Tower Resources has now released their interim results for the year ending 2014.

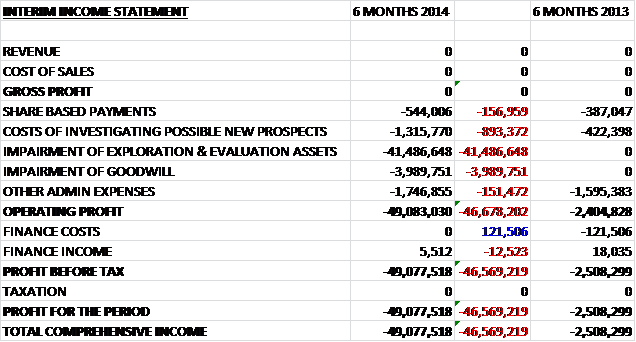

As there were no sales or cost of sales, the operating loss is made up of admin expenses. By far the largest of these was the non-cash impairment of exploration assets relating to the failed Namibia drill. Another non-cash item was the $4M impairment of goodwill, which was attributable to Neptune Petroleum in Namibia. The cost of investigating new prospects was £893K higher than in the same period of last year with share based payments and other admin charges also increasing somewhat on last year to give an operating loss of £49.1M which due to the lack of any finance costs this period was also the loss for the half year, some £46.6M worse than in the first half of 2013. It seems to me, though, that the profit and loss account is pretty useless to use to analyse Tower.

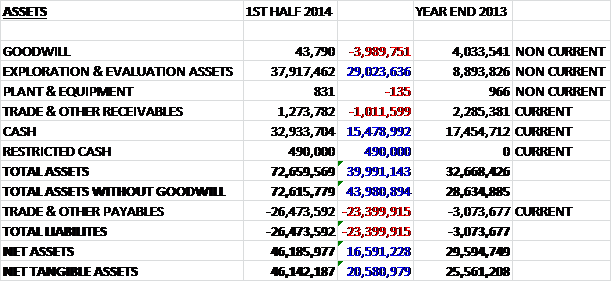

Overall, assets more than double to $72.7M driven by a $29M increase in exploration & evaluation assets and a $15.5M hike in cash due to the share placing. This was only partially offset by a $4M reduction in the value of goodwill and a $1M fall in receivables. Liabilities also increased, up $23.4M predominantly due to an increase in payables on the Namibia well ($21.8M). This all meant that net tangible assets increased by $20.6M to $46.1M.

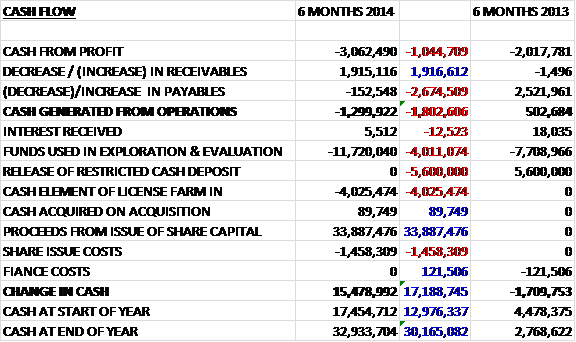

The cash flow statement is more useful for analysing the shape of the company. Before movements in working capital, the group has a cash outflow of $3.1M, some $1M worse than in the same period of last year. A decrease in receivables and a modest decrease in payables meant that cash spent on operations was $1.3M, $1.8M more than in H1 2013. The group needed to issue further share capital which brought in a net $32.4M. The bulk of this cash ($11.7M) was spent on exploration and evaluation, with another $4M used to farm into a license. This meant that at the end of the year there was still $33M in the bank, an improvement of $15.5M on the start of the year.

The first half of the year was clearly dominated by the lack of a hydrocarbon find at the Welwitschia-1 well offshore Namibia. The drill itself was beset by a number of operational issues and delays which meant that the decision was made to plug and abandon the well having drilled to a depth of 2,429 metres after finding that the shallower targets were non-reservoir. Work is ongoing to obtain a full understanding of the results but the group have stated that the prognosed sands in the late Cretaceous and early Tertiary sections were absent and there were no indications of hydrocarbons while drilling and that the amplitude anomaly seems to be related to lithological variation. There remains a desire to assess the remaining prospectivity of the block, specifically the untested deeper Albian carbonate sequence that was not reached due to the delays and cost over-runs of the well.

As of the end date of these accounts, the group had paid $11.4M in relation to the Welwitschia well and has since settled a further $13.9M. Repsol, the operator of the well has submitted further claims which indicate another $7.5M is being sought. Both Tower and the other non-operating party are disputing certain of these costs and this $7.5M is some $5M higher than that estimated by the operator. The extra costs are due to the delays and operational problems mentioned above and it seems fair to me that these extra charges should be paid by Repsol as the operator – we shall see how this goes.

During the year, as reported on previously, the company acquired Rift Petroleum in consideration for the issue of 550 million shares. The acquired group was a private exploration company focussed on the offshore South African region with additional licences located onshore Zambia. The acquisition gives Tower a 50% interest in two South African offshore areas with a number of oil majors such as Exxon, Total and Shell active in adjacent blocks. The primary asset is a 50% non-operated interest in the Algoa-Gamtoos licence alongside operator New Age Energy Algoa. It covers seven blocks and nearly 12,000 km2 between two areas that have been farmed into by Exxon and Total. The license consists of three prospective basins, Algoa, Gamtoos and Outeniqua and the mapping of seismic is ongoing. Rift Petroleum also had rights to acquire a 50% interest in any exploration right granted to New African Global Energy over the SW Orange Basin area covering three blocks and 27,500 km2. In addition, Rift owned an 80% Operating interest in two blocks onshore Zambia (blocks 40 and 41) and finally, negotiations were initiated in Ethiopia and are ongoing.

The application for the license renewal at Algoa-Gamtoos is scheduled to be submitted by November of this year and the results of the 3D seismic are going to be used to re-map the existing leads and provide the basis for a farm-out process but it now looks like the group will not be in a position to drill the first well on the license until mid to late 2016. The first deep-water well to be drilled offshore South Africa was spud in late July in a block adjacent to Algoa-Gamtoos which should be complete by November. Any success with that well would provide encouragement for the potential of the basin that continues into the Algoa-Gamtoos license area. At the second South African license area, where Tower has a potential for a 50% interest, recent data shows the potential for large deep-water turbidite oil plays and large synrift traps that would require a seismic acquisition to map further.

The partner in Towers 80% owned Zambia blocks is Blue Square Oil and Gas and the license comprises of several thousand metres of Permian to Jurassic age sediments. During August, extensive geological field study work across both blocks was undertaken, including rock sampling of potential reservoir rocks and geochemical analysis of potential source rocks. The results of this analysis should be completed by year end.

The group agreed to farm in for a 15% interest in Block 2B in Kenya which is operated by 30% owner, Taipan Resources. The remainder of this licence is held by Premier Oil. In consideration for the farm in, the group paid $4.5M in cash, 9M in shares and a further contingent payment of $1M on spud of a second well. The block is estimated to contain mean gross unrisked prospective resources of 1,593 mmboe and the first Badada-1 prospect well is due to be drilled by Q1 2015. This well is due to be drilled to a depth of 3,500 metres and is targeting prospective resources of 251 mmboe in Tertiary and Cretaceous reservoirs with an expected gross well cost of between $20M to $25M. On an adjacent block a well encountered an upper gas bearing interval which tested gas at a maximum rate of 6 M cubic feet per day from a 25 metre net pay interval. A deeper test was inconclusive with a small gas flare and oil recovery in small quantities. The next well that was drilled on that block is scheduled to be complete by early November of this year. The Badada well is targeting different sands but the results may be relevant.

There has been no activity for Tower in Western Sahara but an application to extend the expiry date of the license to December 2020 has been submitted. Kosmos energy is due to drill a prospect well within the disputed area towards the end of this year, however, so the results of that may be interesting. In Ethiopia, negotiations are due to commence shortly for two blocks in a frontier basin and the group continues negotiations in Madagascar to obtain a license for Block 2102.

In Cameroon, Tower was the preferred bidder for the offshore Dissoni block which is located in the Rio del Rey basin and negotiations have continued throughout the year. The block is located in an area of proven oil production and there is already one shallow discovery there with the potential to find sufficient additional resources to make a commercial development viable. There is also a higher risk potential in the deeper section that has not been successfully imaged to date. There is significant competitor activity nearby with both Glencore and Parenco planning new seismic in adjacent blocks. If successful with the bid, Tower would look to acquire 3D seismic in H1 2015 with drilling to potentially follow in 2016/2017.

The placing of 550 million shares for the acquisition of Rift Petroleum raised proceeds of £19.3M and £820K was raised via a modest draw-down on the EFF agreement with Darwin that resulted in the issue of 19 million new shares. After period end, the company issued a further 10 million shares as part settlement for consulting services.

Overall then, this update is dominated by the failure in Namibia which meant that my initial stake is now looking rather poor. There seems to be enough cash to cover the costs of this well but more will need to be raised before the end of the year to drill the Kenya prospect, which is the next one on the horizon. For now, then, it seem to me that there will be several quiet months before more can be learned about the Kenya resource before drilling should start early next year. There is no point selling out now, this was always going to be a risky punt so it’s a case of wait and see for now.

On the 8th October the group updated the market regarding the drilling campaign in Kenya. The operator (Tower has a 15% interest) has signed a letter of intent with the Greatwall Drilling Company of China to contract a land rig for the planned Badada-1 well onshore Block 2B in Kenya. The well is expected to spud between mid December and mid January and should take about 70 days to drill. It is planned to be drilled to a depth of between 3,000 and 4,500m to test primary Tertiary age reservoirs and potentially secondary upper Cretaceous age reservoirs. Management estimate a mean gross unrisked resource of 169mmboe. Taipan predicts an additional 405mmboe of gross mean unrisked resources in the four prospects and leads immediately adjacent to the Badada-1 well. In total in the block 19 leads have been identified with total estimated gross mean unrisked prospective resources of 1,593 mmboe. Gross well costs are estimated to be between $20M and $25M with between $3M and $3.75M attributable to Tower.

On the 18th November the group announced that the operator of the Badada-1 well in Kenya has received formal notice from the High Court of Kenya of a temporary injunction preventing the company from working on the well. Co-respondents in the lawsuit are the Kenyan Cabinet Secretary, Ministry of Petroleum and Premier Oil. The board are confident that the injunction will be revoked so that they can progress to a projected spud in early January. This all seems very ominous and I feel it is hard to justify and investment here until the uncertainty has lifted.

On the 27th November the group announced that a court order has allowed the operator of the Kenyan well to continue work at the site.The court also ruled that any related petitions against the respondents are to be consolidated and heard as a single petition at the next hearing scheduled for the 10th December.

On the 12 December the group confirmed that a court ruling allowed them to continue work on the Badada-1 well site with a further hearing scheduled after the projected completion of the well which will not affect the drilling timetable. The operators have executed a contract with Greatwall for the GW-190 land rig and have also contracted Norwell Engineering to manage the drilling operations. Drilling itself if expected to start in early January with the well expected to take about 70 days with costs net to Tower of between $3M and $3.75M. The well is designed to test the Tertiary age reservoirs and the total depth is planned to be between 3,000 and 4,000 metres. Local companies have been contracted to provide well site services such as logistics and road repairs and the operator has embarked on a number of initiatives including clean water projects and medical care for the local community, no doubt to improve their standing come the final court ruling.

On the 19th December the group issued a statement covering the disputed costs for the Namibian well. The group has reached an agreement with Repsol so that they will pay another cash payment of $3M to contribute to the increased costs which represents a $4.7M reduction against the previous estimate. Following this payment, Tower now have a cash position of $7.5M and is fully funded for its part in the Badada-1 drill. With this out of the way and the run up to the drill in Kenya now underway, I am tempted to pick up a few shares at this price.

On the 31st December the group sneaked out an announcement covering the grant of options to directors, the management team and consultants. Overall 78.7M shares were granted at an exercise price of 0.70p per share. The options will vest in three equal tranches in 12, 24 and 36 months. This brings the total number of outstanding options to 209.2M shares, representing more than 5% of the share capital of the company, which seems like quite a lot.

On the 7th January the company announced that the GW-190 rig had spudded the Badada-1 well onshore Kenya. The well is planned to be drilled to a total depth of between 3000 and 4000 metres to test Tertiary age reservoirs analogous to those in the Lokichar basing where Tullow have made discoveries. It is expected that the well should take 70 days to complete drilling and Tower will be updating the market every two weeks throughout the drill, which is a pleasing change to the lack of updates last time.

As promised Tower have released an update on the Badada-1 well drill on the 21st January. So far the well has been drilled to a depth of 918 metres MDBRT (Measured Depth Below the Rotary Table, whatever that means) intersecting the Neogene sequence. A 20 inch casing point has been set 298m MDBRT and the well is currently drilling ahead to the next casing point. It is planned to be drilled to a total depth of between 3,000 and 4,000 metres in order to test primary targets in Tertiary age reservoirs and is expected to take up to 70 days to complete. Another update will be made in about two weeks after further progress. There is nothing much to note really but nice to have an update nonetheless.

On the 4th February the group released another statement covering progress at the drill. They have now drilled to a depth of 1,647 metres MDBRT. 13 3/8 inch casing has been run to 1,644 metres and cemented in the 17 1/2 inch hole and the well is currently preparing to drill ahead with the 12 1/4 inch hole section to the next casing point which expected to be at TD. Not a huge amount of interest but nice to be kept up to date.

On the 18th February the group released another statement covering the progress at the Badada-1 well. It has now been drilled to a depth of 3,372 metres, intersecting the Neogene sequence. Preparations are underway for the logging of the hole section between 1,644 and 3,500 metres and is expected to be completed within a few days.

On the 23rd February it was announced that following completion of the logging operations, the well will be plugged and abandoned as a dry hole. The drill was completed in less time than expected and under the gross budget of $25.8M so that is something I guess. The well encountered a thick and untested Neogene age succession in the Anza basin and although commercial hydrocarbons were not found, minor gas shows and traces of heavier gas molecules indicate the presence of a thermogenic source rock. Drilling results suggested that the section here is sandier than had been expected and the development of sealing claystones is less than had hoped. The partners will be evaluating the results of the well to assess the remaining prospectivity in this large area. So, this is all rather disappointing but not totally unexpected and I do appreciate them getting straight to the point in this update. My holding here is pretty much worthless so I guess I will have to wait and see what happens next!

On the 19th March the group have released a corporate update. The portfolio now has limited financial exposure with no drilling commitments and discretionary programmes being cut. The current cash balance is around $4M after paying in full for the Kenya well. Due to the undervaluation of exploration assets, the board are apparently alive to the opportunity for consolidation as well as the attractiveness of building a wider low-cost, high-impact exploration portfolio.

In Kenya, the operator is in talks with the Kenyan ministry of energy regarding how best to complete its evaluation of the remaining prospectivity of Block 2B. Badada-1 was the first well to target Tertiary rather than Cretaceous age source and reservoirs within the Anza basin. The information gained from the well should enable the group to make better predictions of seal and source for any future drilling which reduces risks. Despite being a duster the well took only 51 days and came in slightly under budget with $3.8M net to the group. Financial commitments are fully met and they do not expect significant additional expenditure this year with any additional drilling likely to require a farm-out. The injunction rumbles on, however, but with a hearing expected shortly the named parties believe the claims have no merit.

In Zambia, where the group is operator with an 80% interest, the company has completed all of its initial period commitments. During August, the group completed a programme of geological fieldwork in blocks 40 and 41 of the Zambezi basin as part of the initial period work programme. The results of this work will be submitted to Zambian Ministry of Mines and Energy in the coming weeks and initial results are encouraging and indicate that the elements for a working petroleum system are present. The three year second period has been split into three on year periods which would involve further field work, minor gravity data acquisition and interpretation and then potentially a 2D seismic programme. Tower will be looking for partners to fund these surveys in 2017.

In Namibia, following resolution of their dispute with the operator, Repsol, regarding final drilling costs the company continues to evaluate the remaining potential in the license. The well completed in June failed to reach the deeper Albian Carbonate targets identified previously and attention is now focussed on a reassessment of the potential here in the light of extra geophysical data obtained from the well during the reassessment period.

In South Africa, where the group has a 50% interest, concerns about the regulatory environment have been lessened by the government’s decision to consult further with the industry. On the Algoa-Gamtoos block, the processing and interpretation of 3D seismic data acquired during the year has continued. The first renewal application to the exploration right has been submitted to the Petroleum Authority and it is expected to be granted in the second half of 2015 and the hope is to be in a position to start drilling in 2016/2017 with Tower’s preferred option being to farm out part of its interest in advance of that time. Adjacent to the group’s block, Total spudded the deep water Brulpadda 1 exploration well in August but due to technical issues with the rig, drilling was abandoned with a view to returning in 2016. An application to convert the SW Orange Basin TCP into a three year exploration right has been submitted with a formal response to the application expected later in the year.

In Cameroon, Tower was selected as preferred bidder on the shallow eater Disonni block and negotiations regarding the production sharing contract are now entering their final stages. The block is located in the under-explored Rio Del Rey basin which is an extension of the Niger Delta systems and offers the group access to potentially lower risk prospectivity combined with material upside in deeper gas/condensate plays. The priority on signing the agreement will be the acquisition of 3D seismic in H2 2015 and a partner will be sought to share the group’s financial commitment and provide additional technical input.

In the SADR, there has been some recent activity in the Aaiun basin where the CB-1 exploration well was drilled in the Morocco awarded offshore Cap Boujdour block. The well encountered 14 metres of net gas and condensate over an interval of about 500metres. The discovery was non-commercial and the well was plugged and abandoned. The result could be promising, though, as the well has established a working petroleum system with de-risks the plays along this part of the Atlantic Margin. Whether the group will ever be able to drill on its concession, however, is a key question given the disputed nature of the country. In Ethiopia, the company has decided to withdraw the application made for blocks AB3 and AB6 and in other news, the group will not be reviewing its £20M EEF with Darwin.