Laura Ashley has now released their half year results for the year ending 2015.

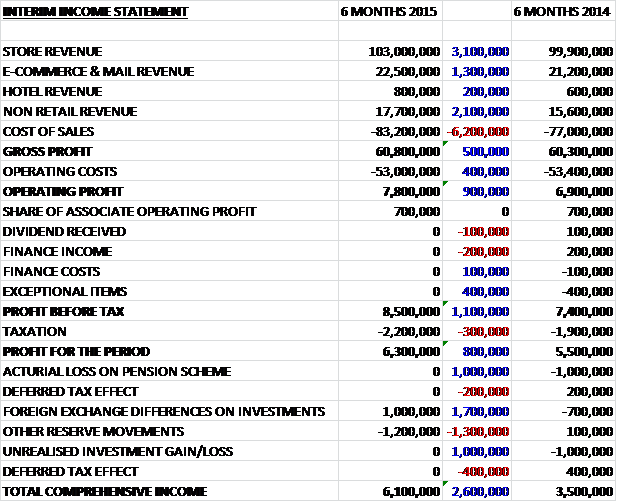

Revenues were up across all sectors with non-retail revenue showing a particularly good improvement, up £2.1M to £17.7M. Cost of sales also increased to give a gross profit some £500K higher than during the first half of last year. Operating costs actually fell during the period so operating profits were nearly £1M higher before the lack of any exceptional items, offset by a £300K higher tax bill, meant that the profit for the year was up by £800K to £6.3M.

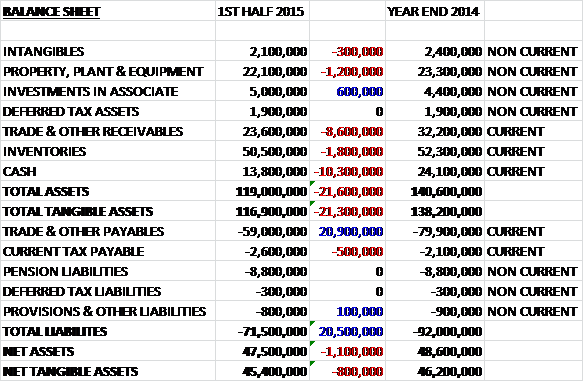

When compared to the end point of last year, total assets in the first half of this year fell by £21.6M. This was driven by a £10.3M fall in cash levels, an £8.6M reduction in trade & receivables, a £1.8M decline in inventories and a £1.2M fall in the value of property, plant and equipment. Liabilities also fell, driven by a £20.9M reduction in trade and payables to give net tangible assets of £45.4M, a modest £800K fall on the situation six months ago.

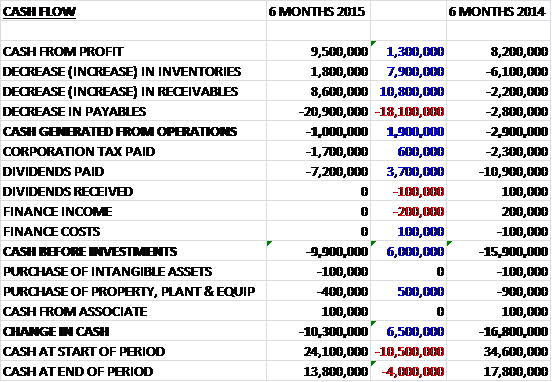

Before movements in working capital, cash profits were some £1.3M higher than during the same period of last year at £9.5M. A huge decrease in payables, possibly the “other payables” on the book at the year-end, meant that there was a £1M cash outflow at the operating level. This seems to be seasonal, as the same thing happened last year before payables evened themselves out and was £1.9M better than in the first half of last year. By far the largest destination for the cash was dividends, which at £7.2M were £3.7M less than in H1 2014 and the £1.7M spent on tax was some £600K better. Capital expenditure pretty much halved during the period to a paltry £400K, all of which meant the group had a cash outflow of some £10.3M, £6.5M less than last time.

During the period, retail stores contributed £7M, a £600K increase on the same period of last year and e-commerce retail contributed £4.6M, an increase of £500K. Two new stores were opened in the UK and three were closed, reducing total selling space by 1.3%. E-Commerce now represents 18% of total UK retail sales. Like for like furniture sales were down 1.2% but new ranges have been launched for the second half which it is hoped will halt the decline. Like for like Home Accessory sales were up 4.3%, which significantly outperformed the market, driven by lighting and gifts. Like for like Decorating sales were up 1.3%, which modestly outperformed the market and the best performing products were curtains and paints. Like for like Fashion sales were broadly flat during the period, which was an underperformance compared to the rest of the market.

In the first half of this year, the hotels made a loss of £100K, double the loss made in the first half of last year. The group have recently partnered with another hotel, this time in Windermere. The Belsfield is a 62 room hotel that has been entirely decorated in Laura Ashley products and customer response has been good. There is no real indication of what the group is planning to achieve with these hotels, which do not seem to be breaking even yet. During the period, non-retail items made a contribution of £6.6M, a £700K increase on the first half of last year. There was an increase of 10 franchised stores, with additional ones being opened in Japan, Australia, South Korea and Russia.

The board have approved an interim dividend of 1p per share which represents a stonking full year dividend yield of 7.3% at the current share price. Trading at the start of the second half of the year is up 8% on a like for like basis, so it would be good if this performance can continue. Laura Ashley is an odd beast really. The international franchises really seem to be driving what little growth there is. Trading in the UK stores seems OK, but nothing to get excited about. That dividend yield is something to get excited about, however, and it seems that the group’s main purpose is to give cash back to shareholders to the extent that there is virtually no capital expenditure. I am not sure what the strategy is with the hotels – are more being sought? Are they going to make the company money or just showcase their products. Who knows, there was very little in the way of narrative in the interim report. Overall I am more than happy to collect the dividends but it would be good to know more about their strategy going forward.