Gem Diamonds has now released their interim results for the year ending 2014.

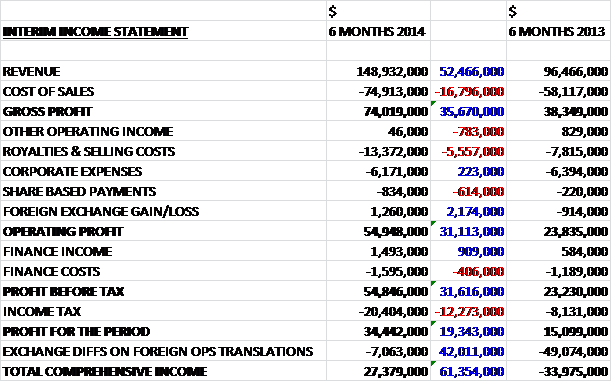

Revenues were up considerably, increasing by $52.5M to $148.9M. Cost of sales were up too, but not to the same degree so gross profits were some $35.7M higher than during the same period of last year. Other operating income collapsed to $46K and there was a $5.6M increase in royalties and selling costs, somewhat counteracted by a small reduction in corporate expenses and a $1.3M gain due to foreign exchange differences to give an operating profit $31.1M higher than in the first half of 2013. Finance income and finance costs broadly cancelled each other out before a $12.3M hike in income tax gave an overall profit for the period of $34.4M, an impressive $19.3M more than in the same period of last year.

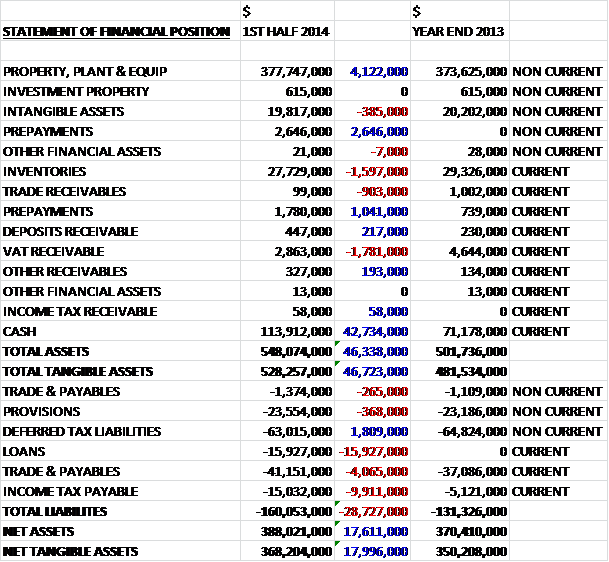

Total assets increased by $46.3M when compared to the end point of last year. This was mostly driven by a $42.7M increase in cash levels, but other increases included a $4.1M growth in the value of property, plant and equipment and a $3.7M increase in prepayments, which are the waste costs to be covered by the contractor over the term of the new contract, somewhat mitigated by a $1.6M decline in inventories and a $1.8M fall in VAT receivable. Likewise, liabilities also increased with the largest being a $15.9M new loan, a $9.9M increase in current tax payable and a $4.1M increase in trade and payables. This left net assets being some $17.6M higher at $388M, which looks rather good to me.

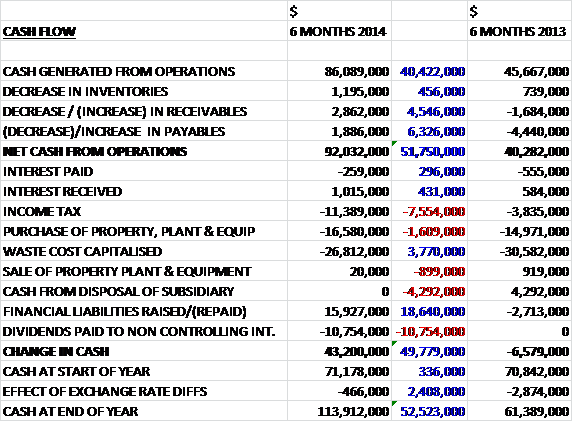

Before movements in working capital, cash profits nearly doubled to $86.1M. Favourable movements in receivables and payables meant that net cash from operations was a massive $51.8M higher at $92M. The largest expenses for the cash was $26.8M of waste cost capitalised, $3.8M less than in the first six months of last year; $16.6M sent on tangible asset capex, up by $1.6M which related to development at Ghaghoo, the coarse recovery plant at Letseng and the resource extension drilling; $11.4M of income tax, some $7.6M higher; and $10.8M on dividends to the Lesotho government. The group also gained some $16M in cash from new loans which seems quite strange to me considering this resulted in a $43.2M increase in cash levels to $113.9M. This is a seriously good result, the group is swimming in cash which makes it difficult for me to understand why it is taking out loans unless an acquisition is being lined up.

Letseng sold 53,799 carats during the period compared to 47,065 during the same period of last year and the price per carat increased from $1,741 to $2,747. Of the ore sourced, 36% was from the Satellite pipe with the remainder from the Main pipe. The Alluvial Ventures plant continued to run during the period and the contract was extended to the end of 2015. In addition, the installation of the secondary and tertiary crushers last year led to significant improvements in the fragmentation and blasting process, which increased plant throughput and helped lead to the increase in carats produced. Waste mining was 2% higher than in the first half of last year and in order to keep up, larger mining equipment consisting of two CAT excavators and trucks were commissioned in May.

During the period, Letseng negotiated a new contract with its mining contractor, MMIC, resulting in improved unit costs for the next eight years. The new coarse recovery plant project remains on track for completion in Q2 2015 for a total of $13.2M, of which $7.7M is expected to be spent in 2014. The X-Ray sorters have been ordered, which will ensure improved recovery of high value diamonds and improved x-ray scanners for personnel are planned for Q3 this year. Work to improve throughput and diamond breakage has been approved and phase one of the project has commenced and is planned to be complete by Q1 2015, which will deliver an increase in treatment capacity of about 250,000 tonnes per annum as well as further reducing diamond breakage. Of the $4.7M expected to be spent on this project, $3.6M is expected to be spent this year.

During the period, five tenders were held for Letseng’s production resulting in rough diamond tender revenue of $147.8M. Higher quality diamonds due to lower breakage and increased production from the Satellite pipe has resulted in the increased revenues seen in the period. The focus at the mine going forward will be continual improvement of current operations and costs, delivery of the Coarse Recovery Plant, delivery of phase one and two of the Plant upgrade, optimising waste stripping profiles in order to maximise timing of moving from open pit mining to underground mining in the satellite pipe, and continual refinement of future phases of projects.

At Ghaghoo, 2,400 carats have been recovered so far during the commissioning of the plant which have included a 20 and two 10 carat stones. The production tunnels are progressing within kimberlite on the first production level at 154 metres below the surface where high volumes of water from basalt fissures have been encountered which has contributed to difficult mining conditions and has necessitated the procurement of additional pumping capacity and the drilling of additional bore holes but is not expected to impact production in 2015. Drilling of the second ventilation hole is complete and the third and final hole has been drilled to a depth of 121 metres and was completed in July. So far, $82M of the total budget of $96M has been spent with the balance being spent in the second half of the year.

Going forward, the focus at the mine will be the build-up of production to 60,000 tonnes per month, continuing underground development to ensure production sustainability, designing and developing a long-term water management system, determining the next phase of expansion and optimising the sales and marketing arrangements. A sale of Ghaghoo’s initial production is scheduled to take place before the end of the year. The marketing and manufacturing business contributed $2.4M in additional revenue to the group and 377 carats of Letseng rough diamonds were extracted for polishing and manufacture at Baobab, with 371 carats of rough diamonds being received from third parties for analysis and manufacturing, for which Baobab charges a fee.

As reported on previously, the group has released a revised resource and reserve statement. Letseng indicated resource base increased in carat terms by 127% to a total of 3.2 M carats with an average grade of 1.73 carats per hundred tonnes. This increase is a result of the extension of the indicated depth classification from 100m below the mining face to 350m below as a result of infill drilling programmes, improved estimation techniques and detailed geological studies. Due to the substantial improvement in indicated resources, an increase in the Letseng reserve base is also noted, increasing by 64% to 2.3 M carats. This increase means that the 21 year life of the mine open pit is entirely contained within the reserve.

Going forward, the board have approved capital projects of $40.5M in respect of continued development of Ghaghoo and $19.2M relating to various projects at Letseng. The second half of the year should see the strong diamond price maintained with continued growth in demand from Asian markets, along with strength in traditional markets.

The new debt incurs interest at the South African interbank rate plus 4.95% which makes it all the more curious that the group has taken it out given the large cash reserves, in my opinion it indicates that the board have an eye on an acquisition. The company is still on target to pay its maiden dividend in March 2015 based on the full year results. There is a very strong net cash position of $98.4M, an increase on the $71.2M at the end point of last year. Overall, this is a very good set of results, the Letseng mine is powering ahead and seems to be very cash generative, despite the capital expenditure that has taken place. Over the next year, more will be spent improving operations at Letseng and bringing Ghaghoo up to speed. The presence of large quantities of water is a slight worry but the group seem to be on top of this. I am pleased with my share purchase here and happy to hold.

On the 1st October the group announced that they had sold the 198 carat white diamond for $10.6M which seems like a decent rather than spectacular price

On the 6th November the group released an interim management statement covering Q3 2014. Although the prices received for Letseng’s high value production remained healthy at $2,603 per carat, compared to $2,582 in Q3 last year, the market for both rough and polished diamonds declined towards October but the group expect prices at Letseng to remain resilient for the rest of the year. The commissioning of new earthmoving equipment at Letseng has resulted in a 5% increase in waste mined over the same quarter of last year but the number of carats produced fell by 1% due to a vertical conveyor on Plant 2 being replaced and a higher percentage of ore being sourced from the Main pipe.

The new Coarse Recovery Plant project remains on track for completion in Q2 2015 for a total budget of $12.5M and the XRT sorters arrived in South Africa in October. The design of the Personnel Control Centre is well advanced and includes an X Ray scanner which has already been tested for accuracy and health & safety. The civil contractor has commenced work as planned and the other contractors are scheduled to mobilise in Q4 of this year. The Plant 2 Phase 1 upgrade project has been approved for implementation and is on track to be completed by Q1 2015. It is planed to deliver an increase in treatment capacity of 250,000 tonnes per annum as well as further reducing diamond damage.

In Botswana development is currently progressing in four production tunnels withing the kimberlite on level 1. The significant volume of water flowing in from a fissure within the Basalt country rock has been managed efficiently and the final sealing of the fissure is in progress. The tunnels in the old sampling level were intersected during August and they are now accessible and have been dewatered, fully inspected and made safe. The second ventilation hole has been completed and work is progressing to link it with the first hole. The significant intake of water has impacted planned development rates and the monthly production rate is now likely to be achieved by the end of Q1 2015. A training slope has been developed on Level 0 which will be used to provide ore to complete the optimisation of the treatment plant during the latter part of this year. At the end of the period, 4,028 carats have been recovered from Ghaghoo and it has been decided to hold the initial sale alongside the Letseng sale in February 2015 to allow existing customers to participate.

All in all it is not a bad update but the softening market for diamonds is a concern and although the prices at Letseng are expected to hold up, the lower quality Ghaghoo diamonds could suffer. Also although the water problems seem to have been overcome it is a bit disappointing that production has been delayed. Nevertheless I have decided to top up on the share price weakness.

On the 29th December the group announced that non-executive director Gavin Beevers had purchased 14,800 shares at a cost of abut £25K. He now owns just under 160,000 shares so this is a nice vote of confidence.

On the 7th January it was announced that the Capital Group’s Smallcap World Find fund had sold 19,850 shares so that it’s holding went below the 5% threshold, which is a shame.

On the 27th January the group released a trading update for Q4 2014. During the quarter the Antwerp Diamond Bank announced its closure which led to concerns over the availability of liquidity in the rough diamond market, weakening market sentiment during the period that led to downward pressure on prices during the period which is likely to continue into Q1 2015, although the high quality of Letseng’s output offers some resilience. Operationally at the mine 25,525 carats were recovered, a 9% fall when compared to Q4 last year due to falling grades despite the new machinery allowing a higher quantity of ore to be processed. At the three tenders during the period, 31,614 carats were sold at $2,140 per carat, a fall of 18% on the price per carat this time last year but is still slightly above the $2,043 average per carat achieved during the whole of last year.

During the quarter, 13 exceptional rough diamonds were extracted including a 299 carat yellow diamond which was sold into a partnership arrangement in January with Letseng to share 50% of the polished uplift. Other highlights were a 113 carat white diamond sold on tender for $5.8M and a 90 carat white diamond sold for $4.2M. Mainly due to the yellow diamond, some $15.2M worth of diamonds remained in polished inventory at the end of the year compared to $2.9M at the end of last year which affected the overall group revenue to the tune of $12.3M. The new Coarse Recovery Plant remains on track for completion in Q2 2015 for a total budget of $12.1M and the majority of the equipment is now on site with construction underway. The plant will optimise the treatment of the high value, coarse fraction of ore and is expected to improve the recovery of the high value Type 2 diamonds. Implementation of the Plant 2 Phase 1 upgrade project commenced in Q3 and is on track to be completed by the end of Q1 2015 following a planned three week implementation shutdown. This project is expected to deliver an increase in treatment capacity of 250,000 tonnes per annum.

In Botswana the development of Phase 1 at Ghaghoo has continued to progress well. Three kimberlite tunnels on the first main production level have been fully developed to the northern orebody rock contact while the fourth is nearing completion. The sealing of fissure water intersected by the basalt country rock has been completed and a significant amount of work has been done to enable any future water intersections to be handled efficiently. The training stope and access tunnels in the kimberlite on Level 0 have continued to provide ore for the plant during the commissioning period and will continue to do so until replaced by steady production from level 1 later in 2015. By the end of December, 10,167 carats had been recovered but the grade averaged out at just over 21 cpht compared to the expected 27 cpht. The grade was negatively impacted by highly diluted ore derived from the margins of the pipe and normal plant inefficiencies during commissioning. During the latter part of the period, the grade improved and management expects the anticipated grades will be achieved when production ramps up. The initial sale of about 10,000 carats will be held in Botswana and Antwerp during January and February 2015.

At the period end, the net cash position of the group stands at £73.6M and the group is still on track to declare its first dividend to shareholders at the announcement of the final results in March. Although the long term prospects of the group remain very strong, there is no doubt that the altogether unexpected weakness in the diamond market will have an effect on profits. Management expect it to continue into Q1 and I have sold out until there is a little less uncertainty about the prices going forward.