Wynnstay has now released its final results for the year ending 2016.

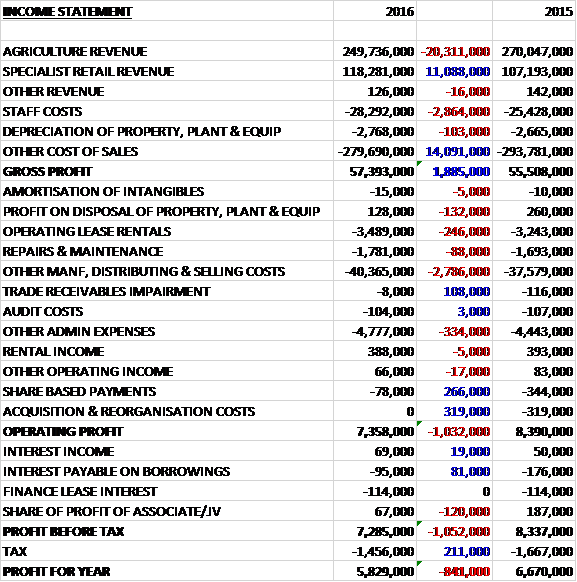

Revenues declined when compared to last year as an £11.1M growth in specialist retail revenue due to the prior year acquisitions was more than offset by a £20.3M decline in agriculture revenue. Staff costs increased by £2.9M, depreciation was up £103K but other cost of sales decreased by £14.1M to give a gross profit £1.9M above that of last year. Operating lease rentals grew by £246K and other manufacturing, distribution and selling costs were up £3M with admin expenses growing by £225K. We also see a £266K reduction in share based payments and no acquisition costs which accounted for £319K last time to give an operating profit £1M higher. Interest payments came down but there was a £120K reduction in the share of profits from associates which meant that after the tax charge declined by £211K the profit for the year was £5.8M, a decline of £841K year on year.

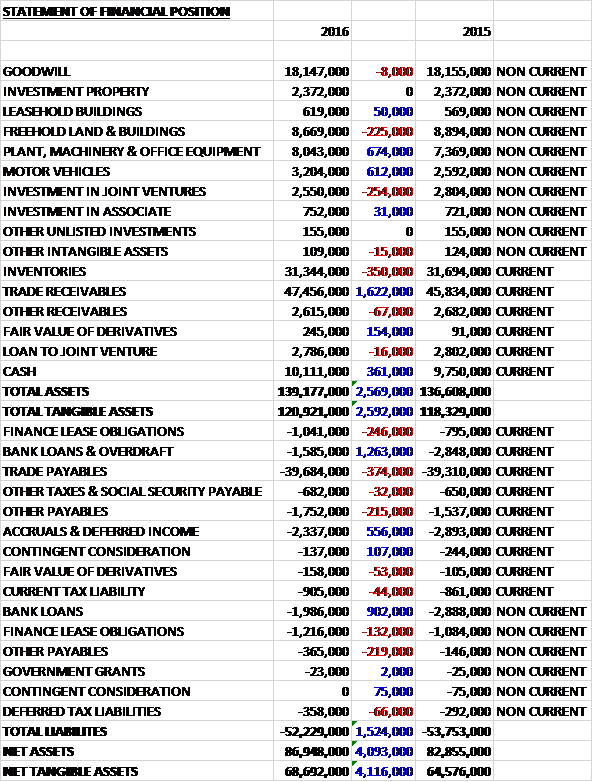

When compared to the end point of last year, total assets increased by £2.6M to £139.2M driven by a £1.6M growth in trade receivables, a £674K increase in property, plant & equipment, a £612K growth in motor vehicles and a £361K increase in cash partially offset by a £350K decline in inventories. Total liabilities declined during the year as a £2.2M fall in bank loans and a £556K decrease in accruals were partially offset by a £374K growth in trade payables. The end result was a net tangible asset level of £68.7M, a growth of £4.1M year on year.

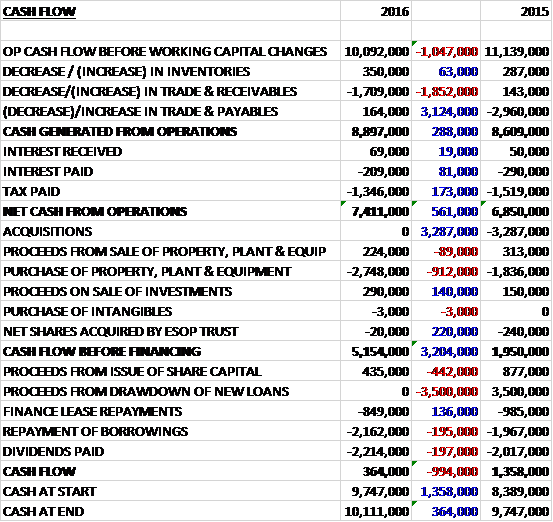

Before movements in working capital, cash profits declined by £1M to £10.1M. There was a cash outflow from working capital but this was less than last year and after tax payments declined by £173K and interest payments declined mostly the net cash from operations was £7.4M, a growth of £561K year on year. The group spent a net £2.5M on property, plant and equipment and had a free cash flow of £5.2M. Of this, £849K was used to repay finance leases, £2.2M went on repaying borrowings and £2.2M went on dividends to give a cash flow for the year of £364K and a cash level of £10.1M at the year-end.

The operating profit for the Agriculture division was £3M, a decline of £1.1M year on year as customers looked to cut costs. The downturn in farm output prices experienced over the last two years has been widely felt across most sectors. The downturn was especially evident in the dairy sector with milk prices falling below the cost of production for most farmers. The resultant fall in demand for feed and associated products has been felt nationally and the group’s feed activities were similarly affected. By contrast, despite low grain prices reducing crop farmers income, their arable activities contributed an improved performance over last year.

Demand for livestock feed was down year on year, mirroring national trends. As mentioned above, the reduced demand was particularly evident in the dairy sector, especially for blended feeds, some of which was replaced by straight feeds. This reduction reflected a decision on the part of the farmers to search for production efficiency and, for some, not to feed for marginal milk volume. The resultant reduction in UK milk yields was the catalyst for an upward movement in milk prices in the late summer, however. Feed demand over the winter period has improved and there are encouraging signs that demand will continue to strengthen.

Glasson’s contribution this year was lower than in the prior year with margin pressure across all products and a reduction in fertilizer volumes which was also evident in the Fert Link joint venture.

The group’s arable activities have continued to perform well despite the subdued market environment. Demand for all products was higher year on year which was reflected in volumes. As they expected, however, there was also some pressure on margins. Sales of cereal and herbage seed have been buoyant and broken previous records. Demand for fertilizer was subdued at the beginning of the year but they are well placed to satisfy the market. An active buying spell in the autumn helped increase volumes for the year as a whole ahead of the previous year.

Grain volumes were strong in the first half but the smaller 2016 harvest resulted in reduced activity in the second half on a like for like basis. During the year they started to combine the management of the Woodheads seed and grain business with the Wynnstay seed and Grain Link operations. They expect to complete this process over the coming months.

The operating profit for the Specialist Retail division was £4.5M, a fall of £538K when compared to last year reflecting margin pressure and opening costs in the new stores. The group have now completed the integration of the Agricentre business acquired in 2015, and all the outlets have been rebranded. The group expect the acquired stores to make a positive contribution to the results during 2017. In August they opened a new store next to the sedgemoor Livestock market near Bridgwater. It is a strategically important trading area and complements the newly acquired Agricentre stores.

Although total sales increased by 12%, like for like sales declined, primarily reflecting lower fertilizer sales and a reduced volume of hardware and ancillary products in the dairy sector.

The group added three Just for Pets stores during the year including one Bessie and Boo boutique store in Evesham. The contribution from the pet business is behind that of last year reflecting the opening costs and maturity curve associated with new outlets as well as a small reduction in like for like sales.

The Youngs Animal Feeds business performed in line with expectations and the group believe that there are further opportunities available to it as they continue to expend the specialist retail division as a whole.

The group have been investing significantly across the group and completed a major investment in new packaging facilities for bagged animal feed. This investment enables then to satisfy the growing requirement for bagged feed as they increase the number of their stores. Further investment is now targeted across their arable and feed operations to support growth and efficiencies within the group.

The Brexit vote brings a degree of uncertainty to the agricultural industry but the macroeconomics of food demand are encouraging. Over recent months there has been a recovery in output prices for farmers, mainly as a result of the devaluation of Sterling, and the new financial year has started in line with management expectations. The board remain optimistic of future improvement.

At the current share price the shares are trading on a PE ratio of 19 which falls to 18.5 on next year’s consensus forecast. After a 5% increase in the final dividend the shares are yielding 2.1% which increases to 2.2% on next year’s forecast. At the year-end the group had a net cash position of £4.3M compared to £2.1M at the end of last year.

Overall this has been a rather difficult year for the group. Profits declined and although the operating cash flow grew, this was due to more favourable working capital movements and cash profits fell. Having said that, the group did produce a very good level of free cash and the net asset level grew.

Both sectors saw declines. The agricultural business was hit by lower output prices for farmers, particularly in the dairy sector which saw demand for livestock feed tank. In the retail sector, the farm business saw margins under pressure due to the lower farm output prices and the pet business also saw a small like for like decline in revenue. The acquired stores should contribute to profits next year, however.

Brexit has been a double edged sword. Clearly it adds uncertainty to the industry with the fate of subsidies etc not yet known. The decline in Sterling has been a positive, however, and recent months have seen farm output prices rise with a recovery in the dairy market. This bodes rather well for this year and I do like this company – it seems very well run. My only issue really is the continuing uncertainty surrounding Brexit and the high valuation for the shares – a forward PE of 18.5 and yield of 2.2% look rather expensive to me.

On the 21st March the group released an AGM statement. The trading environment for farmers has continued to show signs of recovery, with farm output prices higher year on year, although from low comparatives. At this stage the board continue to remain encouraged that they are on track to return to growth this year.

In the Agriculture division, demand for ruminant feed has increased, reflecting national trends. Fertilizer sales have been good as farmers purchased ahead of expected price increase. Demand for spring seed is also encouraging and, as expected, the smaller 2016 harvest has meant that grain trading volumes in the period are behind the previous year.

Within the specialist retail operations, the agricultural retail activities have seen a small increase in like for like sales over recent months, mainly attributable to hardware products. Demand at Just for Pets, the pet products business, remains subdued, reflecting the challenging high street.

Overall then things seem to be improving but this doesn’t seem quite strong enough to encourage me to buy in here.

On the 24th May the group releases a trading update covering the first half of the year. Excluding Just for Pets, the group is expecting to show a better performance year on year. Trading headwinds for farmers have eased somewhat but the agricultural environment remains challenging with margin pressures a feature. Just for Pets has continued to experience subdued demand, reflecting general retail trends in the sector, and certain stores in particular have not delivered the expected performance, resulting in losses in this activity during the first half.

As a consequence the board now expects to book a goodwill impairment for the period which will result in the group’s reported profits being materially lower than in the first half of last year. Excluding this, the adjusted pre-tax profit will be marginally below last year, impacted by the performance of Just for Pets.