Shaft Sinkers have now released their interim results for the year ending 2014.

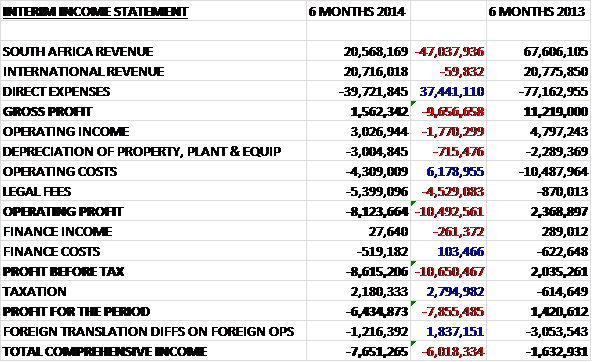

Revenues took a big hit during the first half of the year. Sales from within South Africa collapsed by £47M to just £20.6M whilst International revenues were flat. Direct expenses nearly halved to £39.7M to give a gross profit some £10M lower at £1.6M. Operating income fell by £1.8M and was broadly counteracted by the depreciation of the tangible assets. Operating costs fell by £6.2M but this was counteracted by a £4.5M increase in legal fees. This is certainly taking its toll on profitability and the operating loss increased by over £10M to £8.1M. There was also half a million pounds of operating costs before the group got a tax rebate of £2.2M due to the loss making South African operations which meant that the total loss for the half year was £6.4M, a swing of £7.9M on the small profit made during this period of last year.

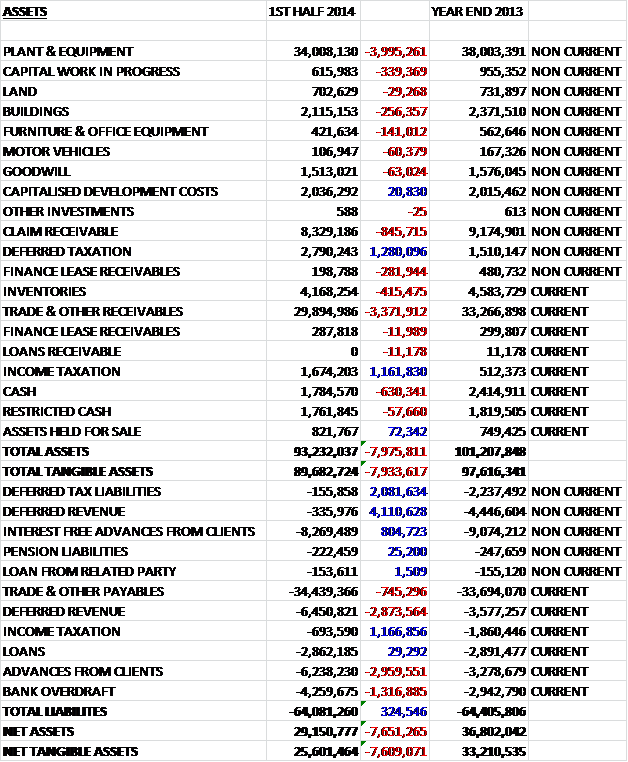

Overall assets fell by just under £8M when compared to the end point of last year. This was driven by a £4M fall in the value of plant & equipment, a £3.4M reduction in trade & receivables, and an £800K fall in the value of claims receivable. These decreases were only partially offset by a £2.4M increase in taxation assets. Liabilities were broadly flat during the same period, down by just £300K as reductions in deferred revenue (£1.2M) and tax liabilities (£3.2M) were offset by increases in bank overdrafts (£1.3M) and advances from clients (£2.2M). The result is a net tangible asset base some £7.6M lower at £25.6M which is clearly not good.

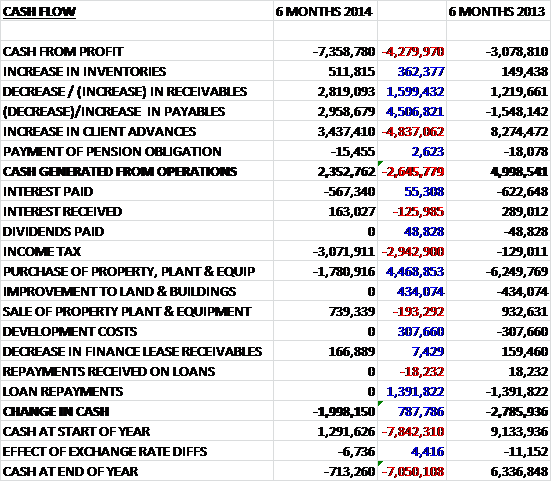

Before movements in working capital, the cash loss from operations was £7.4M, some £4.3M worse than during the first half of last year. Favourable movements in working capital, however, including a decrease in receivables, increase in payables and an increase in client advances meant that the cash generated from operations was £2.4M, less than half that received in the first six months of 2013. The bulk of this cash was actually paid on income tax which was some £3M and £2.9M more than last time which relates to higher taxes paid in India; and capital expenditure, which was at least £4.4M less than in the same period of 2013. The group did manage to scrape together £700K by flogging off some equipment but this could not prevent the cash outflow being £2M. This is poor but at least it was £800K better than the outflow in H1 2013. Clearly Shaft have a lot on their plate at the moment but it does somewhat annoy when their published statement of cash flow is incorrect due to a typo. The correct figures are above, not those quoted in the interim report.

During the first six months of the year, South Africa losses widened to £11.2M. The decline has several causes including the termination of a number of contracts (notably Impala 16, Impala 17 fridge shaft, Moab and Hernic Ferrochrome); the impact of strike action, safety stoppages, adverse currency movements and poor performance at Styldrift. Following the end of the strike in June, imminent changes to the terms of a number of contracts and some recent contract extensions, revenues in the country are expected to stabilise in the second half of the year. During the year the Impala 17 contract, which has long been loss making was converted to a cost reimbursable contract for a limited time until October. At this point, it will be retendered. Performance on the project was hampered by safety stoppages which contributed to a 4% reduction in South African revenues. Work at Impala 16 was suspended for most of the period due to strike action but after the strike ended, work levels are starting to return to normal. Unfortunately, however Impala declared force majeure at Impala 16 due to the strike action, but the group believes it may be able to recover certain costs from the client.

Although Styldrift made progress during the period, with sinking completed in the main and service shafts, this was offset by hoisting constraints and the lack of available cash. Due to the underperformance and the fact that rates did not cover costs incurred, the project recorded significant losses during the period which reduced South African revenues by 4%. Due to the lack of cash, the client chose to purchase some of the project assets and negotiations are ongoing in order to convert the contract to a cost reimbursable one. The project for Afplats, at least, continued to perform well and is now ahead of schedule with the main shaft now more than 1000m deep. Afplats awarded the group an extension for continuing the sinking of the shaft to 1307m which is expected to run until mid-2014. The work for Lonmin was affected by the strike action and the group was prevented from working on the project for a considerable time. After the end of the strike, management expect to be up to speed by Q4 this year.

During the first half of the year, International profits fell by £2.6M to £5.8M. Progress has been good at Kibali Goldmines where sinking is progressing in line with expectations and the main shaft has reached a depth of 500m. Operations at Hindustan Zinc delivered an improved performance compared to last year but remained significantly behind schedule and as a result the financial performance was below management expectations. The signing of the Kazchrome contract will improve revenues going forward. The METS division performed slightly below expectations due to the reduction in workload and the lack of any new contract awards.

As previously announced, the group has secured a short term loan facility with Hillside Investments which resulted in a bridging loan of £3.5M coming in to the group while the convertible loan agreement is prepared for approval that should bring in another £5.7M. This means that the group should have sufficient cash to meet its debt repayments, which require a payment of £2.9M this December. The Eurochem proceedings continue to hang like a dark cloud over everything Shaft does. There is no further news on this front but an outcome is likely to be forthcoming in 2015.

The order book stands at £191M, down from £238.2M at the end point of last year with a pipeline of £802M of outstanding tenders, including a number in South Africa. After year end, however, new contracts have added £47M to the order book. The outlook for the second half of 2014 is for an improvement on the first half of the year.

Net debt currently stands at £3.6M, a £2M increase on the end point of last year and clearly it is not appropriate to announce a dividend at this time. There is no getting away from the fact that these are terrible numbers. This has resulted in the cash squeeze, and the Indian tax bill has really not helped in this regard and the measures set about above to tackle this. There are also a number of operational problems at some of the projects, clients have cancelled work, the order book is not as healthy as it was and the bid pipeline is at its lowest level for some time. In addition, should Eurochem win their claim, the group will not be trading which is something that seems to be weighing on client sentiment. So, why would anyone want to buy shares in Shaft? Well, the immediate cash problem seems to have been sorted, there was a new international contract win (albeit for a related group) and the strike action in South Africa seems to be calming down. If, and it is a big if, Shaft survive until the Eurochem verdict and they win it, these shares will be very cheap. I have made a VERY risky small purchase on these grounds.

On the 29th August the group announced that it had been awarded a six month extension by Impala at Impala 16. The contract has a value of £3.7M and relates to development work on a number of levels within the shaft complex and comprises drilling to excavate the levels as well as removal of waste rock via an underground railway. The contract is on a labour rates basis with a performance based element.

On the 13th February 13th the group released a statement that effectively said they were going bust. There is unlikely to be any value left for shareholders. This could be seen coming a mile off and I have made progress in that I managed to get out with some equity intact but I should not have made that risky punt – this has been a bit of a learning experience.

On the 17th February the shares surprised no-one by being suspended on request of the company. I suspect this will be the last SHFT update!