Zytronic has now released their interim results for the year ending 2017.

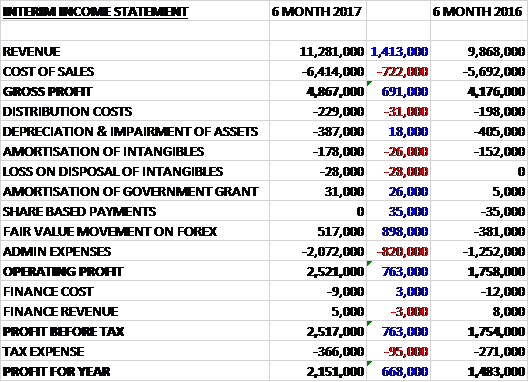

Revenues increased by £1.4M when compared to the first half of last year and with cost of sales only up £722K, the gross profit increased by £691K. Distribution costs were up £31K and there was a loss of £28K from the disposal of intangibles. There was an £898K positive swing in hedging instruments but other admin expenses were p £820K to give an operating profit £763k above that of last time. Finance costs were broadly flat but tax charges grew by £95K which meant that the profit for the half year was £2.2M, a growth of £668K year on year.

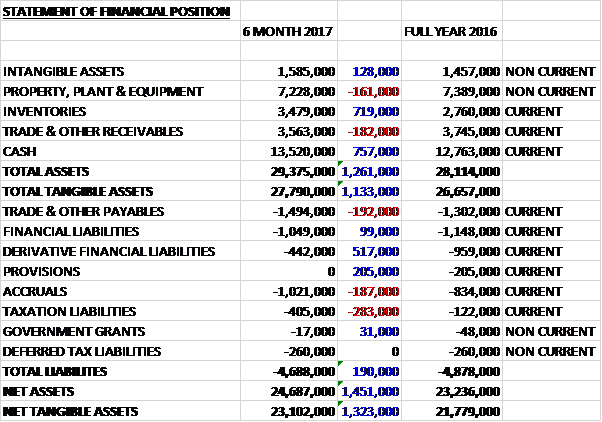

When compared to the end point of last year, total assets increased by £1.3M driven by a £757K growth in cash, a £719K increase in inventories and a £128K growth in intangible assets, partially offset by a £182K decline in receivables and a £161K decrease in property, plant and equipment. Total liabilities reduced modestly as a £283K growth in current tax liabilities, a £192K increase in payables and a £187K growth in accruals were more than offset by a £517K decline in derivative financial liabilities and a £205K decrease in provisions. The end result was a net tangible asset level of £23.1M, a growth of £1.3M over the past six months.

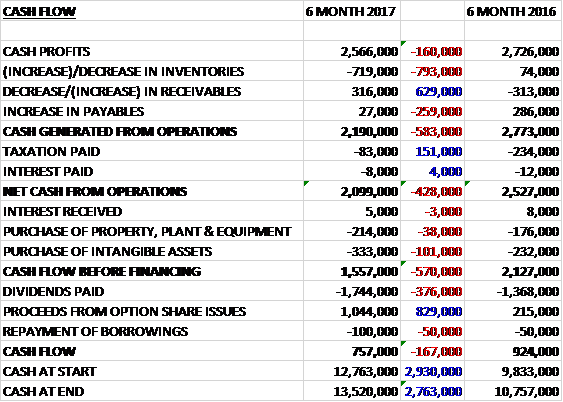

Before movements in working capital, cash profits declined by £160K to £2.6M. There was a cash outflow from working capital but tax payments reduced by £151K to give a net cash from operations of £2.1M, a decline of £428K year on year. The group spent £214K on tangible assets and £333K on intangibles which meant there was a free cash flow of £1.6M. This didn’t quite cover the £1.7M paid out in dividends but the group received £1M in proceeds from share option issues to give a cash flow for the period of £757K and a cash level of £13.5M at the period-end.

During the period there was an increase in demand for the large format proprietary touch products. Touch revenues increased by £1.7M to £10M and together with the focus on proprietary technology for larger format and multi-user sensors, combined to improve gross margin from 42.3% to 43.1%. The principal drivers of growth continues to be the large format sizes in particular in the gaming sector for upright cabinet designs through both Asia Pacific and UK-based customers.

The gaming market has seen the largest increase in revenues with growth of £1M. In gaming, there was increased volumes and mix of MPCT and curved products with new projects started for Japan and Australia. In the financial market growth of £400K in the period was mainly through the EMEA region and some market effects were felt through the merger of Diebold and Wincor Nixdorf. In vending the £300K improvement in revenue has arisen from an increase in period demand from Coca-Cola as well as car parking systems in Germany. In industrial, the £100K revenue growth came from increases of sales to Germany. Signage was the only market to show a decline, down £100K.

In March the group carried out a capital reduction exercise whereby £8.9M of their undistributable profits were capitalised by way of a bonus issue of newly created capital reduction shares. These shares were cancelled and the £8.9M was credited to the retained earnings reserve as distributable profits. I don’t pretend to understand this but I guess it means more can be distributed in dividends? The second half of the year has started well and is in line with expectations.

At the current share price the shares are trading on a PE ratio of 20.1 which falls to 18.3 on the full year consensus forecast. After a 10% increase in the interim dividend the shares are yielding 2.8% which increases to 3.2% on the full year forecast. At the period-end the group had a net cash position of £12.5M compared to £11.6M at the end of the year.

As usual then, this update is rather scant on the details but things seem to be going OK. Profits were up, but this might just have been due to favourable forex movements and the operating cash flow deteriorated year on year. There was still a decent amount of free cash flow generated, however, and the net assets also improved. The main driver of performance seems to be from the gaming industry with revenues up substantially. The second half has started in line with expectations but a forward PE of 18.3 and yield of 3.2% doesn’t suggest amazing value. The group has a strong net cash position, however, which should be taken into account and I continue to hold.

On the 19th October the group released a trading update for the year as a whole. Revenues have continued to show good progress and results are expected to be in line with market expectations.