Dechra has now released its full year results for the year ending 2014.

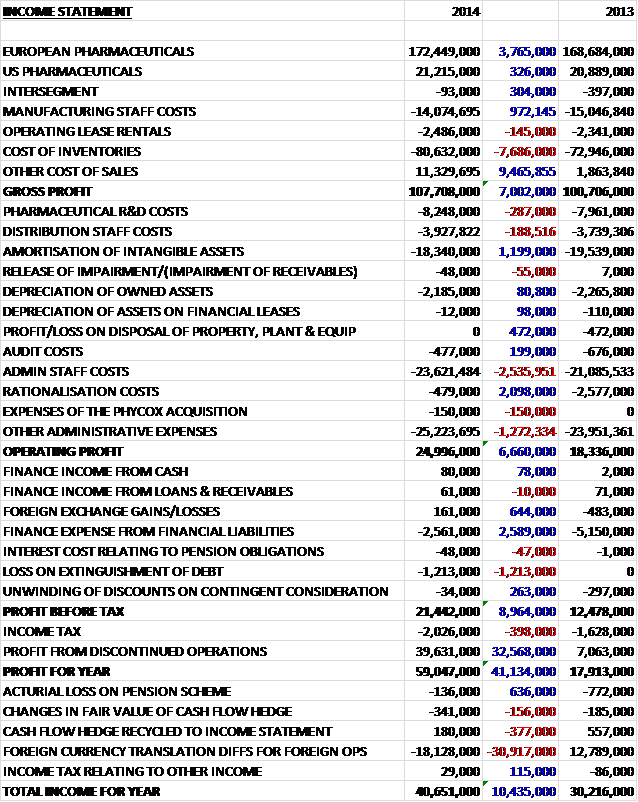

Revenues across both business segments increased, with European pharmaceuticals up £3.8M and US pharmaceuticals up £300K. Revenues also increased across most product categories with Food Animals the only one to show a decline. Manufacturing staff costs reduced slightly but the cost of inventories was up £7.7M. Other operating costs were well down, however, so the gross profit was some £7M higher than in last year. An increase in admin staff costs and other admin expenses were mitigated by a £2.1M fall in rationalisation costs and a £1.2M reduction in the amortisation of intangibles, which remained high at £18.3M, to give an operating profit £6.7M higher than in 2013. Finance costs fell despite a £1.3M loss on the extinguishment of debt to give a profit before tax of nearly £9M. The overall numbers were distorted by a £32.6M gain on the sale of the discontinued operations so that the profit for the year was £59M, up by £41.1M on last year.

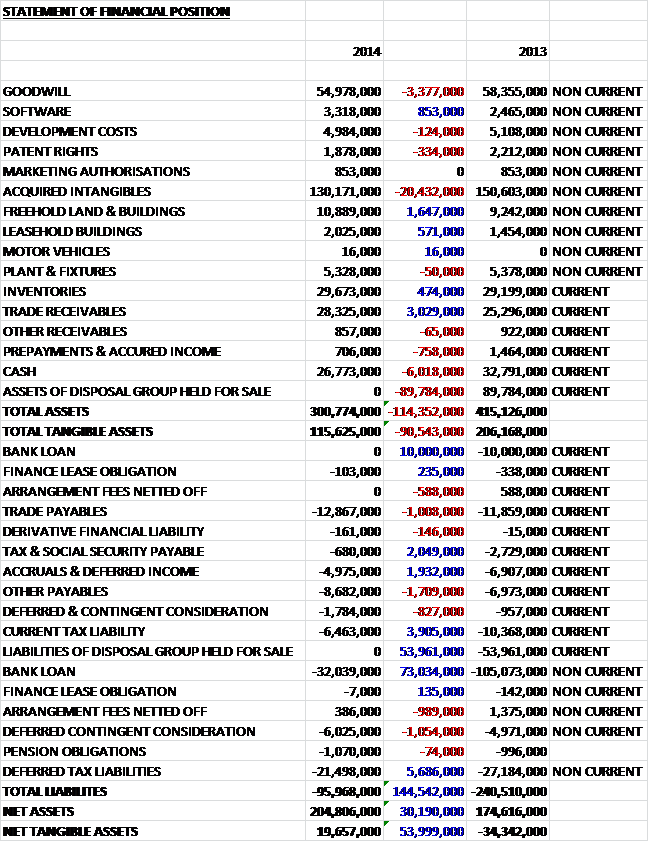

Overall total assets fell by £114.4M. This reduction was driven by the sale of the £90M of assets for the services group held for sale. Other large falls included a £20.4M reduction in the value of acquired intangibles which related to amortisation of development costs and product rights at the various acquisitions made in the past, a £6M fall in cash levels and a £3.4M reduction in the value of Goodwill. These falls were only partially offset by a £3M increase in trade receivables and a £1.6M increase in the value of land and buildings. Total liabilities also fell, down by £144.5M driven by an £83M reduction in the bank loan, the £54M of liabilities disposed of with the disposal group and the £5.7M fall in deferred tax liabilities, with the only substantial increases being a £1.7M hike in ‘other’ payables and £1M increases in both trade payables and deferred consideration. Overall this meant that net assets increased by £30.2M to £204.8M.

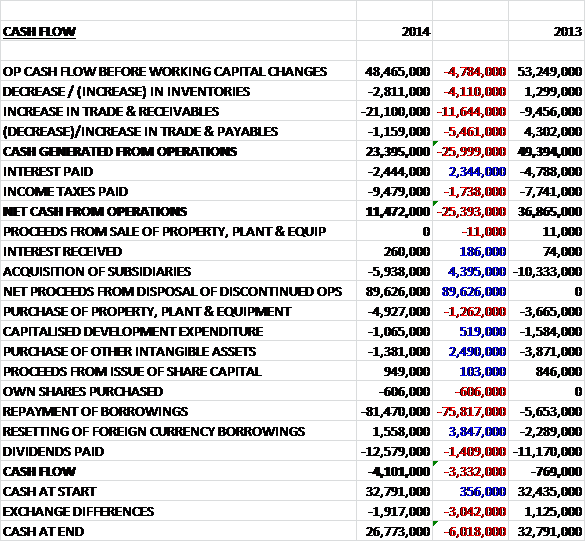

Before movements in working capital, cash from operations was £4.8M lower at £48.5M. There was a pretty disastrous movement in working capital, however, particularly a £21.1M increase in receivables that seems to be related to the disposal of the Services group, the exact details of which I have failed to understand, that meant cash generated from operations was only £23.4M, less than half that achieved last year. Interest payments halved but an increase in the income tax paid meant that net cash from operations of £11.5M was £25.4M lower than in 2013. This cash flow comfortably covers capital expenditure of £5M towards property, plant equipment; £1.1M of development expenditure and £1.4M of other intangible assets. It also nearly covers the £5.9M spent on the acquisition of subsidiaries. The group received nearly £90M from the disposal, the bulk of which was spent on reducing borrowings by £81.5M. The rest was then spent on dividends of £12.6M to give a cash outflow of £4.1M. The cash from operations does not seem to cover dividends which is disappointing.

Operating profit for European Pharmaceuticals was £49M, a £3.2M increase on last year. Despite this increase, there were some issues with Vetoryl sales momentum slowing down due to the phasing of sales in Italy and the unavailability of a drug necessary to diagnose Cushing’s disease. Apart from in the Netherlands, the defence strategy against generic competition for Felimazole proved successful. The main issue, however, was the decline in Food Animal products due to the reduction in the prescription of antibiotics and increased competition in the Netherlands. Sales of Cardisure increased by 32% and it is rapidly approaching one of the five most important products for the business. Another good performance was the 11% increase in the Equine range driven by a second half recovery of Equipalazone and a strong growth in the sales of HY50.

Operating profit for US Pharmaceuticals was £6M, an increase of £400K on last year. Some key products performed strongly including Vetoryl, with sales up 24%, Felimazole with sales up 19% and Dermapet with sales up 11%. There were no sales of Animax, however, due to supply issues which reduced sales overall by £1.5M. The performance of Felimazole was particularly good considering it is now competing with a number of low cost human generics

The strong performance of medicated shampoos was further enhanced by the recent launch of MiconaHex in the US. Other plus points have been Cardisure, a cardiovascular product has increased sales by 32% across the EU; Comfortan, an anaesthetic, has grown sales by 40% and Vetropolycin has been re-launched in the US following the resolution of a long term supply issue. A number of products acquired through Eurovet that were marketed through distribution partners have been taken in-house, enabling the group to retain the full margin and contracts with the previous partners ended in December, allowing the group to market Forythron in France and Sweden, and Atipam and Sedator in the Nordics.

Sales in Food animal antimicrobials fell by 7.3% this year due to a very competitive environment and a global focus on antimicrobial reduction. The Netherlands saw the largest decline and was the only European market to suffer an overall fall in revenue. This is predominantly due to the fact that Dutch vets reduced their antimicrobial usage by 50% due to government pressure. The board suspect that the group has further exposure to this trend, particularly in Germany where they have a strong market position.

During the year the group achieved approval in the US and the UK for Osphos, a new equine product that controls navicular syndrome that should go on sale in the first half of 2015. The product was also submitted for approval in the EU, but because the horse is a food producing animal in much of Europe, the approval process takes more time. Navicular syndrome occurs in approximately 6% of horses and causes pain and lameness in the forelimbs. Other new introductions have included: Buprenodale, a generic Buprenorphine injection launched in 16 European countries; Felimazole tablets 1.25mg, for hyperthyroidism in cats was launched in 12 European countries to try and counteract increasing generic competition; and MiconalHex+Triz, a dermatological shampoo was launched in the US to compete with the leading brand whose patent recently expired. In countries where the group does not have a direct presence, Felimazole tablets were launched in South Korea and Canada whilst Sedator and Atipam were launched in Israel.

As far as the pipeline is concerned, dossiers have been submitted in the US and EU for a new canine endocrinology product, a clinical trial is underway for a second canine endocrine product, studies are ongoing for a canine dermatology product and canine ophthalmology product, Osphos has been submitted in Australia and Canada, but unfortunately clinical trials for a feline endocrinology drug were suspended due to concerns over the formulation.

In the long term there are two major factors affecting the food animal market, which makes up 18% of group sales. There is increasing global demand for animal protein which in turn feeds demand for food animal drugs but as touched upon earlier, this is tempered by an increasing regulation of antimicrobial use due to the potential for drug resistant pathogens to develop. This has been most keenly felt in the Netherlands but it is likely that the rest of the EU and the US will follow suit in time. Spending on companion animals is growing globally and pet ownership is also growing in both developed and emerging markets. In addition, pets are generally living longer than in the past which in turn creates more demand for companion animal pharmaceuticals.

The group are actively looking to expand into new geographical areas where they have achieved critical mass. Trading started in Italy in March of this year and is the first major territory to be entered into since the US in 2004. Sales in that country have so far been in line with expectations. The group is also looking into entering Canada and they have appointed a country manager in Montreal and trading is expected to start in January 2015. Management have apparently identified other potential markets and intend to start trading in another new territory in 2016.

The group have made investments into the liquids, creams and ointments manufacturing suite, tablet compression machines and the encapsulation production line. The application to the FDA for the approval of the new canine endocrinology product prompted an FDA inspection of the sterile injectables facility in Skipton where the product will be manufactured. The group have invested a significant amount of resources and effort into ensuring that the facility meets the standards required. They have also moved the manufacture of Cardisure and Forthyron to the facility after they were brought in-house from outside manufacturers.

The new enlarged central European distribution centre in Denmark was opened in November after a €2M investment. The facility has more than doubled in scale and tripled the group’s pallet handling capacity. It creates a logistics hub that will fulfil the medium term distribution requirements, eliminates third party storage and handling costs and improves efficiency. The group has also started to transfer their Specific pet diets to a new external manufacturer and following the transfer, an improvement in quality, palatability and on time delivery has been observed. There has also been an investment into the IT platform that the group uses.

During the year the group acquired certain trade and assets of PSPC Inc for a total consideration of £8.4M. The principal asset is a product called Phycox, a patented nutraceutical which competes in the US joint health supplement market and there is also another product in the final phase of development. There is only £84K of goodwill being paid so the price seems fair, without knowing about the products in any more detail. A contingent consideration (included in the £8.4M total) of £900K was paid after the successful registration of the new product and there remains another £2.5M of contingent consideration payable after a certain number of sales. The group also paid out a further £10M of contingent consideration relating to the Dermapet acquisition, mainly due to a milestone sales target being hit. There remains another $6M of consideration payable relating to this purchase.

The transformational event that happened this year was the disposal of the Services group for proceeds of £91.2M which relates to a profit on disposal of £38.7M. The group are actively looking and have been in discussions with other companies with a view to acquire them but the valuations have apparently been too high.

At the last AGM, Neil Warner stepped down as Senior Independent Non Exec director and Ishbel Macpherson has taken over the role. In January, Ed Torr stepped down as an executive director following 17 years with the business, he will continue to work as a consultant for the group. Current trading is in line with expectations with growth consistent with that seen in the second half of the year.

At the end of the year net debt was just under £5M, a vast improvement on the £80.1M recorded at the end of last year and gives the group many more options for taking the company forward. The current P/E ratio is 34.3, falling to 20.3 next year on analyst’s predictions for EPS which is not cheap. The board have announced a dividend for the year of 15.4p, a 10% increase on the dividend last year and the dividend yield currently stands at 2% which again, is nice to have but not exactly high yielding.

This has been a fairly good set of results for Dechra, the supply problems in the US seem to have improved and it is good to see them take a number of products in-house to maintain market share. The generic competition for Felimazole is a concern as this is an important product for the group but they seem to be handling this well. Perhaps more concerning will be the impact when the German government decides to restrict the antimicrobial drugs. The diversification into Italy and Canada seems like a good move to me and the new Equine product looks promising. The disposal has also meant that the debt has been slashed which clearly makes this a less risky investment although the falling operational cash flow is a bit disappointing. The shares are not exactly cheap on a P/E or dividend yield basis though so I rate these as a hold.

On the 14th January the group released an update covering trading in the first half of the year ahead of the interim results that are due on the 23rd February. Group trading during the period was in line with management expectations with revenues increasing by 12% on a constant currency basis against a soft comparator period last year. European pharmaceuticals increased sales by 7% on a constant currency basis but only 0.5% on a reported basis. Sales of companion animal products were ahead of expectations with equine and diet products also performing strongly. These gains were offset by the continued pressure on vets to reduce antibiotic prescribing for food producing animals, however, particularly in Germany and the Netherlands.

US revenues increased by 59% on a constant currency basis (54% reported) which was predominantly attributable to the acquisition of Phycox, the launch of Osphos in Q1 and the relaunch of two Ophthalmic products following the resolution of the supply issues and all products have performed in line with expectations. During the period the group opened a subsidiary in Canada which should enhance growth going forward. In Q2 of the year the group obtained approval in all of their European territories for TAF spray, a FAP differentiated generic antibiotic aerosol to treat superficial wound infections. Due to the strength of the recent revenue growth in the US, management are strengthening sales teams there and so far in the rest of 2015, the group is performing within expectations.

Overall, this is a good update. It is particularly pleasing to see such strength in the US and the end to the long running saga of supply interruptions. In Europe, the drag of the food animal products due to antibiotic prescription pressure looks unlikely to change any time soon but in all, I may look to add if there is any price weakness.