Zytronic has now released its interim results for the year ending 2016.

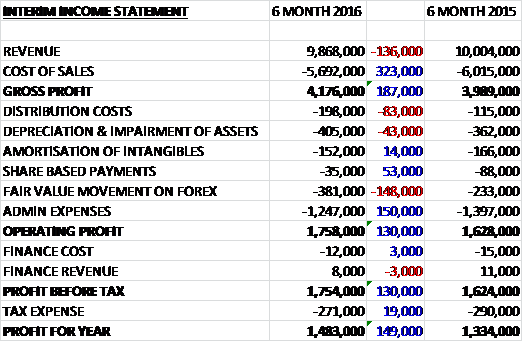

Revenues declined by £136K when compared to the first half of last year but cost of sales also fell and the gross profit was £187K above that of last time. Distribution costs increased by £83K and depreciation was up £43K but these increases were partially offset by a £53K fall in share based payments. We then see a £148K increase in the loss from forex movements offset by a £150K decrease in other admin costs to give an operating profit £130K above that of the first half of 2015. Tax expenses fell slightly and the profit for the six month period came in at £1.5M, a growth of £149K year on year.

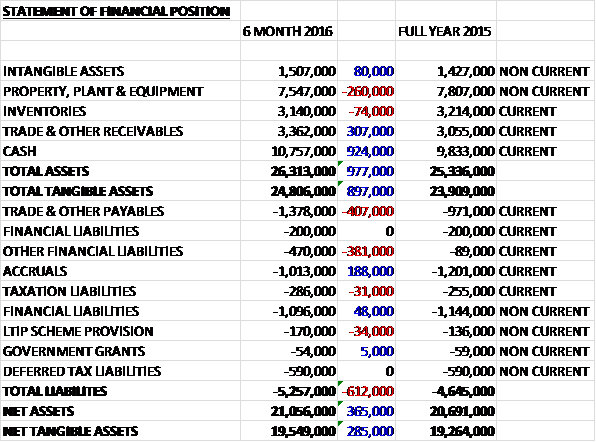

Total assets increased by £977K when compared to the end point of last year, driven by a £924K growth in cash and a £307K increase in receivables, partially offset by a £260K decrease in property, plant and equipment. Total liabilities also increased during the period as a £407K growth in payables and a £381K increase in other financial liabilities were partially offset by a £188K decline in accruals. The end result was a net tangible asset level of £19.5M, a growth of £285K over the half year period.

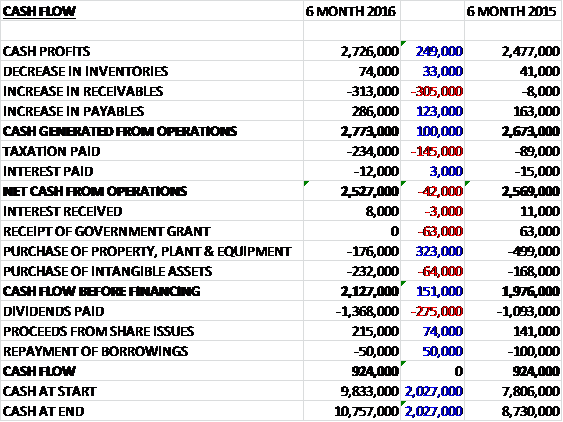

Before movements in working capital, cash profits increased by £249K to £2.7M. There was a broadly neutral working capital position but tax payments increased by £145K to give a net cash from operations of £2.5M, a decline of £42K year on year. The group spent £176K on property, plant and equipment along with £232K on intangible assets so there was a free cash flow of £2.1M. Of this, £1.4M was spent on dividends which meant that there was a cash flow of £924K for the half year and a cash level of £10.8M at the period-end.

Whilst revenues were slightly lower, this was to some extent expected and consistent with the strategy of moving away from the traditional glass displays and growing the touch product business as sales of touch products increased by £400K to £8.3M and sales of glass displays and filter products reduced by £500K to £1.6M with ATM display filters falling by £600K. The group has continued to see growth and opportunities in areas that require larger size touch sensors in particular demand for large format curved products developed for the gaming industry.

By market, there were lower volume requirements from China based OEM sites for financial products. In gaming, there was a continuation of the strong H2 2015 demand which was considerably above that in the first half; in the vending market the forecasted reduced demand from Coca Cola, fuel payment system project end of life in H1 last year and lower fuel vending demand from Korea gave rise lower sales; and in industrial markets sales reduced due to lower oil and gas demand for HM1 panels.

The second half of the year has so far experienced a similar trend with touch product revenues continuing to increase relative to the traditional products, and the consequent improved margins from this change in mix and the move towards the more niche larger touch sensors. The board expect to continue to make progress in the coming year.

After a 10% increase in the interim dividend the shares are yielding 3.2% which increases to 3.4% on the full year forecast. At the current share price the company is trading on a forward PE ratio of 15. At the period-end, the group has a net cash position of £9.5M, an increase of £1M over the past six months.

Overall then, this was a solid if rather uninspiring update from the group. Profit was up but this was due to an improvement in the product mix and revenues declined, net assets increased but the operating cash flow declined due to an increase in tax payments. Cash profits did improve, however, and some decent free cash was generated.

There has been an increase in touch products for the gaming industry at the expense of ATM filters, Korean fuel vending products, an expected reduction in demand for vending products from Coca Cola and a reduction in industrial products due to the collapse in the oil and gas industry. The outlook statement seems a little subdued but there is a decent 3.4% forward yield on offer here and the forward PE ratio of 15 doesn’t seem too bad when the large net cash position is taken into account.

In conclusion, I think the price is about right so I continue to hold but my convictions is not quite as strong as it was.

On the 17th October the group released a trading update for the full year. The second half of the year has shown a continuing trend to that reported in the first half, with touch products increasing relative to both traditional products and year on year. Pre-tax profit for the full year will reflect the impact of a £900K provision arising from the forex policy but the underlying profit is expected to be significantly ahead of last year and at least in line with market expectations.