and environmental due diligence studies for the £335M acquisition by Hammerson of the Grand Central Shopping Centre in Birmingham. The scheme is developed by Network rail and Birmingham City Council as part of the £750M New Street regeneration project.

The operating profit at the Infrastructure and Environment Consulting business was £23K, an improvement of £301K when compared to the first half of last year. The streamlining of the business resulted in more focused units and there were significantly fewer historic commissions passing through the business which had previously adversely affected profitability. The business was very active, advising clients across all markets throughout the UK.

They continue to provide pre-planning support on major urban regeneration projects in London including Battersea Power Station, Brent Cross and Old Oak Park. More recently they have advised on the proposed development of the old Shredded Wheat factory site in Welwyn Garden City for Spen Hill Developments, the redevelopment of Royal Mint Court opposite the Tower of London for Delancey and LRC, and the redevelopment of the Elephant & Castle shopping centre for Delancey and APG. They are also assisting British Land with engineering and environmental advice for the development of a masterplan for the 46 acre mixed use regeneration of Canada Water.

The operating profit at the Highways and Transportation outsourcing business was £579K, a growth of £253K year on year with staff numbers increasing by 22%. The autumn statement by the chancellor confirms the government’s commitment to invest in highway and transport infrastructure which bodes well for the continued flow of new projects and commissions. The board are expecting demand for these services to grow which should increase operating margins in future years. They currently provide highways and transportation engineers to over fifty local authorities and highways departments throughout the UK.

It is worth noting that this company seems to have quite a lot of overdue receivables as over 55% seem to be overdue and over 15% were impaired. This is actually an improvement on the prior year but it still seems high to me. Also, as touched upon before, there is a hefty LTIP award here that has the potential to be quite dilutive. There are 3,000,000 nil-cost options outstanding, all of which will vest of the share price remains above 150p for a short period of time. This is not a very stretching target and seems rather greedy in my view.

Going forward the board expects further progress to be made during the second half of the year and beyond and they expect to continue to generate repeat business year on year whilst the UK economy is strong.

At the period-end the group had a net cash position of £6.6M which was an improvement on the £3.8M net cash position at the year-end. A the current share price the shares trade on a forward PE of just 10.5 and after a 50% increase in the interim dividend the shares are yielding 2.9% which increased to 3.7% on the full year consensus forecast.

Overall then, this has been a strong period for the group. Profits were up, net tangible assets increased and the operating cash flow grew with plenty of free cash being generated. The structures business performed well, as did the Irish business and the Highways and Transportation outsourcing division which looks very strong. The Infrastructure and Environment business hit break-even, although this was mostly because the loss making business has been merged with the profitable environment one. This is perhaps a little unfair, as it has also been streamlined and there were fewer historic commissions affecting profitability.

The Australian business fared less well, in part due to weakness in the Aussie dollar, and the Building Services business also suffered a decline in profitability due to continued higher investment. The shares do look cheap with a forward PE ratio of 10.5 and yield of 3.7% and I am tempted to take a position here but I am held back by Brexit worries and the possible effect it would have on the UK economy. I will have a think about this and may add.

On the 11th May the group released a trading update covering Q3. Their trading performance has remained in line with board expectations with revenue in the first nine months of the year 10% above the prior year period. The board continues to anticipate that results for the current year will show a significant increase in adjusted operating margin and cash collection has been strong with group net cash at the year-end now expected to be above the current market forecast.

This is all reassuring stuff but I feel a bit overexposed to the sector at the moment with the looming Brexit vote so I will probably sit this one out.

On the 16th June the group announced that CEO Nick Taylor purchased 32,756 shares at a value of £28K to give him a total holding of 212,525.

On the 27th June the group announced that it has been commissioned to provide advice on two riverside residential projects in West London. They have been appointed by Pinenorth Properties structural designs for the 4.5 acre Tedding Film Studios riverside site where planning consent has been granted for over 200 apartments. Demolition of the existing buildings is currently ongoing and construction of the new apartments will start this year.

A second commission recently received from Reselton is to provide environmental and structural advice for the planning application for the 22 acre Stag Brewery site adjacent to the River Thames at Mortlake. This site is being developed for residential, retail, hotel and leisure use. This is good stuff, clearly designed to halt the share price collapse after the Brexit vote.

On the 28th July the group announced the start on site of the Capital Dock development by Kennedy Wilson in Dublin where they have been appointed to provide civil and structural engineering services. The project includes 30,000m2 of office space and 190 homes across three buildings, one of which will be the tallest tower in the city.

On the 1st August the group released a trading update covering the year ending June. The board expects to report results which exceed its previously declared objective of tripling annual pre-tax profit to £3.3M over the three year period to June 2016. An emphasis on working capital management has resulted in a significant improvement in the cash position and they expect to report net cash of £5.4M compared to £3.8M at the same point of last year and £6.6M at the half year point.

Whilst the recent EU referendum decision has generated a period of uncertainty for markets, the board feel it is too early to speculate what impact there will be on future prospects. In the five weeks since the referendum they have continued to experience good levels of enquiries and have been appointed for several new commissions.

So, this seems to be a good performance but this was never really in doubt. More important is future prospects but despite holding up OK, as the group say – it is just too early to tell.

On the 22nd September the group announced that it had been appointed by Canary Wharf Group to provide structural engineering for a significant development at Canary Wharf. They are assisting them with their plans for a further phase of the overall development which is likely to involve over 200,000 square metres of mixed use buildings.